Unity Software U is rebuilding its business around higher-quality revenue streams, stronger profitability and broader monetization opportunities. The company’s transition away from nonstrategic operations is improving revenue quality, even as divestitures continue creating temporary volatility.

Strategic revenue grew 35% year over year in the first quarter of 2026 to $432 million, reflecting stronger execution across advertising and developer services.

Unity is also expanding its positioning against AppLovin APP, Roblox RBLX and Adobe ADBE as gaming, advertising and AI-powered creator tools converge. The question for investors is whether Unity’s transition can support sustainable growth and profitability improvements.

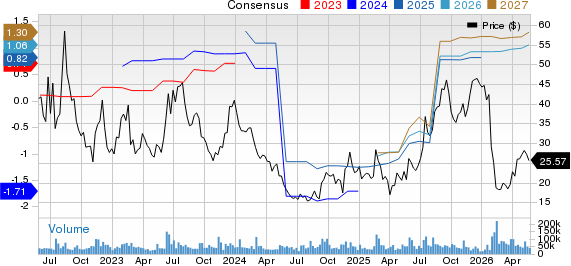

Unity Software Inc. Price and Consensus

Unity Software Inc. price-consensus-chart | Unity Software Inc. Quote

U Investment Case Hinges on Strategic Revenue Acceleration

Unity’s investment case depends heavily on accelerating strategic revenue while reducing exposure to lower-quality operations. In the first quarter of 2026, nonstrategic revenue declined 34% year over year due to the sunset of the ironSource Ad Network and the planned Supersonic divestiture.

The shift matters because it improves the long-term durability of Unity’s business model. Management is prioritizing scalable advertising tools, creator subscriptions and monetization services that can support recurring revenue growth.

Second-quarter guidance also reflects the transition. Unity expects Strategic Revenue between $455 million and $465 million, representing 29-32% year-over-year growth. While total revenue guidance remains relatively flat, the strategic business is expanding rapidly.

The transition places Unity in closer competition with AppLovin in mobile advertising and monetization software. However, Unity benefits from combining ad technology with a broader game-development ecosystem.

Unity’s Product Ecosystem Expands Monetization Paths

Unity’s product ecosystem continues creating new monetization channels for developers. The Create segment delivered 15% year-over-year strategic revenue growth during the first quarter, supported by subscription demand and consumption-based services.

A major catalyst is Unity AI, which entered public beta during May 2026. The platform integrates directly into development workflows and helps automate coding, asset creation and productivity tasks.

Unity is also expanding into web and commerce tools that help developers manage catalogs, pricing and payments across mobile, browser and PC experiences.

Roblox is similarly investing in creator monetization and immersive experiences, though Unity maintains stronger exposure to professional developers and enterprise applications. Meanwhile, Adobe continues integrating AI into creative workflows, increasing competitive pressure in digital production software.

U Earnings Growth Outlook Supports Forward Multiple Compression

Unity’s profitability trajectory has improved meaningfully. Zacks consensus estimates project earnings per share of $1.06 for 2026 and $1.30 for 2027, reflecting expanding operating leverage as strategic revenue grows.

Estimate revisions have strengthened sharply, with current-year EPS estimates rising roughly 174% over the past four weeks. Investors are increasingly optimistic about Unity’s margin expansion potential.

First-quarter adjusted EBITDA margin improved to 27%, supported by tighter spending across research and development, sales and marketing and administrative functions. Management also expects progress toward GAAP profitability by the fourth quarter of 2026.

Compared with Roblox, Unity appears further along in balancing growth and profitability. However, AppLovin continues demonstrating strong execution in mobile advertising, which keeps competitive pressure elevated.

Unity Software Balance Sheet Strength Reduces Downside Risk

Unity’s balance sheet provides stability. The company ended the first quarter with approximately $2.14 billion in cash and cash equivalents alongside improving operating cash flow.

Operating cash flow totaled $71 million during the quarter, while free cash flow reached $66 million. Management also indicated that available liquidity should comfortably address the company’s $558 million convertible debt maturity due in November 2026.

Strong liquidity gives Unity flexibility to continue investing in AI infrastructure, product development and monetization tools despite macroeconomic uncertainty. Adobe’s aggressive AI investments also highlight the importance of maintaining financial flexibility.

U Stock Risks Could Limit Near-Term Upside Potential

Risks remain despite the improving outlook. Unity’s second-quarter guidance still implies relatively flat total revenue growth as nonstrategic revenue exits offset strategic gains.

The company also remains exposed to ad-market cyclicality and mobile gaming demand trends. In addition, integrating AI models, runtime behavioral data and commerce capabilities introduces execution complexity that could temporarily affect performance.

Conclusion

Although Unity’s strategic momentum and profitability trends are encouraging, some investors may prefer waiting for clearer post-transition visibility before becoming more aggressive with the stock. Additional competition from Roblox and AppLovin should also keep innovation pressure elevated across the gaming ecosystem. Unity currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Adobe Inc. (ADBE): Free Stock Analysis Report

AppLovin Corporation (APP): Free Stock Analysis Report

Unity Software Inc. (U): Free Stock Analysis Report

Roblox Corporation (RBLX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).