There was a time when Roku (ROKU) quietly slipped into living rooms as a simple way to stream content – no heavy hardware, just plug in and play. Over the years, it grew from a modest device maker into a full-fledged platform powerhouse, powering smart TVs, shaping ad-driven streaming, and becoming a go-to partner for manufacturers looking to keep things lean and affordable.

Now, an unlikely factor is stepping into the spotlight – soaring memory prices. Across the tech world, rising costs of memory components are squeezing hardware margins and forcing companies to rethink design and pricing. But Roku seems to be playing a slightly different game.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

During its Q1 earnings call last week, CEO Anthony Wood pointed out something subtle yet strategic. Roku’s operating system requires less memory and storage than competing platforms. That efficiency creates an edge, in essence, a bill-of-materials advantage, especially as component costs climb.

In a market where every dollar of hardware cost matters, that small design choice could turn into a big advantage, positioning Roku as a surprising winner in a high-cost environment.

About Roku Stock

Headquartered in San Jose, Roku has played a defining role in bringing streaming into the mainstream. With a market cap of $18.2 billion, it operates at the intersection of viewers, content creators, and advertisers through its streaming players, Roku TV™, and smart home devices.

Now one of the top TV streaming platforms across the U.S., Canada, and Mexico by hours streamed, Roku continues to expand globally through licensing partnerships with TV manufacturers and service providers. Alongside its hardware, it runs The Roku Channel and other streaming services, steadily shaping the future of connected entertainment.

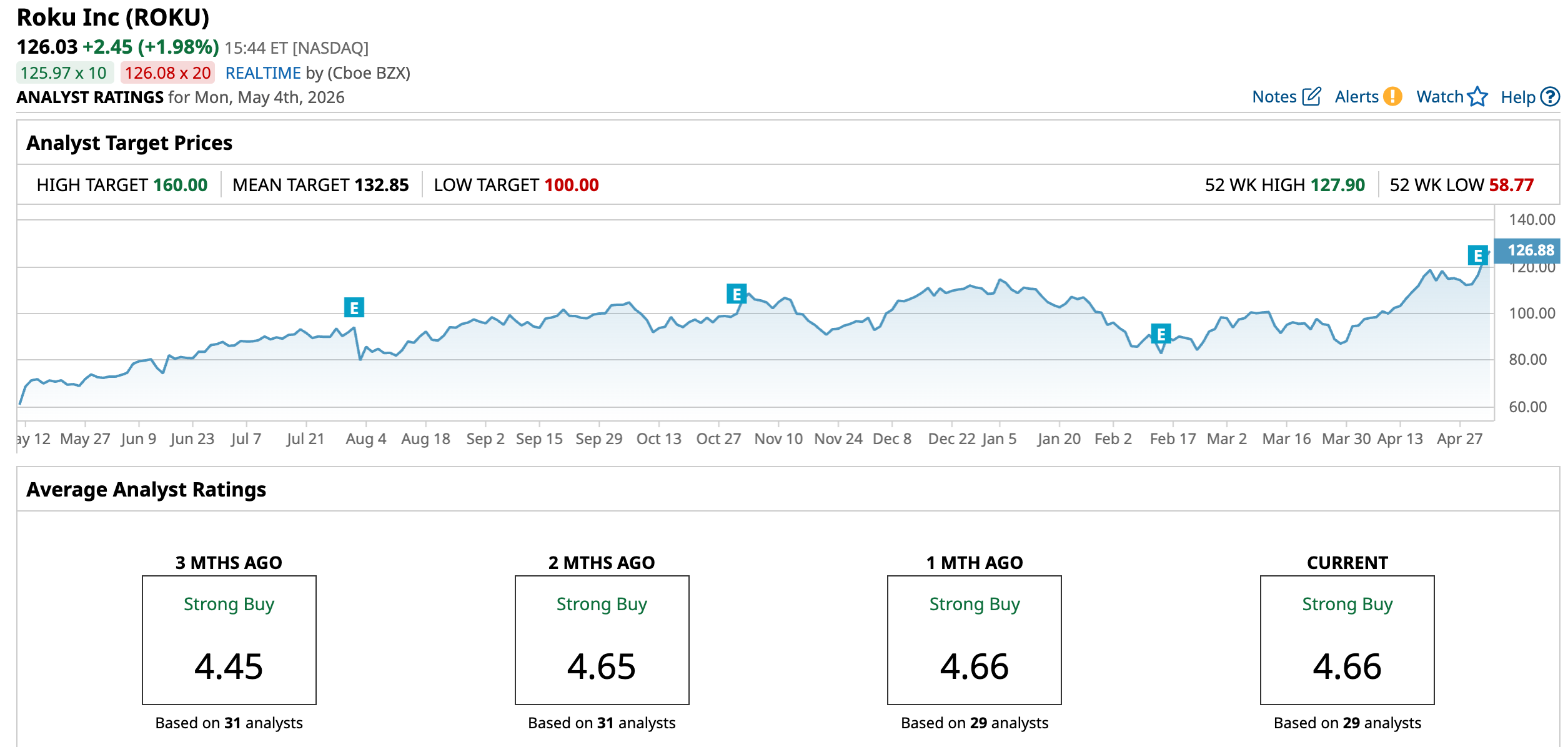

ROKU stock has been on a pretty strong streak. After its Q1 results landed well with investors, the stock ran up to a year-to-date (YTD) high of $127.90 on May 4. It has slipped slightly since then – down 0.84% – but that barely dents the bigger picture. Over the past 52 weeks, the stock has climbed 105.56%, and it is still up 16.62% so far this year. What really stands out is the recent momentum. Roku has jumped 29.56% in just the past month and added another 10.62% in the last five trading days, showing clear buying interest.

Technically, things are getting a bit stretched. The 14-day RSI is sitting at 73.42, signalling overbought territory. Still, the MACD remains positive, suggesting the upward trend has not lost steam just yet.

www.barchart.com

www.barchart.com From a valuation standpoint, ROKU is not exactly cheap, but it is not stretched either. It is priced at 3.29 times forward sales, slightly above peers, which suggests that investors are still willing to pay a premium for its growth story. Meanwhile, it is sitting below its own historical average, so it is not as overheated as it once was. ROKU is essentially priced with optimism, but not excess. So that leaves room if the growth story continues to play out.

Roku Beats Q1 Estimates

Roku started fiscal 2026 Roku stared fiscal 2026 on a powerful note, reporting impressive first-quarter results on April 30. The market responded quickly, and shares climbed about 6% the following day as the company delivered stronger-than-expected numbers. Revenue rose 22.4% year-over-year (YOY) to $1.25 billion, while profitability showed a sharp turnaround. Earnings came in at $0.57 per share, a notable swing from the -$0.19 per-share it posted a year ago.

Platform revenue jumped 28.4% annually to $1.13 billion, comfortably ahead of the company’s expectations, powered by major events like the Olympics and the Super Bowl that drove subscription activity and media spending. Devices revenue, on the other hand, dropped 15.9% YOY to $117.6 million. Even so, that’s largely by design. Roku continues to treat hardware as a gateway, not a profit center. Despite a $19.1 million gross loss in the Devices segment, overall gross profit climbed 27% YOY to $565 million, with Platform gross profit reaching $584.1 million.

Meanwhile, adjusted EBITDA surged 165% YOY to $148 million, translating to a 12% margin. Free cash flow over the trailing twelve months stood at $538.8 million, signaling improving financial strength.

Scale is no longer a question for Roku. The platform now reaches over 100 million active streaming households, accounting for more than half of U.S. streaming homes. Engagement remains solid too, with streaming hours rising 8% to 38.7 billion. The Roku Channel has emerged as a major player, ranking as the second most engaged app on the platform in the U.S.

Roku is also sharpening its monetization strategy. Its open, programmatic ad model continues to gain traction through partnerships with players like Amazon DSP, The Trade Desk, and a new integration with DV360. Plus, with the growth in premium subscriptions, international expansion, and early success from a redesigned home screen, the company is steadily deepening its revenue streams.

Then there’s the broader industry backdrop of rising memory costs. Roku acknowledged that tighter DRAM supply and pricing pressure will weigh on Device margins in the second half of 2026. But this is the point at which its design philosophy starts to matter. As CEO Anthony Wood has highlighted, Roku’s operating system runs on significantly less memory than competing platforms.

So, in an environment where memory prices have surged dramatically due to AI-driven demand, that efficiency could become a real advantage. Roku believes this widening cost gap will attract more TV OEM partners, and it is already expanding licensing agreements, with new partnerships expected to contribute to unit volumes later this year.

Looking ahead, the management estimates platform revenue to grow about 20% annually, while Devices revenue may decline by high single digits. That should still push total quarterly revenue to around $1.3 billion, up nearly 17%, alongside $580 million in gross profit and $170 million in adjusted EBITDA.

For fiscal 2026, the management is targeting roughly $5 billion in platform revenue, up about 21% YOY, total revenue of $5.5 billion. Margins on the Platform side are likely to sit at the upper end of the 51% to 52% range, while Devices margins are expected to stay in the high -20% zone. Adjusted EBITDA is anticipated to be $675 million, implying margin expansion of about 330 basis points.

Even with higher memory costs baked in, the company is holding its overall Devices investment steady. With operating expenses expected to grow in the mid-single digits and remain weighted toward the second half, Roku still sees a clear path forward. Plus, management feels confident that the company can keep delivering solid double-digit Platform growth, and is still eyeing that $1 billion free cash flow mark by 2028, maybe even sooner.

Analysts tracking Roku predict profit to be $0.36 per share in Q2, with revenue hitting $1.3 billion. Over the longer term, EPS is estimated to be $2.24 in fiscal 2026, up 279.66% YOY, and then rise by another 48.2% annually to $3.32 in fiscal 2027.

What Do Analysts Expect for Roku Stock?

After Roku’s strong Q1 print, several brokerage firms wasted no time lifting their price targets, and the tone has clearly turned more confident. Evercore ISI bumped its target to $160 from $150, sticking with an “Outperform” rating and pointing to the better-than-expected results.

Piper Sandler set a $148 target, raising it from $140, with analyst Thomas Champion keeping an “Overweight” rating and hinting that Roku’s second-half outlook might actually be conservative. The view there is that execution has been solid, and momentum could carry forward.

KeyBanc’s Justin Patterson also increased the target from $140 to $150 and also maintained an “Overweight” rating, saying the quarter reinforced confidence in Roku’s multiple growth levers. He sees improving margins and FCF as a meaningful turning point.

Needham raised its price target to $140 and pointed to Roku’s massive base of over 100 million streaming households and its role as a key gatekeeper in TV monetization. It also highlights Roku’s lower-memory OS as a quiet advantage, especially as rising memory costs push more TV makers toward its platform. Adding its scale of first-party data and premium content, Roku starts to look especially valuable in an AI-driven ad world.

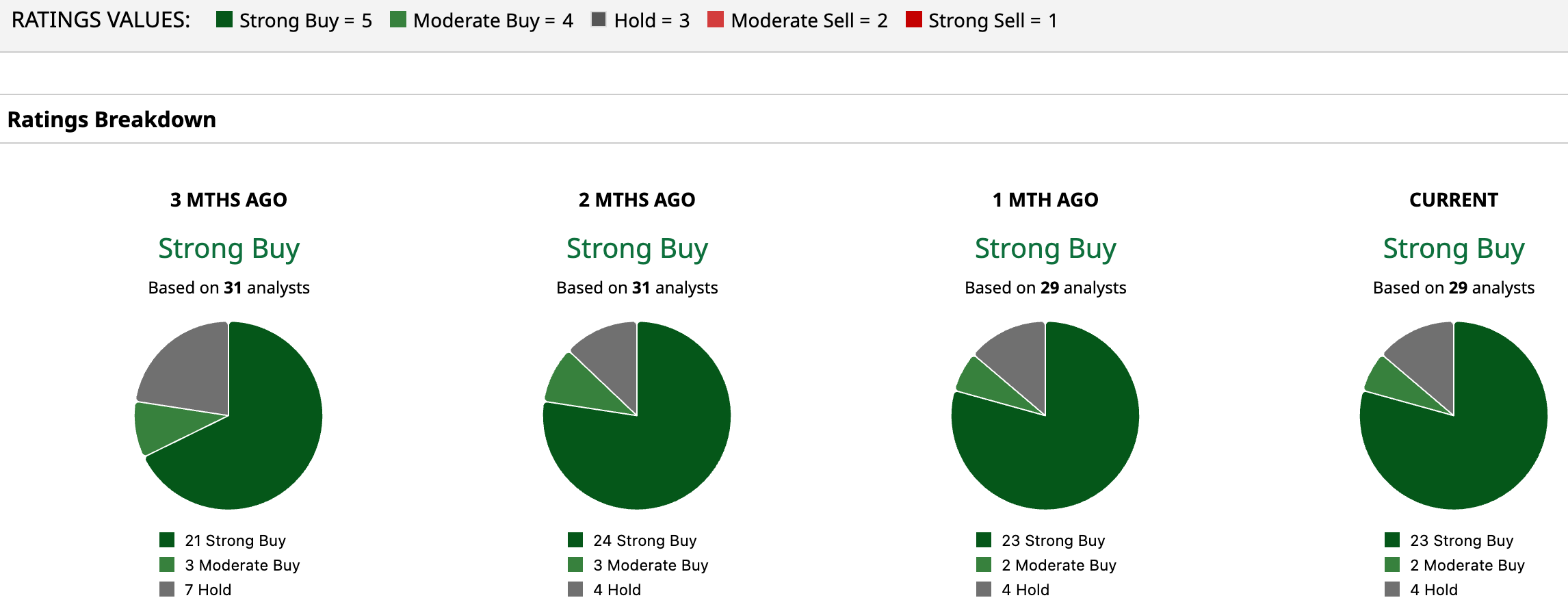

Wall Street seems firmly on Roku’s side, with the stock carrying a consensus “Strong Buy” rating. Of the 29 analysts covering the stock, 23 are all-in with a “Strong Buy,” two advise a “Moderate Buy,” and four are playing it safe with a “Hold” rating.

The average analyst price target of $132.85 hints at 5.4% upside potential, but the boldest forecasts shoot for $160 – signaling that the stock could surge as much as 27%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Final Thoughts on ROKU Stock

At first glance, rising memory costs look like just another industry headache, but for Roku, the story is a bit more layered. Yes, device margins could feel the pressure in the latter half of 2026, something management has already flagged. But that’s only one side of the equation. The bigger picture lies in how Roku is positioned.

Roku’s real strength lies in its platform-first model. Its OS runs on far less memory – sometimes as low as 512MB on entry devices – giving it a meaningful bill-of-materials advantage. As costs rise across the industry, that gap only widens, making Roku increasingly attractive to TV OEM partners like TCL and Hisense, which already drive the bulk of its user base, ultimately feeding into its higher-margin platform business.

That matters because platform revenue from ads, subscriptions, and billing accounts for over 90% of its business. So even if hardware takes a hit, growing partnerships and installations could more than offset it. In that sense, what looks like a cost challenge today could quietly turn into a long-term growth tailwind for Roku.

If the dynamic holds, it could steadily support ROKU stock, with platform-driven growth and expanding partnerships potentially keeping the longer-term trajectory tilted to the upside, despite near-term margin noise.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Latest Changes to the Clarity Act Are Sending Circle Stock Higher Today. Here's Why. Dear Western Digital Stock Fans, Mark Your Calendars for June 5 Ahead of Palantir Earnings, Here Is What Barchart Options Data Shows for PLTR Stock How ROKU Stock Could Be One of the Biggest Winners of Sky-High Memory Prices