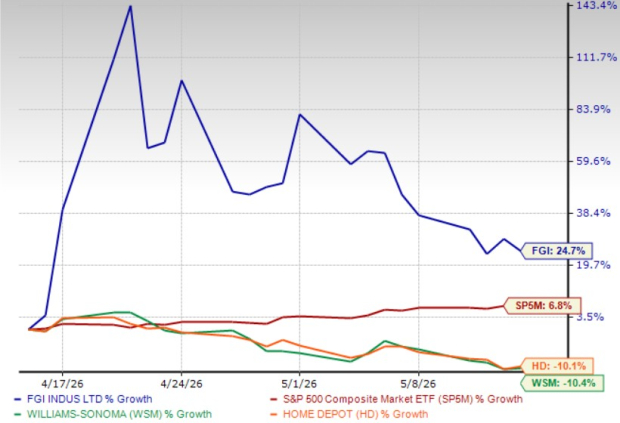

FGI Industries Ltd. FGI stock has surged 24.7% in the past month, against the industry’s decline of 8.6%. The stock has even overshadowed the S&P 500’s rally of 6.8% in the same time period.

The company’s focus on improving its long-term fundamentals despite near-term macroeconomic pressures bodes well. FGI reported weaker fourth-quarter 2025 sales, the market appears encouraged by expanding margins, international growth opportunities and management’s positive 2026 outlook.

Investor sentiment also improved after management highlighted strong momentum entering 2026. During the latest earnings call, executives said new customer programs, dealer expansion and sourcing diversification efforts continue to support the business despite ongoing tariff uncertainty. The company’s ability to maintain operational stability during a volatile period likely strengthened confidence in its long-term strategy.

In the past month, the stock has also outpaced industry players like Williams-Sonoma, Inc. WSM and The Home Depot, Inc. HD, as shown in the chart below.

Price Performance

Image Source: Zacks Investment Research

Margin Expansion & Global Growth Initiatives Support the Rally

One of the strongest positives from the quarter was FGI’s margin improvement. Although fourth-quarter 2025 revenues declined 14.4% year over year to $30.5 million, gross margin expanded sharply to 26.7% from 24.6% a year earlier. Management attributed the improvement to better performance from higher-margin businesses and operational efficiencies. Investors often reward companies that demonstrate stronger profitability trends even during slower sales periods.

FGI’s full-year performance also remained relatively resilient despite tariff-related disruptions. Management noted that both revenues and gross profit declined less than 1% for the full year, reflecting stability across the broader business. The company’s focus on brands, products and channels strategy appears to be helping strengthen its competitive position.

Another major growth driver is India. CEO David Bruce highlighted rapid dealer additions in Mumbai while noting that the company is gradually expanding into Delhi through new distributors and dealers. Investors may view India as a meaningful long-term opportunity, given the country’s growing demand for housing and renovation.

FGI is also broadening its international footprint beyond India. The company said its wholesale bath initiative in Germany has performed well over the past several months, supported by a newly established distribution center. These expansion efforts could diversify revenue sources and reduce dependence on slower markets.

Another encouraging factor is FGI’s China Plus One sourcing strategy. Management confirmed that it has secured additional partnerships outside China, including in Thailand, to reduce supply-chain risks and tariff exposure. This diversification could improve long-term operational flexibility.

Still, risks remain. Tariff uncertainty, geopolitical tensions and uneven consumer demand could continue to impact ordering patterns. Management acknowledged that customers paused some purchases during 2025 due to shifting trade policies.

FGI’s Bottom Line Improves

FGI’s loss estimates for 2026 have narrowed sharply in the past 30 days. The company is expected to deliver a loss per share of 27 cents in fiscal 2026, compared with the reported figure of a loss of $3.20 in 2025. FGI’s top line in 2026 is likely to witness growth of 5.3%.

Image Source: Zacks Investment Research

On the other hand, Williams-Sonoma and The Home Depot earnings in the current year are likely to witness growth of 4.8% and 2.3% year over year, respectively.

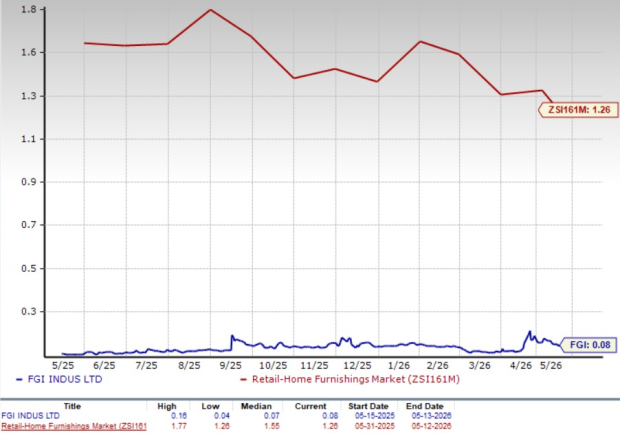

FGI Trades at a Discount

FGI Industries is trading at a discount on a forward 12-month price-to-sales (P/S) ratio basis. Its forward 12-month P/S ratio stands at 0.08X, lower than the industry. This indicates that despite the recent stock price increase in the past month, it remains an attractive option for investors looking for a discounted entry point.

FGI P/S Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Wrapping Up

FGI Industries appears increasingly attractive for investors because it is showing signs of operational improvement despite a challenging macroeconomic environment. Expanding margins, improving earnings trends, international expansion in markets like India and Germany, and diversification away from China are strengthening its long-term growth profile.

Management’s confidence in new customer programs, dealer additions and sourcing flexibility also suggests the business is building a more resilient foundation. In addition, the stock still trades at a discounted valuation compared with industry peers, indicating the recent rally may still have room to continue if the company executes well on its growth initiatives and profitability strategy.

The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Home Depot, Inc. (HD): Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

FGI Industries Ltd. (FGI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).