PayPal PYPL is set to report its first-quarter 2026 results on May 5, before the opening bell.

This digital payment company expected currency-neutral revenue growth in the low single digits for the to-be-reported quarter. Non-GAAP earnings per share (EPS) are expected to decline in the mid-single digits.

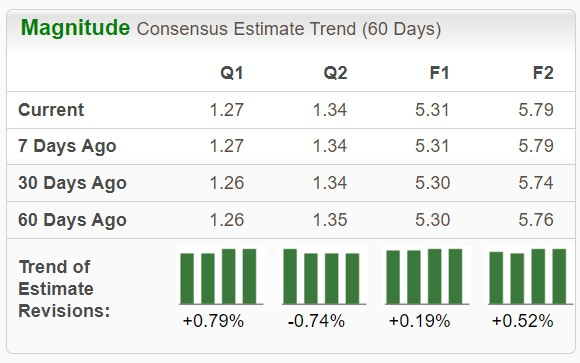

The Zacks Consensus Estimate for first-quarter revenues is pegged at $8.12 billion, indicating an increase of 4.23% from the year-ago quarter’s reported figure.

The consensus mark for earnings stands at $1.27 per share, up by a penny over the past month. However, it indicates for a decline of 4.51% from the figure reported in the year-ago quarter.

Image Source: Zacks Investment Research

Over the trailing four quarters, the company’s earnings per share surpassed the Zacks Consensus Estimate on three occasions and missed in the remaining period, with the average surprise being 7.83%. The graph below depicts this surprise history:

PayPal Holdings, Inc. Price and EPS Surprise

PayPal Holdings, Inc. price-eps-surprise | PayPal Holdings, Inc. Quote

Q1 Earnings Whispers for PYPL

However, our proprietary model does not conclusively predict an earnings beat for PayPal this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

PayPal has an Earnings ESP of -0.08% and a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Factors Shaping PayPal’s Q1 Results

PayPal is evolving into a comprehensive commerce platform, moving far beyond mere payments by leveraging advanced, data-powered tools to accelerate merchant expansion and foster customer loyalty. PYPL’s first-quarter results are expected to benefit from its scale, diversification and balance sheet strength. During the first quarter, the company continued to make progress on its transformation efforts and is likely to have gained from consumers and merchants expanding usage of PayPal.

In the quarter under consideration, PYPL is expected to have benefited from an improving Total Payment Volume (TPV). The metric is likely to have gained from a strong relationship between the company and its merchants and consumers.

Despite strong fundamentals, diversified offerings and strategic moves, PayPal is likely to have faced competitive pressure from other digital payment companies. Broader macroeconomic pressures and uncertainty are likely to have also affected its first-quarter results.

The nature of business makes PayPal vulnerable to foreign exchange fluctuations. A significant part of the company’s operations is international and thus, appreciation or depreciation of the U.S. dollar versus foreign currencies could impact the company’s first-quarter results.

Q1 Projections for PYPL

The Zacks Consensus Estimate for PayPal’s Transaction revenues is pegged at $7.31 billion, which suggests a 4.2% increase from the year-ago quarter.

PYPL is also poised to benefit from its value-added services. Its consensus mark for revenues from other value-added services is pegged at $783.6 million for the first quarter, up 1.1% from the year-ago period.

The consensus mark for TPV is pegged at $447.882 billion, indicating 7.4% year-over-year growth. PayPal’s active accounts are likely to reach 439.8 million, which denotes an increase from the year-ago value of 436 million.

The consensus mark for the number of payment transactions stands at 6.316 billion, which is above the company’s reported figure of 6.045 billion in the same quarter last year.

However, the consensus mark for transaction margin is pegged at 45.89%, down from the year-ago figure of 47.70%.

PayPal anticipated its first-quarter transaction margin (TM) dollars to decline slightly or remain roughly flat, excluding interest on customer balances. The company expected its non-transaction operating expenditure to grow by a mid-single-digit percentage in the first quarter.

PYPL’s Price Performance & Valuation

PayPal shares have gained 22.9% in the past three months. The Zacks Financial Transaction Services has decreased 9.1%, while the S&P 500 has risen 5.5% for the same period. Rivals like Visa Inc. V and Mastercard Incorporated MA continue to expand their offerings, challenging PayPal’s dominance in digital payments.

Compared to its peers, PayPal’s performance has been notably stronger. Visa shares have decreased 0.5%, while Mastercard shares have decreased 9.1% over the same timeframe.

Image Source: Zacks Investment Research

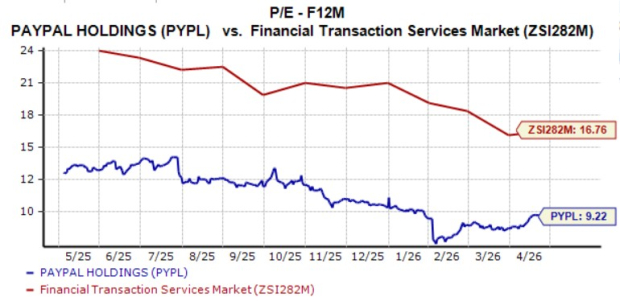

From a valuation standpoint, PayPal shares are trading cheap, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 9.22X compared with the Zacks Financial Transaction Services industry’s 16.76X.

Shares of Visa and Mastercard are currently trading at P/E of 23.45X and 24.10X, respectively.

Image Source: Zacks Investment Research

PYPL: Buy, Sell or Hold?

PayPal is transforming from being a simple payment processor into a comprehensive commerce platform. By integrating its services into one unified platform, the company is fostering stronger ties between consumers and merchants. With an emphasis on enhancing user experience, building deeper merchant partnerships, and growing internationally, PayPal is positioning itself for sustained long-term expansion.

Competition in the digital payments space, macroeconomic uncertainty and foreign exchange rate volatility remain as the concerns for the to-be-reported quarter. Although short-term risks exist, they do not overshadow PayPal’s long-term potential. The stock appears to be a buying opportunity on the back of its solid fundamentals and discounted valuation.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).