Applied Digital APLD shares are overvalued, as suggested by a Value Score of F. The stock is trading at a premium, with a forward 12-month Price/Sales (P/S) of 16.98X compared with the Zacks Financial - Miscellaneous Services industry’s 3X and the Zacks Finance sector's 8.82X. Among its peers, RIOT Platforms RIOT and Equinix EQIX are trading at comparatively lower multiples of 13.43X and 10.1X, respectively.

The premium valuation reflects Applied Digital’s existing positioning within the AI infrastructure segment, though a meaningful portion of the longer-term narrative already appears reflected in the stock. The higher multiple largely stems from APLD’s growing hyperscale AI data center platform, expanding development pipeline and increasing exposure to long-duration infrastructure contracts tied to rising AI compute demand.

APLD’s P/S F12M Ratio

Image Source: Zacks Investment Research

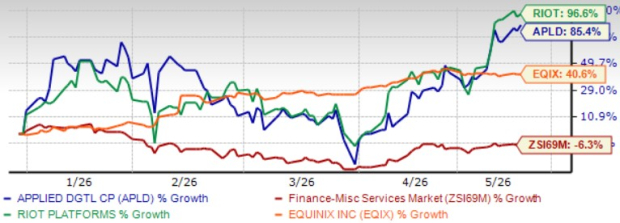

On a year-to-date basis, APLD shares have risen 85.4%, well above the sub-industry, which has declined 6.3%. RIOT Platforms has surged 96.6% while Equinix has advanced 40.6% year to date. APLD's outperformance reflects expectations surrounding its rapidly expanding hyperscale AI infrastructure platform and growing long-term revenue visibility.

APLD’s YTD Performance

Image Source: Shutterstock

So how should investors approach APLD at this stage? Let's take a closer look.

AI Infrastructure Expansion Fuels Revenue Visibility for APLD

APLD's expanding campus portfolio is beginning to translate long-term lease commitments into visible recurring revenues. Revenues rose 139% year over year in the third quarter of fiscal 2026, driven by the first full quarter of base rent recognition from the operational 100 megawatt facility at Polaris Forge 1. Additional capacity at Polaris Forge 1 and Polaris Forge 2 is expected to ramp through fiscal 2027, supporting revenue diversification across multiple hyperscale customers.

Delta Forge 1 further extends the company’s development pipeline into a new geography. Following the separation of the cloud business into ChronoScale Corporation, APLD is increasingly focused on scaling its AI data center platform. With approximately one gigawatt of capacity across four actively marketed sites, the contracted revenue base has meaningful room to grow beyond the current $16 billion.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $395.4 million, up 83.48% year over year. The consensus loss estimate of 61 cents per share has widened by 9 cents over the past 30 days, reflecting near-term construction cost pressure. However, this represents an improvement of 23.75% over the fiscal 2025 loss, suggesting the platform's earnings trajectory remains directionally positive. RIOT Platforms and Equinix continue expanding AI and digital infrastructure capabilities as well, though APLD remains earlier in its hyperscale monetization cycle.

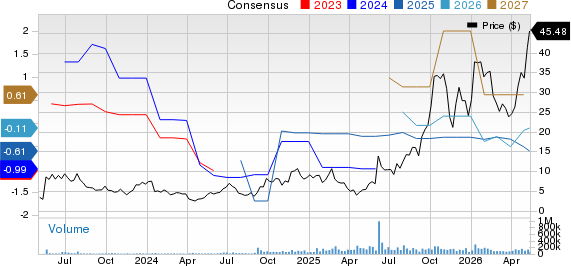

Applied Digital Corporation Price and Consensus

Applied Digital Corporation price-consensus-chart | Applied Digital Corporation Quote

Balance Sheet Strength Anchors APLD's Construction Phase

APLD ended the third quarter of fiscal 2026 with $2.1 billion in cash and equivalents against $2.7 billion in total debt, with no material maturities due within the next two years. The liquidity position provides flexibility to continue funding its ongoing campus buildout during a highly capital-intensive expansion phase.

The $2.15 billion Senior Secured Notes offering at 6.75% due 2031 funds Polaris Forge 2, while the $100 million DevCo Facility with Macquarie Equipment Capital supports Delta Forge 1 development costs. Access to $4.1 billion in preferred equity commitments from Macquarie Asset Management, contingent on executed investment-grade leases, preserves over 85% common equity ownership for shareholders at each new campus.

CoreWeave’s CRWV SPV tenant subsidiary securing an A3 credit rating also improved the credit profile attached to Polaris Forge 1 lease agreements. Over time, stabilized assets and improving financing structures could support lower borrowing costs, particularly as additional campuses begin contributing recurring lease revenues.

APLD Faces Customer Concentration and Execution Risk

Despite improving customer diversification, CoreWeave remains APLD’s largest hyperscale exposure and still accounts for roughly $11 billion of the company’s $23 billion in contracted lease revenues. While additional investment-grade hyperscaler agreements at Polaris Forge 2 and Delta Forge 1 have reduced concentration risk, dependence on CoreWeave remains an important factor to monitor.

APLD is simultaneously managing large-scale construction across multiple campuses, advancing utility agreements and pursuing lease negotiations across remaining development sites. Each workstream carries its own timeline risk, and a delay in any one of them could slow the revenue ramp the market is currently pricing in. Consistent delivery across a complex, multi-campus construction program remains the central variable that will ultimately determine whether the growth case plays out as projected.

Conclusion

Applied Digital remains well-positioned within one of the fastest-growing areas of digital infrastructure, supported by expanding hyperscale AI data center capacity, improving revenue visibility and sufficient liquidity to fund its ongoing construction pipeline. The company is executing against a large multi-campus opportunity set, though elevated valuation, customer concentration and execution risks continue limiting near-term upside visibility after the stock’s strong rally.

APLD currently carries a Zacks Rank #3 (Hold). Existing investors may consider maintaining their positions, while new investors could benefit from waiting for a more favorable entry point. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Equinix, Inc. (EQIX): Free Stock Analysis Report

Riot Platforms, Inc. (RIOT): Free Stock Analysis Report

Applied Digital Corporation (APLD): Free Stock Analysis Report

CoreWeave Inc. (CRWV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).