Nvidia (NVDA) just delivered another solid quarter, beating Wall Street expectations as soaring artificial intelligence (AI) demand continued to drive explosive growth across its data-center business.

Despite the strong earnings report, the market’s initial reaction remained surprisingly muted. However, Nvidia’s long-term momentum appears far from over. Surging demand, next-generation chip launches, and expanding growth opportunities could continue to drive strong growth in the coming quarters, pushing NVDA stock higher.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

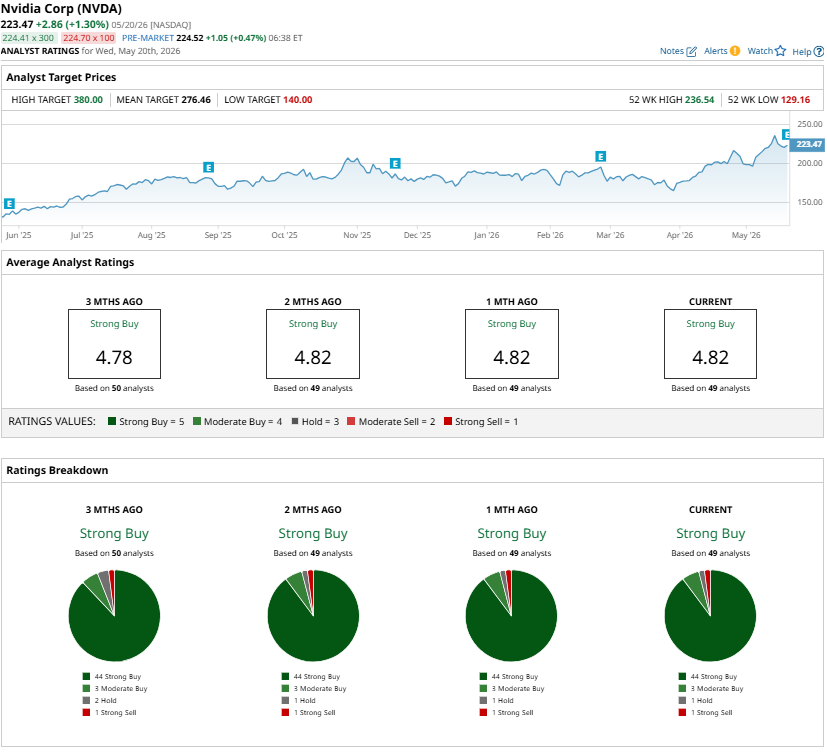

Wall Street analysts remain bullish on Nvidia following its first-quarter results, maintaining a “Strong Buy” consensus rating. Moreover, the Street’s highest price target of $380 implies 70% potential upside from NVDA stock’s May 20 closing price of $223.47.

www.barchart.com

www.barchart.com Nvidia’s AI Empire Is Expanding Beyond GPUs

Nvidia’s rally has largely been driven by its dominance in AI GPUs. However, what began as a GPU-led AI infrastructure cycle is evolving into a full-stack compute expansion, and Nvidia is positioning itself to capture a much larger share of enterprise and hyperscale spending. This could dramatically increase Nvidia’s long-term revenue opportunity.

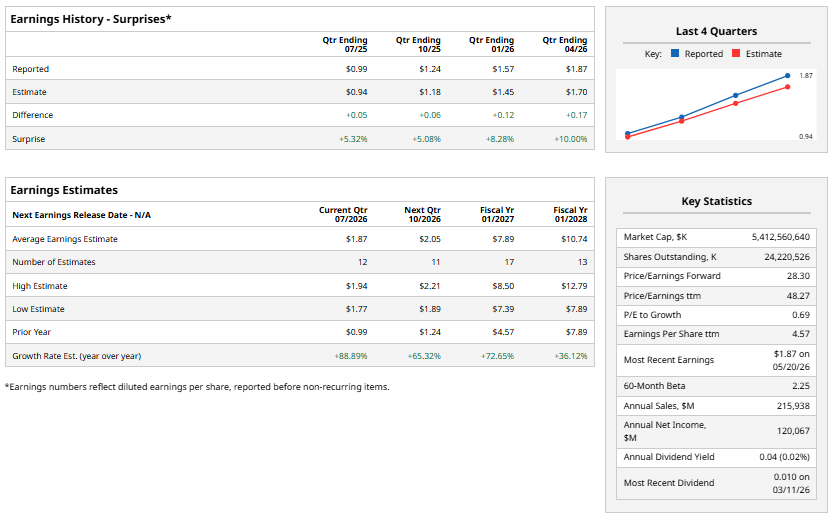

The company’s recent numbers show solid momentum in its business. Nvidia generated $82 billion in total revenue, up 85% year-over-year (YOY) and 20% sequentially. More importantly, Nvidia added $13.5 billion in revenue in just one quarter, a staggering increase for a company already operating at a massive scale.

The biggest catalyst remains its data-center business, which produced $75 billion in revenue, rising 92% YOY and 21% sequentially. Nvidia attributes the acceleration primarily to continued adoption of its Blackwell architecture, with GB300 and NVL72 systems seeing particularly strong uptake among hyperscalers and frontier AI model developers.

Within the business, data-center computing revenue climbed to $60 billion, while networking revenue nearly tripled YOY to $15 billion. That indicates Nvidia is increasingly capturing adjacent infrastructure layers required to scale AI workloads efficiently across massive clusters.

Moreover, Nvidia is now pushing even deeper into the stack with CPUs. As the AI industry transitions from model training toward inference and agentic AI workloads, the need for CPUs is rising significantly, creating a solid growth opportunity for the company.

Nvidia now estimates there is roughly $200 billion in CPU-related opportunity. Management expects CPU products alone to contribute approximately $20 billion in revenue this year.

Nvidia’s growing dominance in this space strengthens its growth outlook. First, it deepens Nvidia’s role inside AI data centers by enabling the company to sell integrated compute platforms. Second, it increases switching costs for hyperscalers and enterprise customers adopting Nvidia’s full-stack architecture. Finally, it expands Nvidia’s monetization potential across every phase of AI deployment, from training to inference to autonomous AI agents.

Overall, Nvidia has a solid growth opportunity ahead, which will support its share price. Nvidia projects Blackwell and Rubin-related revenue of $1 trillion from 2025 through calendar-year 2027. Moreover, if CPU adoption scales alongside that roadmap, Nvidia’s long-term revenue potential may extend well beyond current consensus expectations.

Nvidia Stock Appears Attractive on Valuation

Nvidia’s AI ecosystem is expanding rapidly. While Nvidia already dominates the GPU market, its fast-growing networking revenues, expansion into CPUs, and full-stack AI infrastructure are opening significantly larger long-term revenue opportunities. Strong demand for Blackwell systems, rising spending from hyperscalers, and increasing adoption of inference and agentic AI workloads are expected to drive significant future growth.

At the same time, NVDA stock still trades at a valuation that looks attractive relative to its exceptional growth outlook. NVDA trades at 28.3 times forward earnings, which appears low given its growth potential. Analysts expect earnings growth of 72% in fiscal 2027, followed by a solid 36% jump in fiscal 2028.

Strong ongoing spending on AI, Nvidia’s expanding revenue base, and its leadership in next-generation GPUs and CPUs indicate that Nvidia stock has significant upside potential and could hit the Street-high $380 price target.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Stock Price Predictions: How NVDA Could Rally to $380 Elon Musk Wants Small Investors to Buy the SpaceX IPO. Here’s Why You Shouldn’t. Why Wall Street Thinks This Dividend Stock Could Jump 30% Unusual Options Activity in CSX Stock Could Signal More Upside Ahead