Seagate Technology (STX) stock has delivered phenomenal returns of almost 700% in the last 52 weeks on the back of AI demand, which has translated into a demand-supply mismatch for storage products. Strong demand coupled with price increases for storage drives has helped Seagate's top line grow and margins expand. This has triggered positive price action for STX stock as cash flows swell.

Seagate reported third-quarter earnings on April 29. Results and guidance topped Wall Street’s estimates. With STX stock surging higher on the news, some analysts have also upgraded their price targets. One key rating upgrade catalyst was Seagate's minimum 20% annual revenue growth guidance for the next few years. Further, with nearline capacity “almost fully allocated through calendar 2027” according to CEO Dave Mosley, there is clear revenue and cash flow visibility.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

It’s worth noting that Seagate retired $640 million in debt in Q3 and improved net leverage to 0.7 times. Further, with $2.4 billion in liquidity and a solid interest coverage ratio, Fitch has upgraded Seagate's credit to investment grade. With robust cash flow visibility, it’s likely that financial flexibility will remain high for dividends, share repurchases, and investment in innovation.

About Seagate Technology Stock

Seagate Technology is a provider of data storage and infrastructure solutions. The company’s key products are hard disk drives. Additionally, Seagate produces a range of data storage products like solid-state drives and storage subsystems.

With a large portfolio of patents both in and outside of the United States, Seagate is evidently focused on R&D and innovation-driven growth. With Mozaic 3+, the company brought HAMR technology “first to market and first to scale.” Further, Mozaic 4+ and Mozaic 5+ will likely extend the innovation spree. Mozaic 5+ shipments are expected toward the end of 2027.

For Q3 fiscal 2026, Seagate reported revenue of $3.11 billion, which was higher by 44% on a year-over-year (YOY) basis. For the same period, operating margin expanded from 20% in the prior-year quarter to 32.1%. With expanding margins, the company’s free cash flow was almost $1 billion for the quarter, coming in at $953 million.

With a continued flow of good news, STX stock has surged by 180% in the last six months. Given the optimistic growth outlook, this positive momentum will likely sustain in the coming quarters.

www.barchart.com

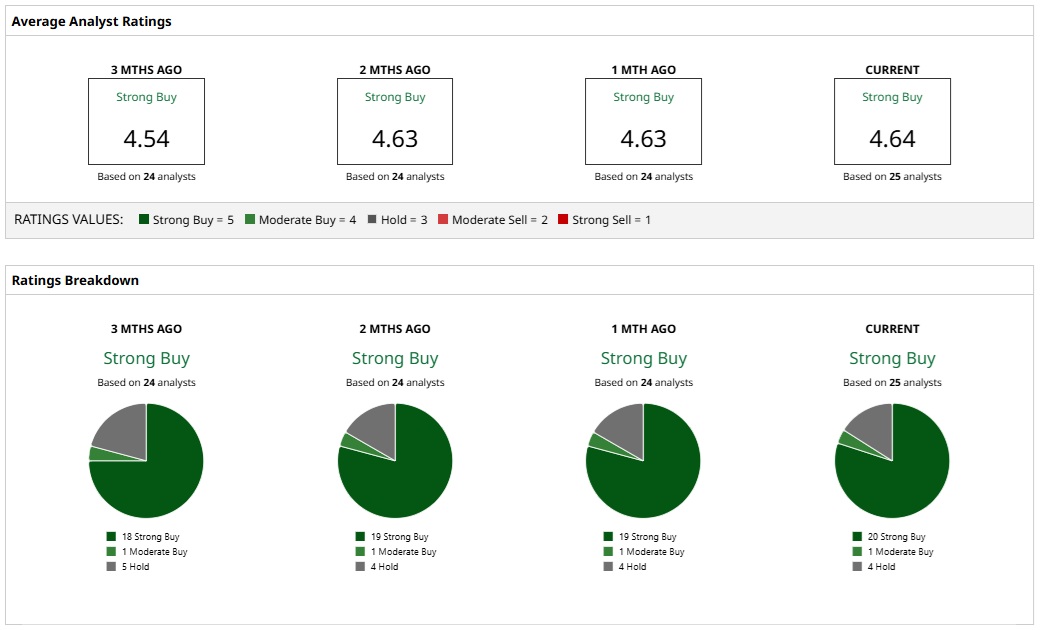

www.barchart.com What Do Analysts Say About STX Stock?

Based on 25 analysts with coverage, STX stock has a consensus “Strong Buy” rating. While 20 analysts have a “Strong Buy” for STX stock, one analyst has a “Moderate Buy," and four analysts have a “Hold" rating.

The mean price target of $717.32 has already been surpassed by current levels, suggesting minimal potential downside. However, the most bullish price target of $1,000 suggests that STX stock could climb as much as 39% from here.

www.barchart.com

www.barchart.com Among recent views, Morgan Stanley expects Seagate to benefit further from token growth and AI apps. Analyst Erik Woodring also believes that Seagate will “surpass 50% gross margins and $5 of quarterly earnings power in the December 2026 quarter.” By June 2027, the analyst forecasts Seagate "surpassing 60% gross margins."

Wedbush Securities also reiterated an “Outperform” rating following the recent results with a price target of $825. Meanwhile, JPMorgan analyst Samik Chatterjee is bullish as Mozaic 4+ has been qualified by two hyperscalers. With Mozaic on-track for shipments in 2027, the growth momentum is likely to sustain.

Overall, analyst views are overwhelmingly optimistic and backed by structural industry tailwinds. While STX stock trades at a forward price-to-earnings (P/E) ratio of 52.4 times, the P/E-to-growth (PEG) ratio of 1.06 times indicates that valuations remain attractive considering the earnings growth potential.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Can’t Get Enough of Seagate Technology Stock After Its Major Earnings Win 3 Reasons to Buy the Dip in Meta Stock — And 3 Reasons to Stay Away Dear Veeva Systems Stock Fans, Mark Your Calendar for May 7 META vs. MSFT: Which Is the Better Buy Now?