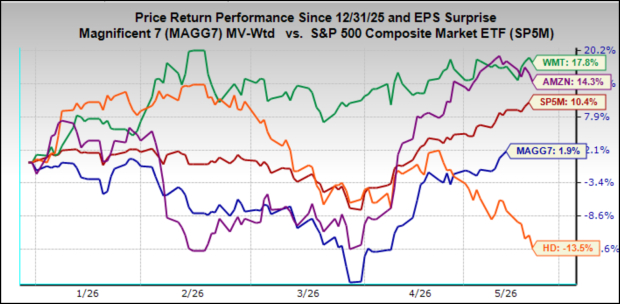

Walmart WMT shares have been standout performers this year, handily outperforming not just the broader market indexes but also the likes of Amazon AMZN and many members of the Magnificent 7 group.

Walmart and other big-box retailers are undoubtedly facing a difficult operating environment, with elevated fuel costs not only adding to consumers’ financial burdens but also increasing the retailers’ expenses.

Walmart is better positioned than many others in the space, given its value orientation, greater indexing to groceries, and robust digital capabilities. Walmart has been consistently gaining market share among higher-income households in recent years, more than offsetting affordability-based demand softness among its lower-income consumers. With all of these positive attributes still very much in place, we expect Walmart shares to sustain their recent momentum following quarterly results on Thursday, May 21st.

The chart below shows the year-to-date performance of Walmart shares (green line, up +17.8%) relative to the Mag 7 group (blue line, up +1.9%), the S&P 500 index (red line, up +10.4%), Amazon (purple line, up +14.3%) and Home Depot HD shares (bottom line in the chart, down -13.5%). Home Depot reports results before the market’s open on Tuesday, May 19th.

Image Source: Zacks Investment Research

Walmart has a large and growing digital operation, but its merchandise remains heavily weighted toward groceries and other essential, must-have items.

This orientation towards essentials, coupled with Walmart’s well-earned reputation for low prices, provides the company’s results with a high degree of cyclical stability and hence the stock’s defensive attributes. Walmart’s value orientation has been a key contributing factor to the company’s ability to gain market share among high-income households. The company’s growing digital offerings also contribute to that trend. Growth in e-commerce, coupled with gains from third-party fulfillment and advertising, are some of the other areas that will benefit results this quarter.

Walmart is expected to report $0.65 in EPS on $174.07 billion in revenues, representing year-over-year changes of +6.6% and +5.1%, respectively. Estimates have been stable, though they have modestly come down since the quarter got underway.

In terms of same-store sales, the expectation is U.S. comps (ex fuel) of +3.86%, which will compare to a +4.6% gain in the preceding quarter (vs. expectations of +4.24%) and a +4.5% gain in the year-earlier period (vs. expectations of +3.9%). A positive general merchandise read will also have positive read-throughs for Target.

Same-store sales at Home Depot are expected to be flat (0% growth) when it reports results on Tuesday, May 19th. Comps at Home Depot have been positive for the last four quarters, though the gains were modest at +0.3% and +0.1% in each of the last two quarters. The stock’s underperformance is a reflection of the housing market’s challenges, with continued soft demand for home improvement projects and big-ticket appliances.

With respect to the Retail sector 2026 Q1 earnings season scorecard, we now have results from 17 of the 31 retailers in the S&P 500 index. Regular readers know that Zacks has a dedicated stand-alone economic sector for the retail space, unlike its placement in the Consumer Staples and Consumer Discretionary sectors in the Standard & Poor’s standard industry classification.

The Zacks Retail sector includes not only Walmart, Home Depot, and other traditional retailers, but also online vendors like Amazon AMZN and restaurant players. The 17 Zacks Retail companies in the S&P 500 index that have reported Q1 results already belong mostly to the ecommerce and restaurant industries, though we have a number of restaurant companies on deck to report results this week as well.

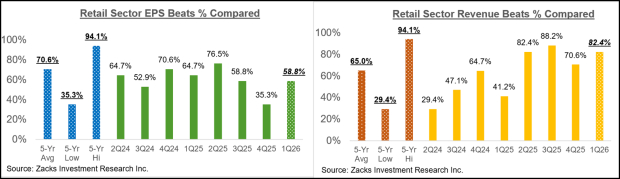

Total Q1 earnings for these 17 retailers that have reported are up +1.9% from the same period last year on +13.9% higher revenues, with 58.8% beating EPS estimates and 82.4% beating revenue estimates.

The comparison charts below put the Q1 beats percentages for these retailers in a historical context.

Image Source: Zacks Investment Research

As you can see above, the EPS beats percentages for these online players and restaurant operators are tracking significantly below the historical averages for this group of companies, but revenue beats are far more numerous.

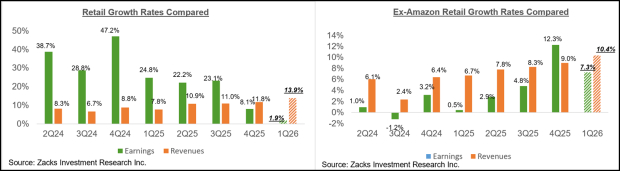

With respect to the earnings and revenue growth rates at this stage, we like to show the group’s performance with and without Amazon, whose results are among the 17 companies that have already reported. As we know, Amazon’s Q1 earnings were modestly down (-0.8%) on +16.6% higher revenues, as it missed both EPS and top- line expectations.

The two comparison charts below show the Q1 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart)

Image Source: Zacks Investment Research

As you can see above, earnings for the group outside of Amazon are up +7.3% on a +10.4% top-line gain.

The Earnings Big Picture

The Q1 earnings season reconfirmed the steadily improving earnings outlook we have consistently highlighted in our earnings commentary.

The earnings focus lately has been on the blockbuster mega-cap Tech players in the Magnificent 7 group, but results have been impressive across the board in all sectors. Most companies comfortably beat the Zacks Consensus EPS and revenue estimates and are showing accelerating earnings and revenue growth trends.

Most importantly, the substance and tone of management guidance have largely been reassuring, notwithstanding the uncertain geopolitical backdrop. This is keeping the aggregate revisions trend positive, which we discuss in some detail later on.

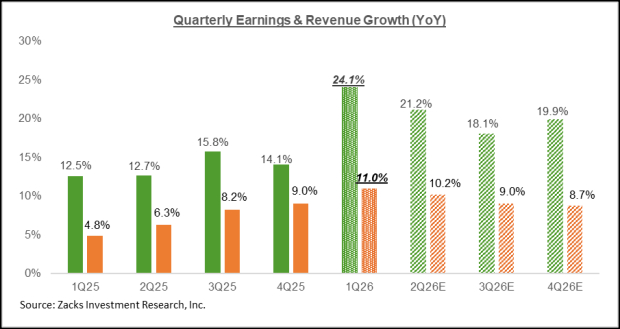

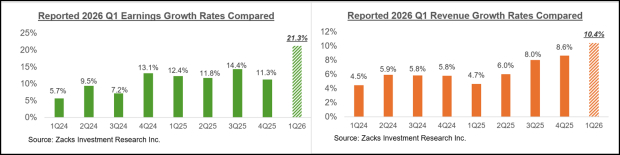

The chart below shows current 2026 Q1 earnings and revenue growth expectations in the context of where growth has been in the preceding five quarters and what is expected in the coming four quarters.

Image Source: Zacks Investment Research

Regular readers of our earnings commentary are familiar with the steadily improving earnings outlook we have consistently highlighted over the past year. This improvement in the earnings outlook has been driven mostly by the Tech sector over the past year, with positive Tech sector estimate revisions offsetting negative revisions elsewhere, keeping the aggregate revisions trend in the neutral-to-positive direction.

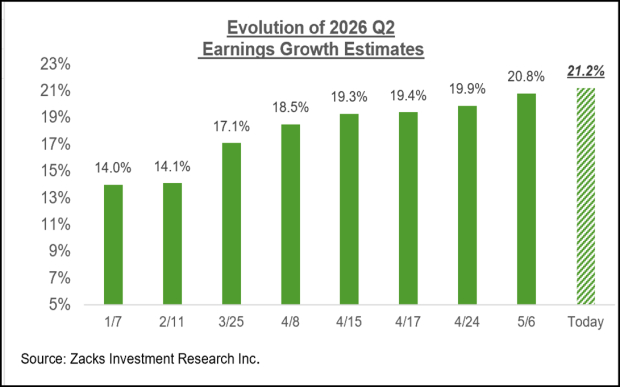

This favorable revisions trend modestly expanded beyond its Tech sector core over the last couple of quarters, and we are seeing that at play in 2026 Q2 as well, as shown nearby.

As you can see in the above chart, the current expectation is of +21.2% earnings growth in 2026 Q2 on +10.2% higher revenues. The chart below shows how these expectations have evolved in recent weeks.

Image Source: Zacks Investment Research

Estimates have moved higher for 7 of the 16 Zacks sectors since the quarter got underway. These sectors are: Tech, Energy, Basic Materials, Utilities, Industrials, Retail, and Business Services.

The positive revisions trend for the Energy and Basic Materials sectors is primarily a function of the conflict in the Persian Gulf and its effect on the supply of oil, LNG, and other commodities.

The upgrade to Retail sector earnings estimates is primarily a function of momentum in Amazon’s (AMZN) business, which we group in the Zacks Retail sector. We suspect that elevated oil prices will prove to be a significant headwind for the sector’s profitability. The negative impact on the Retail sector’s earnings outlook will mostly be through diminished consumer demand, but high oil prices will also stress the freight/logistics component.

On the negative side, Q2 estimates have declined for 9 of the 16 Zacks sectors. The sectors suffering the most declines include Transportation, Autos, Consumer Discretionary, Construction, Finance, and Consumer Staples.

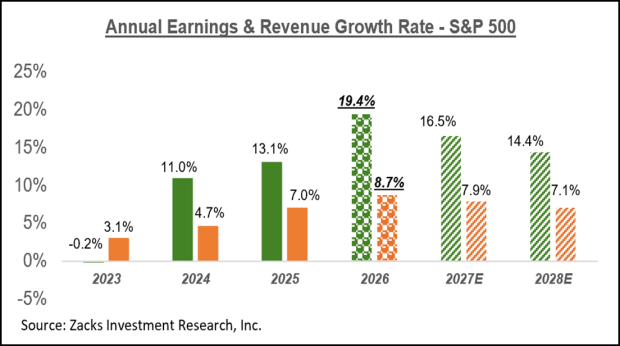

For calendar year 2026, total S&P 500 earnings are currently expected to be up +19.4%, compared to +13.1% earnings growth last year and +16.4% expected next year.

All 16 Zacks sectors are currently expected to enjoy positive earnings growth in 2026, a development that we haven’t seen in a very long time. The Tech and Energy sectors are big contributors to earnings growth in 2026, with +33.9% and +60% earnings growth, respectively.

Excluding the Energy sector’s substantial contribution, 2026 earnings growth for the rest of the index would +17.5% (vs. +19.4% otherwise. Excluding the Tech sector, index earnings would be up +11.9% in 2026.

The chart below shows the aggregate growth picture on an annual basis.

Image Source: Zacks Investment Research

2026 Q1 Earnings Season Scorecard

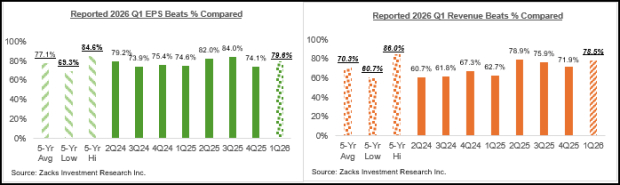

Through Friday, May 15th, we have seen Q1 results from 456 S&P 500 members or 91.2% of the index’s total membership. Total earnings for these 456 index members are up +21.3% from the same period last year on +10.4% higher revenues, with 79.6% beating EPS estimates and 78.5% beating revenue estimates.

We have more than 100 companies on deck to report Q1 results this week, including 17 S&P 500 members. The notable companies reporting this week include Nvidia, Walmart, Home Depot, Deere & Company, Target, and Toll Brothers.

The comparison charts below compare the growth rates of the companies that have reported with what we have seen from this same group of companies in other recent periods.

Image Source: Zacks Investment Research

The comparison charts below put the Q1 EPS and revenue beats percentages for this group of companies relative to what we had seen from them in other recent periods.

Image Source: Zacks Investment Research

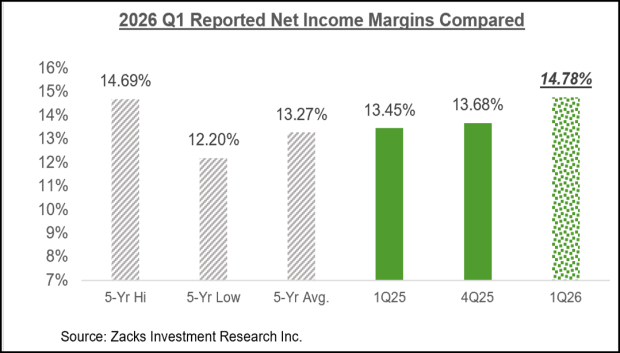

The chart below shows how net margins for the 456 index members that have reported Q1 results compare to other recent periods for this same group of companies.

Image Source: Zacks Investment Research

For a detailed look at the overall earnings picture, including expectations for the coming periods, please check out our weekly Earnings Trends report >>>> Q1 Earnings Season Reconfirms the Positive Earnings Outlook

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

The Home Depot, Inc. (HD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).