The Home Depot, Inc. HD reported first-quarter fiscal 2026 earnings and revenues that surpassed the Zacks Consensus Estimate. The company posted adjusted earnings of $3.43 per share, reflecting a 3.7% decline from the prior-year quarter but exceeding analysts’ expectations of $3.40. Quarterly revenue increased 4.8% year over year to $41.77 billion, also beating the consensus estimate of $41.49 billion.

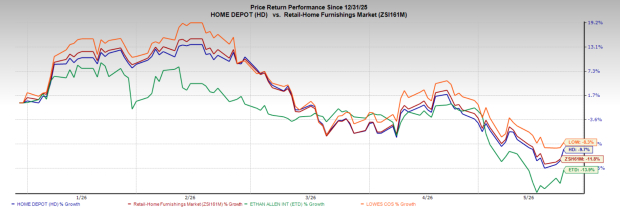

Home Depot, which currently carries a Zacks Rank #3 (Hold), is part of the Zacks Retail - Home Furnishings industry. Its shares have gone down 9.7% year to date compared with a 11.8% decline for the industry. Ethan Allen Interiors Inc. ETD and Lowe's Companies, Inc. LOW, two of HD’s peers from the same industry, have lost 13.9% and 8.3% in the same period, respectively. While Lowe’s also carries a #3, Ethan Allen has a #5 (Strong Sell). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

Industry Faces Housing and Spending Headwinds

The industry has faced a challenging environment year to date, pressured by weak housing activity, elevated interest rates and cautious consumer spending on big-ticket items. Furniture and home furnishings sales have declined in several recent months, with the category underperforming broader retail trends. However, some large players, such as HD and Lowe’s, have shown resilience through stable professional demand and expansion efforts. Despite near-term softness, the industry has modestly outperformed the broader market on a year-to-date basis in stock performance terms.

Management Commentary and Fiscal 2026 Outlook

CEO Ted Decker stated that the company’s first-quarter results aligned with expectations, with underlying business demand remaining largely consistent with trends seen throughout fiscal 2025 despite rising consumer uncertainty and housing affordability pressures. He also highlighted the strong customer service delivered by associates during the quarter and acknowledged their continued dedication and hard work.

HD operated 2,361 retail stores and more than 1,280 SRS locations across North America and employed over 470,000 associates at the end of the first quarter. For fiscal 2026, the company reaffirmed expectations for modest sales and earnings growth, stable comparable sales, about 15 new stores, operating margins near 13%, capital spending equal to roughly 2.5% of sales and net interest expense of approximately $2.3 billion.

Valuation Metrics Suggest Balanced Risk-Reward

HD has a forward 12-month P/E ratio of 20.14, slightly above the industry average of 18.26. This indicates investors expect somewhat stronger earnings stability and long-term growth from Home Depot than from many peers.

Image Source: Zacks Investment Research

It also has a PEG ratio of 3.49, well above the industry average of 1.11, indicating the stock may be expensive relative to its expected earnings growth. However, the premium valuation is not large enough to signal overvaluation. On the contrary, based on short-term price targets offered by 32 analysts, the average fair price target for Home Depot comes to $395.72. The forecasts range from a low of $300.00 to a high of $454.00. It is currently valued at $310.58.

EPS Surprise History Reflects Stable Execution

HD has delivered a mixed but generally stable EPS surprise trend over the last four quarters. The company beat earnings estimates in the most recent two quarters, including a strong 7.94% surprise in the first quarter, indicating resilient execution despite housing market pressures. However, it slightly missed expectations in the prior two quarters, suggesting growth challenges. Overall, the recent earnings history points to steady operational performance rather than strong, accelerating momentum.

Should You Buy, Hold or Wait?

Home Depot appears more suitable for a hold or gradual accumulation strategy than an aggressive buy. This is also in line with its current Zacks Ranking. The company continues to deliver resilient earnings, stable demand and solid execution despite housing market weakness and cautious consumer spending. While analyst price targets suggest meaningful upside from current levels, HD’s elevated PEG ratio indicates the stock may be expensive relative to expected growth. Its slightly premium valuation and mixed EPS surprise trend also suggest limited near-term momentum. Existing investors may continue holding, while new investors could wait for improved housing conditions or a better entry point.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lowe's Companies, Inc. (LOW): Free Stock Analysis Report

The Home Depot, Inc. (HD): Free Stock Analysis Report

Ethan Allen Interiors Inc. (ETD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).