The debate around AI spending is now much more practical as investors are no longer impressed by big spending plans alone. They want to see real returns. In the week before Alibaba Group’s (BABA) report, Alphabet’s (GOOG) (GOOGL) $175 billion to $185 billion CapEx plan for 2026 put fresh attention on whether cloud revenue can justify that kind of spending.

Around the same time, big tech earnings showed the sharp split within the market. Alphabet jumped 10% after its results, while META Platforms (META) fell 8.5% and Microsoft Corporation (MSFT) dropped 4%, proving that Wall Street now wants proof that AI spending can actually make money.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That is the backdrop for Alibaba Group’s fiscal fourth-quarter and full-year 2026 results on May 13. The company posted an operating loss of 848 million yuan ($125 million), compared with an operating profit of 28.5 billion yuan in the same quarter last year. Also, the report followed three straight quarterly misses, with the December 2025 quarter alone coming in 48.57% below EPS estimates, the worst earnings miss the stock has seen in quite some time.

Still, on the same earnings call, CEO Eddie Wu pointed investors to what may matter more going forward: “Alibaba's AI has moved beyond the initial investment phase and progressed to commercialization at scale.”

With profits under pressure but AI and cloud growing fast, is Alibaba Group finally reaching the point where years of spending start to pay off for BABA shareholders? Let’s find out.

Breaking Down the Financials

Alibaba Group runs one of China’s biggest online business ecosystems, with operations across e-commerce, cloud computing, logistics, and digital business services.

The stock has not done much lately. It is up 5% over the past 52 weeks but down 3.98% so far this year.

www.barchart.com

www.barchart.comEven so, Alibaba Group still trades at a forward price-to-earnings of 20.13 times, which is above the sector average of 15.25 times. The company also pays a modest dividend. Its yield is 0.70%, its most recent annual payout was $0.95, its forward payout ratio is 19.94%, and it has increased its dividend for just one year.

In the March 2026 quarter, revenue rose 3% year-over-year (YOY) to RMB243.38 billion ($35.28 billion), or 11% on a like-for-like basis. But profit came under heavy pressure. Adjusted EBITA fell 84% to RMB5.1 billion ($740 million), and Alibaba Group swung to an operating loss of RMB848 million ($123 million).

Non-GAAP net income dropped to just RMB86 million ($12 million), down 100%, while earnings per ADS fell 95%. Cash flow also got weaker, with operating cash flow down 66% and free cash flow turning negative at RMB17.3 billion ($2.51 billion), mainly because the company spent more on cloud infrastructure, AI, and bringing in new users.

Commercializing AI and Growth Drivers

In March, Alibaba Group brought all of its AI work into one unit. That includes its large language models, enterprise AI services, and cloud tools. The goal is simple: move faster and turn those products into real business offerings across its large base of merchants and enterprise customers. As part of that change, Alibaba Group also launched a new agentic AI service for businesses that can help vendors handle customer support, marketing, and operations more efficiently.

That push is moving into robotics. Alibaba Group’s mapping unit, Amap, is getting ready to launch its first physical robot, a four-legged machine built to move through real-world environments. The company is working on a humanoid robot that would put it in the same conversation as companies like Tesla.

On the logistics side, Cainiao has already commercially launched ZeeBot, a warehouse robot that can move quickly across floors and climb vertically, reaching five-story racks in 10 seconds. That setup doubles retrieval efficiency and helps warehouses use 40% more storage space.

There is also policy support behind this. China’s “AI+ Manufacturing” action plan is meant to speed up adoption across thousands of smaller industrial companies, which could expand demand for Alibaba Group’s infrastructure and business services. On top of that, Alibaba Group has started testing its “Happy Horse” AI model in beta, which is expected to support more of its products as competition gets tougher.

Analyst Views and Forward Signals

For the June 2026 quarter, estimates are at $1.85 compared to $1.89 last year, down 2.12%. Looking at next quarter fiscal 2026, earnings are projected at $1.54, up 250%.

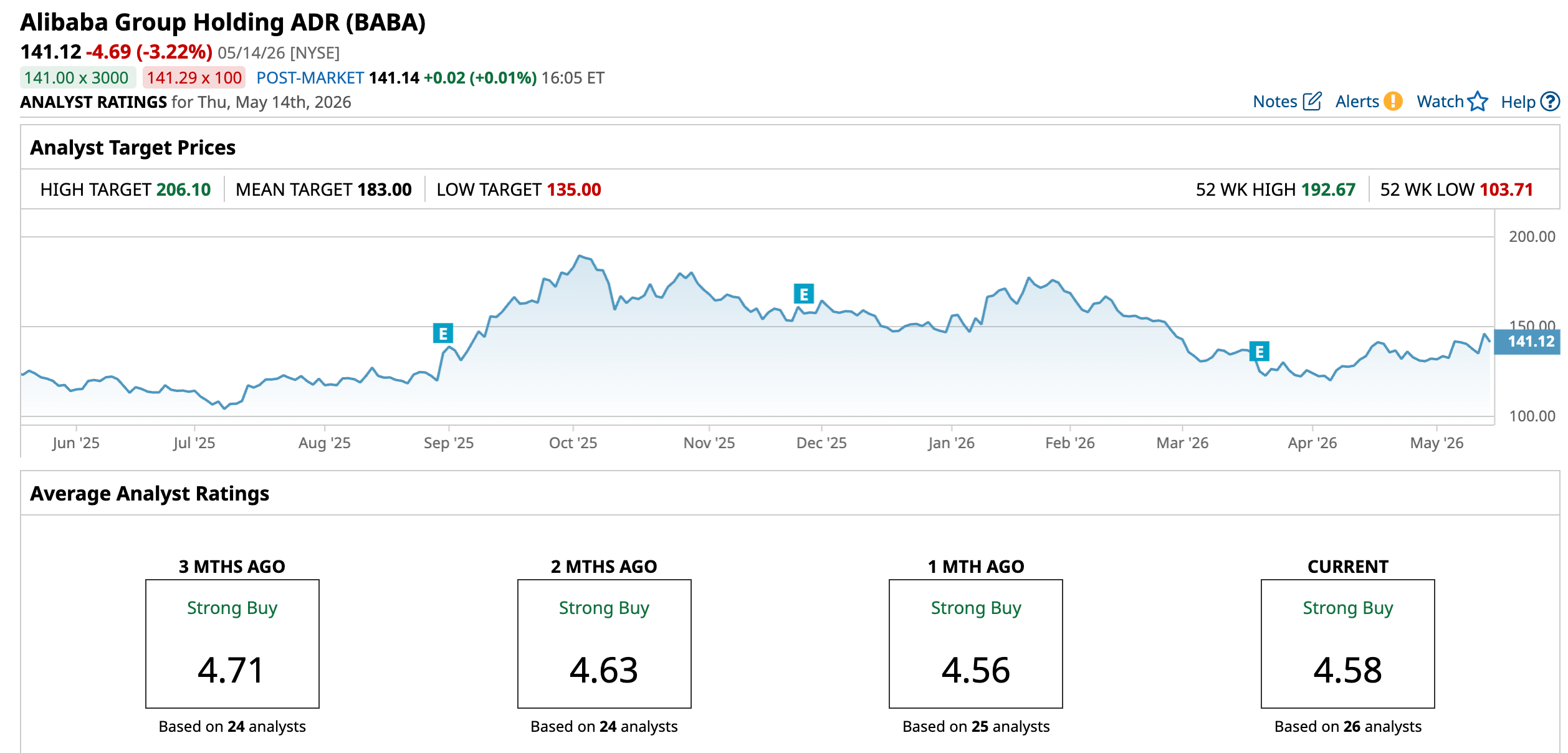

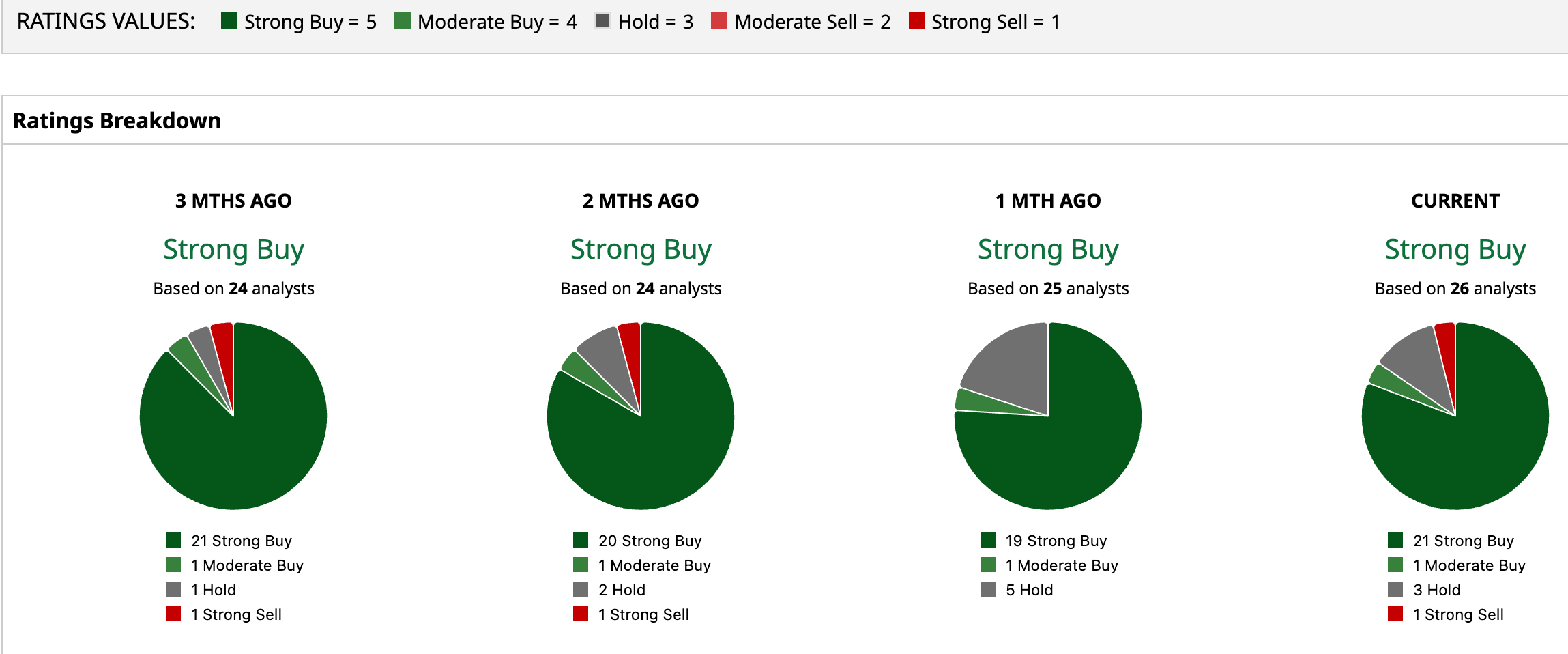

Even with that drop, analysts are not backing away. Jefferies kept its “Buy” rating after Alibaba Group’s fiscal Q3 2026 miss, though it lowered its price target to $212 from $225. Bank of America took a similar view, keeping its “Buy” rating and $180 target while acknowledging the weak earnings, seeing the margin pressure more as a result of heavy investment than a deeper problem.

Overall, Wall Street is still clearly positive. Of the 26 analysts rating the stock, a consensus “Strong Buy,” with the average price target of $183.00 suggests a 29.7% upside from current levels.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

Alibaba’s latest quarter makes the trade-off pretty clear. Near-term earnings took a real hit, but management is no longer asking investors to believe in AI as a distant concept. It is now framing AI as a commercial business tied to cloud, enterprise tools, automation, and even robotics. That does not remove the risk, especially if margins stay under pressure for longer than expected, but it does change the debate around BABA stock. My view is that shares are more likely to trend higher over time if Alibaba can show even modest evidence that AI commercialization is lifting cloud growth and improving monetization, though the path will probably stay volatile in the near term.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Alibaba Profit Fell Sharply, But Full-Stack AI Moved From Incubation to Commercialization. What This Means for BABA Stock. Dell Stock Just Had Its Best Week Since 2024. The Odds of Another Surge Are High. Wix.com Stock Is the Latest Victim of the AI Trade as Shares Plunge Nearly 30% Uber Stock: 3 Reasons Why Analysts See Over 50% Upside Potential