Optical chipmaker POET Technologies (POET) recently saw its momentum take a sharp turn this week, feeling less like a gradual pullback and more like the floor suddenly giving way. Just days after riding a stretch of optimism amid its links with Marvell Technology (MRVL) and even whispers around Nvidia’s (NVDA) ecosystem, the POET stock was cut in half.

This was triggered after Marvell canceled purchase orders that once connected POET to Celestial AI, now under Marvell’s umbrella after a $3.25 billion acquisition. The explanation came quickly, but it didn’t soften the blow. Marvell cited confidentiality concerns, leading it to cancel orders linked to sensitive information disclosures.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For a company still building its footing in AI infrastructure, losing a key customer like that stings, cutting off the revenue stream for POET. And so, the market reacted just as quickly.

Still, this is not a full stop. POET is leaning into what got investors excited in the first place – its opto-electronics tech, including the Optical Interposer platform, built to power the next generation of AI networks. Demand for faster, more efficient data movement is rising, and POET has already been riding that tailwind, filling other orders, expanding its customer base, and counting on the broader AI boom to offset one lost relationship.

Shares of POET Technologies fell hard, but if artificial intelligence (AI) demand holds, the path to a rebound is not off the table.

About POET Technologies Stock

POET Technologies, founded in 1972 and based in Toronto, operates at the intersection of electronics and photonics, quietly building the backbone for next-generation connectivity. The company develops semiconductor solutions anchored by its Optical Interposer platform, which integrates electronic and photonic devices onto a single chip using advanced manufacturing techniques.

Its products power data centers, telecom networks, 5G infrastructure, and emerging applications like LiDAR and medical imaging. With a growing footprint across North America and Asia, and a strategic tie-up with Lite-On Technology, POET is positioning itself to ride the accelerating demand for AI-driven optical networking.

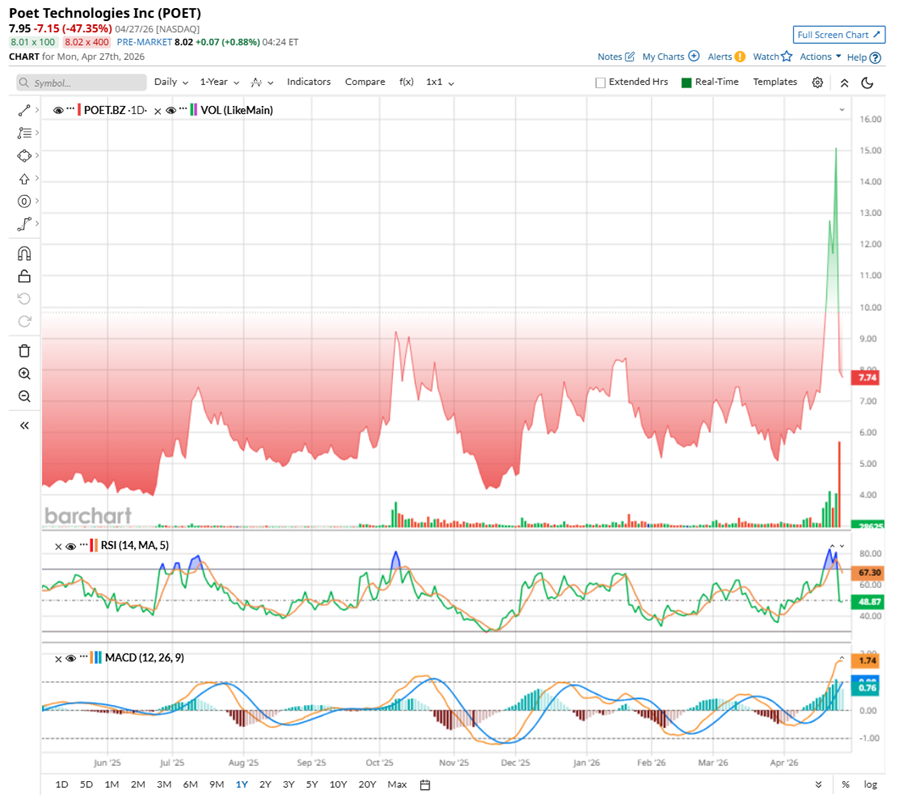

Valued at a market capitalization of $1.5 billion, shares of POET Technologies have experienced volatility recently. Through most of April, the stock looked unstoppable. By April 24, shares had surged more than 150%, fueled by optimism around its role in the fiber-optics and AI ecosystem. Much of that excitement hinged on what appeared to be a growing relationship tied to Marvell Technology.

Then came the reversal. On April 27, reality hit hard. News that POET had lost its contract with Celestial AI pulled the rug out from under the rally, sending the stock down 47.4% in a single session. In just hours, nearly all the gains built over the month, especially the last week’s surge, were wiped out, leaving investors scrambling to reassess the story.

And yet, even after the drop, POET stock remains up 86% over the past 52 weeks, with gains of 28.94% over three months and 54.53% in just the past month. The volatility cuts both ways.

Technically, POET stock’s 14-day RSI swung from near oversold levels last month to overbought territory during the rally, only to settle back 49.68. after the crash. This suggests the froth has largely been shaken out, with momentum resetting to neutral – neither stretched on the upside nor deeply discounted – leaving room for the next directional move to build more sustainably.

The MACD oscillator is flashing a bullish signal, with the MACD line rising above the blue signal line and both trending upward. Plus, rising histogram bars suggest momentum has not fully faded. While the sharp drop shook confidence, buyers may still be quietly holding on.

www.barchart.com

www.barchart.com A Closer Look at POET’s Q4 Report

On March 31, the company released its fiscal Q4 2025 earnings report, and the numbers reflected a business in the middle of a pivot – from pure development toward execution. Q4 revenue rose to $341.2 thousand from just $29 thousand a year ago, a meaningful jump that signals initial traction, even if it is still modest in scale. Still, the results fell short of Wall Street’s expectations, reminding investors that the ramp won’t be linear.

Losses narrowed, improving to -$0.32 per share from -$0.50 per-share last year. But the headline figure doesn’t tell the full story. A significant portion of the loss came from a $30.6 million non-cash fair value adjustment tied to derivative warrant liabilities, up from $12.4 million a year ago and $2.4 million in Q3. This was largely driven by new warrant issuances and a rise in the company’s stock price. Post year-end, POET repriced most of these warrants into U.S. dollars, a move expected to eliminate much of this accounting volatility going forward.

Operationally, spending is rising, as expected. R&D came in at $4.6 million, up from $3.4 million last year and $3.7 million in fiscal Q3 2025, reflecting a shift toward product development. Other non-cash costs included $2.2 million in stock-based compensation and $0.9 million in depreciation, both higher annually. Interest and other income climbed to $2.5 million, supported by stronger cash reserves.

The liquidity position is key. POET raised over $225 million during the quarter and another $150 million in January 2026, ending the year with $313.4 million in cash, cash equivalents, and investments. The company invested $15.9 million in 2025 toward 800G and 1.6T AI-focused optical engines and plans to spend another $30 million over the next two years, alongside $8 million for light source development.

Wall Street analysts tracking POET Technologies anticipate its fiscal 2026 loss per share to be $0.21, and then flipping sharply – shrinking over 109.5% year-over-year (YOY) – before finally crossing into a modest $0.02 per-share profit in 2027.

What Do Analysts Expect for POET Technologies Stock?

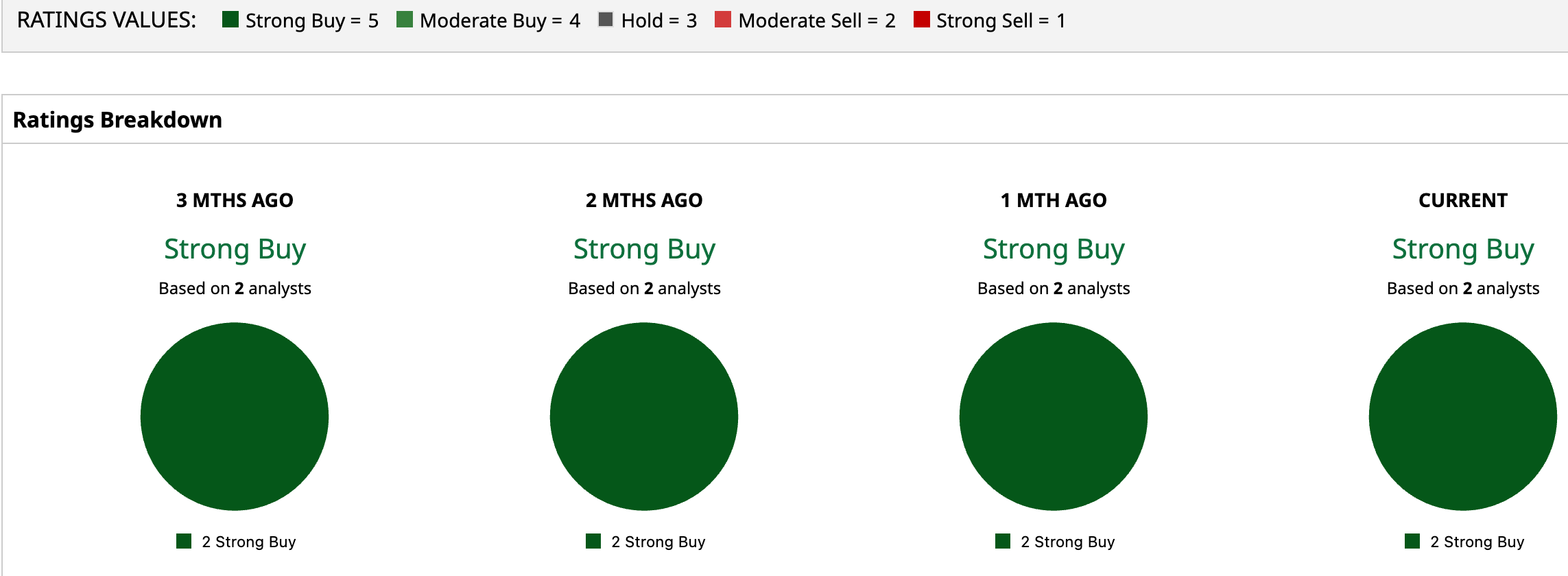

The Street may be quiet on POET stock, but the signal is still bullish. The stock carries a “Strong Buy” rating from the two analysts tracking shares. POET stock is currently trading above the average price target of $6.93 and just slightly below the Street-high target of $8.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

The loss of business tied to Marvell Technology has clearly changed the tone for POET Technologies. What was once seen as a validating partnership now leaves a noticeable gap, with revenue expected to take a hit this year. Beyond leaving a financial hole, the setback also hurts confidence, making other companies more cautious. For POET Technologies, still trying to prove itself, that kind of dent can make things tougher going forward.

Meanwhile, POET Technologies continues to face pressure from high cash burn, negative operating cash flow, ongoing dilution, and limited revenue against a stretched valuation. Without a clear path to large-scale manufacturing with a major partner, its fab-light model may struggle to deliver meaningful near-term revenue visibility.

And yet, the story does not end there. The surge in AI-driven infrastructure demand is real and only gaining momentum. POET’s opto-electronics technology still sits in a space that could benefit directly from this shift. If the company improves execution and delivers consistent results, investor confidence could return – just this time, it will need proof, not just a promise.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Canceled Marvell Orders Just Halved POET Technologies Stock, but the Company Is Still Betting on AI to Juice Demand Should You Buy the Dip in Spotify Stock Today? Amazon Reports Earnings Tomorrow, But a Key OpenAI-Bedrock Announcement May Mean Nothing Else Matters for AMZN Stock As Pony AI Unveils a New Autonomous Driving System, Should You Buy, Sell, or Hold PONY Stock Here?