Invitation Homes Inc. INVH sits in a practical corner of real estate — single-family rental homes. This makes the company tied to a simple trend. Many households still want the space and feel of a house, but buying one remains difficult because of high prices, mortgage costs and limited supply in attractive areas. INVH gives investors exposure to that demand through a large, professionally managed rental platform.

Last month, Invitation Homes reported first-quarter 2026 core funds from operations (FFO) per share of 48 cents, in line with the Zacks Consensus Estimate. The quarter reflected firm operating momentum, with higher blended rentals and leasing trends improving in April.

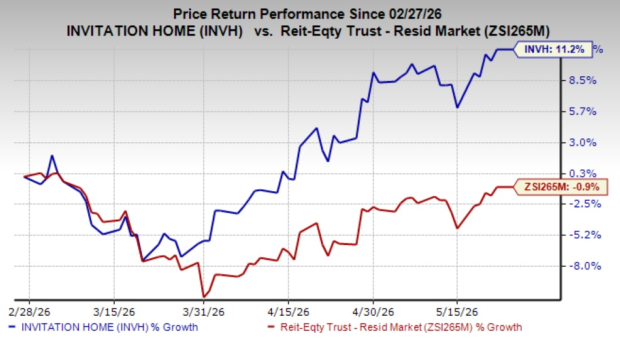

INVH shares have rallied 11.2% over the past three months against the industry’s decline of 0.9%. Analysts also seem bullish on this Zacks Rank #2 (Buy) company, with the Zacks Consensus Estimate for its 2026 and 2027 FFO per share both revised northward by a cent over the past month to $1.95 and $2.02, respectively. Despite the recent run, there seems additional room for further growth of INVH stock.

Image Source: Zacks Investment Research

Factors That Make Invitation Homes Stock a Solid Pick

Strong Position in High-Demand Housing Markets: Invitation Homes owns and manages a large single-family rental platform, with most of its portfolio located in the Western United States, the Sunbelt and Florida. These are markets where population growth, job opportunities and limited housing supply can support long-term rental demand. As of March 31, 2026, the company’s platform covered 109,745 homes across 16 core markets, giving it meaningful scale.

Builder Partnerships Add Growth Options: INVH is not relying only on buying existing homes. Its relationships with homebuilders, the ResiBuilt platform and the construction lending program give the company more ways to grow without taking on the full cost of traditional expansion. It had agreements to acquire about 556 newly built homes over the next few years, backed by roughly $370 million in remaining commitments.

Technology Is Helping Revenues: Invitation Homes continues to invest in technology and process enhancements to improve the resident experience and support margins. The ProCare application and value-added services such as Smart Home, internet bundle and the HVAC filter program are helping lift other property income. In the first quarter of 2026, other property income rose 10.3% year over year, supporting same-store revenue growth.

Balance Sheet Remains Strong: Management remains focused on an investment-grade balance sheet. As of March 31, 2026, Invitation Homes had $1.304 billion of available liquidity and net debt/TTM adjusted EBITDAre of 5.6X, within its targeted 5.5X-6.0X range. About 90% of its wholly owned homes were unencumbered, supporting refinancing flexibility.

Dividend Support and Buybacks Remain Appealing: Solid dividend payouts are arguably the biggest enticement for REIT investors, and the company remains committed to that. The company has increased its dividend five times in the last five years, and its five-year annualized dividend growth rate was 12.76%, which is encouraging. With full-year 2026 core FFO guidance maintained at $1.90-$1.98 per share, the payout looks supported by the company’s cash flow outlook. Invitation Homes has also been active with buybacks. In the first quarter, it repurchased 17.1 million shares for about $439 million, and it later received a new $500 million authorization. Fewer shares can improve per-share results over time, especially when buybacks are done at attractive prices.

Other Stocks to Consider

Some other top-ranked stocks from the broader REIT sector are American Homes 4 Rent AMH and Prologis, Inc. PLD, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus mark for American Homes 4 Rent’s 2026 FFO per share has been revised a cent upward to $1.93 over the past month.

The Zacks Consensus Estimate for Prologis’ 2026 FFO per share suggests a 6.20% increase year over year.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Prologis, Inc. (PLD): Free Stock Analysis Report

American Homes 4 Rent (AMH): Free Stock Analysis Report

Invitation Home (INVH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).