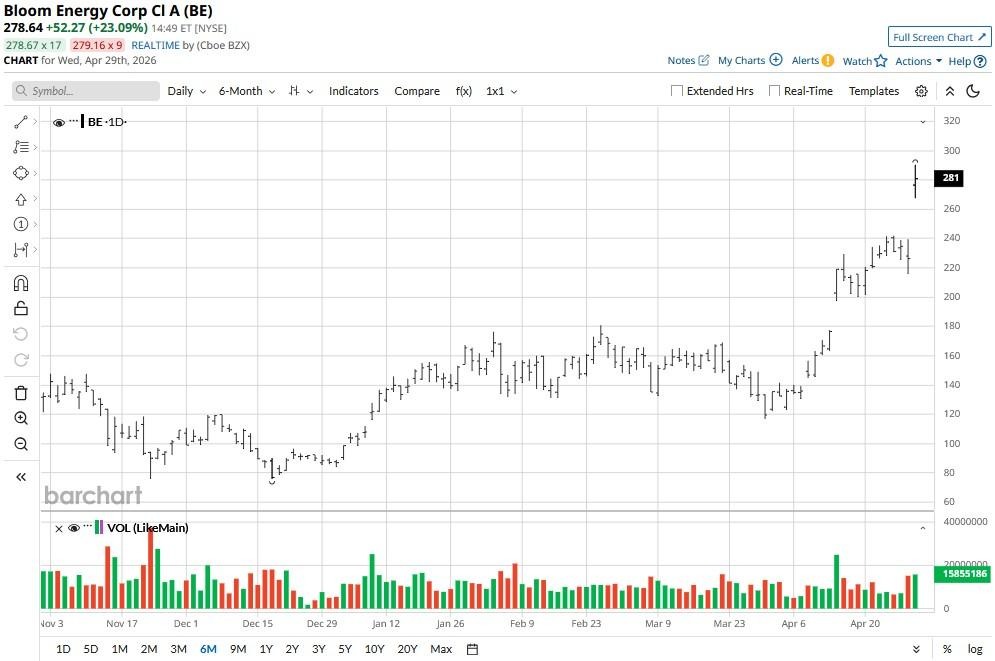

Bloom Energy (BE) shares soared on April 29 after the fuel-cell pioneer reported a blockbuster Q1, featuring massive orders from the artificial intelligence (AI) data center industry.

The company more than doubled its revenue to $751 million in the first quarter, crushing analyst forecast of $531 million. Adjusted earnings came in at $0.44, nearly six times the projected $0.08.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

The post-earnings momentum drove BE’s relative strength index (RSI) into the late 70s, signaling “overbought” conditions that often trigger a near-term pullback.

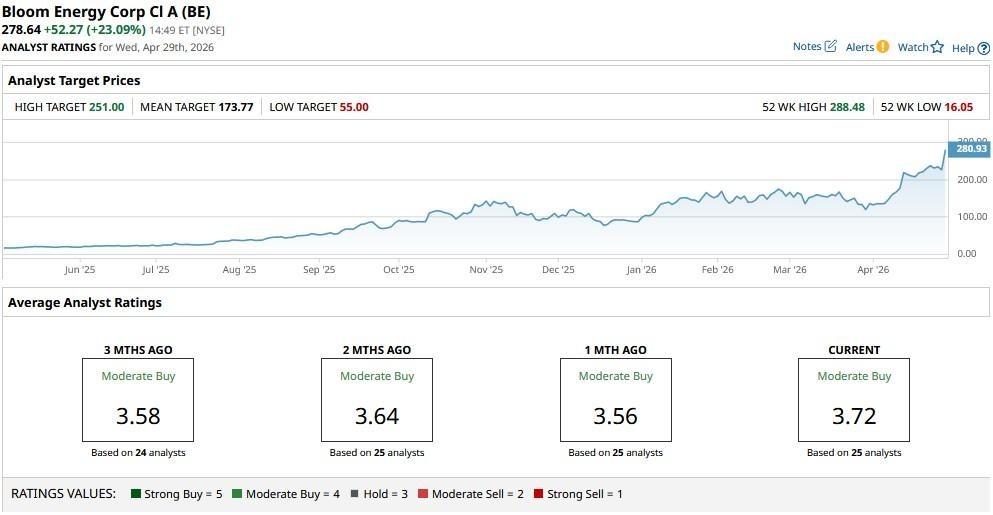

Still, Roth MKM analysts remain constructive on Bloom Energy stock that’s already up an exciting 223% year-to-date.

www.barchart.com

www.barchart.comIs It Too Late to Invest in Bloom Energy Stock?

Bloom Energy’s quarterly print warrants an investment primarily because it represents a significant shift in the company’s total addressable market (TAM).

The standout figure was a whopping 208% increase in product revenue, anchored by an expanded agreement with Oracle (ORCL), which plans on deploying up to 2.8 GW of BE’s fuel cell capacity for its AI data centers.

As grid constraints delay new tech builds, Bloom’s ability to deploy rapid, behind-the-meter power solutions has turned it into a critical infrastructure play.

BE stock is worth owning also because the NYSE-listed firm achieved a major milestone, flipping to a GAAP operating profit of about $72 million in Q1, reinforcing that its solid-oxide tech is now scaling profitably.

BE Shares Are Currently in a Strong Uptrend

Despite a meteoric YTD run and an oversold RSI, Roth MKM analysts remain positive on Bloom Energy shares mostly because of the firm’s unprecedented revenue visibility.

According to them, the order backlog effectively de-risks its newly raised revenue guidance for up to $3.8 billion in full-year revenue, up a remarkable 80% versus 2025.

Roth is bullish also because BE is currently the only fuel-cell provider with manufacturing capacity to meet the immediate, high-density power requirements of large language model (LLM) clusters

Investors should also note that Bloom currently sits miles above its major moving averages (MAs), indicating a strong uptrend that’s unlikely to fade without a meaningful catalyst.

Bloom Energy Remains ‘Buy’-Rated Among Wall Street Firms

Heading into the Q1 release, Wall Street had a consensus “Moderate Buy” rating on Bloom Energy, with a mean price target of $251, which actually translates to a 10% decline from current levels.

However, it’s reasonable to expect upward revisions in the day ahead, after the company’s stellar first-quarter financials that crushed both last year’s numbers and consensus estimates.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Your Smartphone Could Soon Be an AI Agent, and Qualcomm Stock Is Positioned to Profit Big Dell Stock Just Got a New Street-High Price Target. Should You Buy Shares Here? Broadcom Just Hit $2 Trillion Market Cap. Is AVGO Stock a Buy Now? Should You Buy the Dip in Robinhood Stock Today?