Seagate Technology (STX) has been one of the best-performing stocks in the S&P 500 Index ($SPX) this year, with shares soaring 195.42% year-to-date (YTD). The stock’s stellar rally places it among the market’s top gainers, behind only Sandisk (SNDK) and Intel (INTC), whose shares have climbed roughly 529.26% and 224.15%, respectively, over the same period.

The surge in Seagate’s stock has been driven by growing demand for high-capacity data storage solutions as companies ramp up spending on artificial intelligence (AI) infrastructure. The rapid expansion of AI applications is creating an enormous need for data centers capable of storing and processing massive amounts of information, and Seagate is benefiting from this trend.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

At the same time, favorable industry dynamics are strengthening the company’s financial performance. Limited supply across the storage market has helped improve pricing conditions, allowing Seagate to generate stronger revenue and higher profitability. These improving fundamentals have played a major role in driving investor confidence and supporting the stock’s sharp rise.

Even after its impressive gains, here are three reasons why Seagate stock could still keep rallying.

www.barchart.com

www.barchart.com Reason #1: AI-Driven Storage Demand Appears Sustainable

The rally in STX appears sustainable, supported by strong demand for high-performance storage solutions and favorable pricing.

In its latest quarter, Seagate Technology reported $3.1 billion in revenue, driven primarily by its data center business, which accounted for nearly 80% of sales and grew 55% year-over-year (YOY). Growth reflects rising demand from hyperscale cloud and enterprise customers seeking scalable, cost-efficient storage infrastructure.

Profitability improved sharply as adjusted gross profit reached $1.5 billion, while gross margin expanded to 47% from 42.2% in the prior quarter. Better pricing and an improved mix of high-capacity products supported the margin gains.

Long-term, AI adoption is accelerating data creation and increasing the need for long-term storage and historical data analysis. Demand is expanding beyond traditional cloud environments into enterprise edge deployments, reflecting the growing need for high-capacity hard drives in modern data centers.

And, Seagate is strengthening its position through its Mozaic platform and Heat-Assisted Magnetic Recording (HAMR) technology, which aims to increase storage density and efficiency. These innovations could support future demand and margin expansion.

Additionally, the company’s build-to-order (BTO) manufacturing model improves visibility into customer demand while supporting pricing and supply balance.

Overall, rising storage demand, improving pricing trends, and Seagate’s operational discipline position the company for continued revenue and earnings growth, supporting further upside in its stock price.

Reason #2: Seagate’s Balance Sheet Is Improving Fast

Seagate Technology's disciplined capital allocation strategy is focused on lowering debt and strengthening its balance sheet, supporting long-term growth and shareholder returns. During the last reported quarter, the company repaid $641 million in debt, lowering gross debt to about $3.9 billion. Since the start of fiscal 2026, Seagate has reduced total debt by roughly $1.1 billion, reflecting consistent financial discipline and focus on lowering balance sheet risk.

The company’s leverage profile has improved significantly, with net leverage declining to 0.7 times in the March quarter, backed by adjusted EBITDA of $1.2 billion. Lower leverage enhances Seagate’s financial flexibility and ability to invest for future growth while managing obligations effectively.

With improving profitability and strong cash generation, Seagate appears well-positioned to continue reducing debt in the coming quarters, further strengthening its financial foundation and overall stability.

Reason #3: Seagate’s Valuation Indicates Further Upside

Despite Seagate’s strong stock performance, its valuation still looks appealing relative to its earnings growth potential.

The data storage giant continues to benefit from sustained demand for high-capacity storage solutions, driven by the rapid expansion of AI data centers, cloud computing, and enterprise data needs. At the same time, Seagate’s forward price-to-earnings ratio of 53.27 times appears reasonable given the company’s expected earnings growth trajectory. Analysts forecast Seagate’s earnings-per-share to surge by 81% to $25.52 in fiscal 2027, indicating the potential for continued momentum in the stock. With strong industry tailwinds and accelerating profitability, Seagate still offers meaningful upside for long-term investors.

Final Takeaway

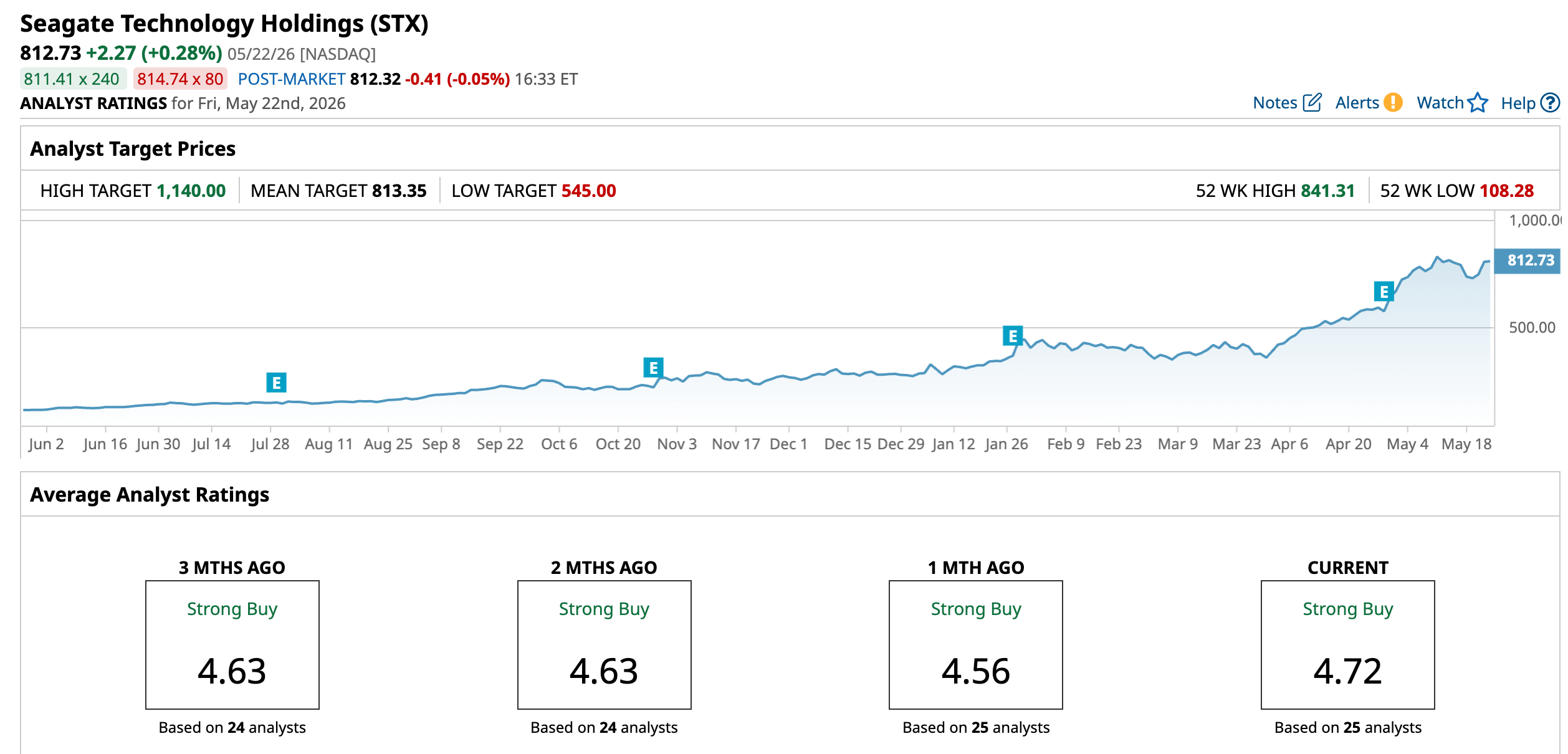

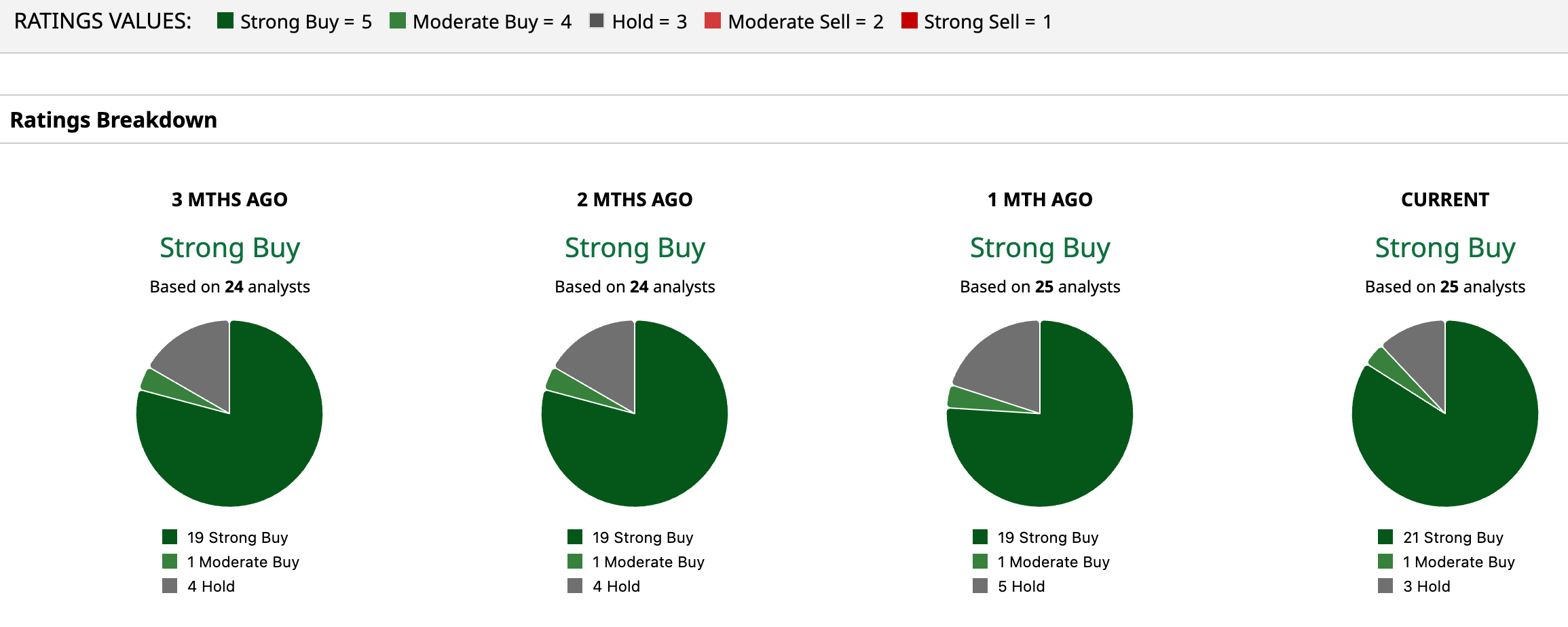

Seagate’s massive run in 2026 is supported by structural demand, improving pricing conditions, and rapidly expanding profitability. With storage demand continuing to surge and financial fundamentals strengthening, Seagate’s rally may still have further to go. Analysts are bullish and maintain a “Strong Buy” consensus rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Broadcom’s AI Packaging Bet Gets Bigger. Wall Street Is Betting on More Upside for AVGO Stock. Up 195% YTD: 3 Reasons Why Seagate Stock Could Keep Rallying Short Sellers Keep Placing Their Bets Against Micron Stock. Why They Think MU Will Stumble Soon. The Microsoft Disaster: Why Dropping the OpenAI Leash Flips the Entire Script for MSFT Stock