Carter's, Inc. CRI appears to be regaining momentum in the U.S. Retail business, with first-quarter fiscal 2026 results signaling improving consumer engagement and stronger brand traction. The company delivered its fourth consecutive quarter of comparable sales (comps) growth, benefiting from higher traffic across stores and digital channels. Management attributed the gains to stronger demand creation initiatives, better product assortments and increased engagement from younger consumers, particularly Gen-Z shoppers. While macroeconomic uncertainty and tariff pressures remain concerns, CRI’s retail performance suggests that its turnaround initiatives are beginning to resonate with customers.

The numbers from the quarter highlight the strength of the retail segment. U.S. Retail net sales increased nearly 13% year over year, while comparable retail sales rose more than 10%. On a two-year basis, comps advanced close to 5%, reflecting sustained improvement beyond easy comparisons. Traffic and average transaction values both improved in the quarter, supported by low-single-digit gains in average unit retail (AUR). At the same time, unit sales climbed in the double digits, indicating that demand remained healthy despite consumers becoming increasingly value-focused. The baby category remained the strongest performer, while toddler and kid assortments also posted growth.

Management emphasized that investments in marketing and demand creation are playing a central role in driving momentum. CRI has expanded its use of social media, influencers and connected TV advertising to reach younger parents, where they increasingly discover brands. Collaborations such as the Disney-OshKosh Winnie the Pooh collection also helped attract new consumers and generated higher-than-average AURs. Importantly, the company noted that its active consumer file continued to grow in the quarter, suggesting that recent marketing initiatives are not only boosting short-term traffic but also strengthening long-term customer acquisition trends.

Still, questions remain about whether this momentum can be sustained through the rest of 2026. Management acknowledged softer demand trends in April following the Easter-driven March surge, while inflationary pressures and evolving tariff conditions could weigh on consumer spending patterns. CRI also expects pricing to play a larger role in the second half, which could moderate unit growth. Nevertheless, easier comparisons ahead, improved wholesale bookings and continued traction from marketing investments provide reasons for optimism. If Carter’s can maintain traffic growth while balancing pricing and value perception, its U.S. Retail momentum may prove more durable than previously expected.

CRI’s Price Performance, Valuation & Estimates

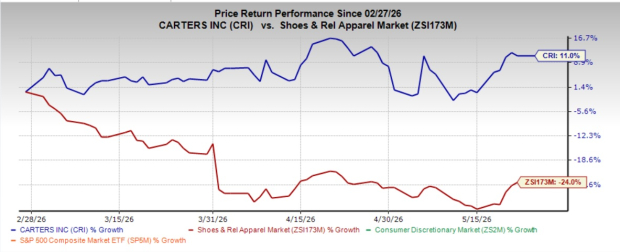

Carter’s shares have gained 11% in the past three months against the industry’s 24% decline.

CRI Stock's Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, CRI trades at a forward price-to-earnings ratio of 11.90X compared with the industry’s average of 20.87X.

CRI Stock's Valuation

Image Source: Zacks Investment Research

Carter’s currently carries a Zacks Rank #3 (Hold).

Key Picks in the Consumer Discretionary Space

Vince Holding Corp. VNCE provides luxury apparel and accessories in the United States and internationally. It operates through Vince Wholesale and Vince Direct-to-Consumer segments. At present, the company flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for VNCE’s current fiscal-year sales implies growth of 4.5%, and the same for earnings implies a decline of 15.9% from the year-ago figures. VNCE has delivered a trailing four-quarter earnings surprise of 647.2%, on average.

Columbia Sportswear Company COLM engages in the design, development, marketing and distribution of outdoor, active and lifestyle products in the United States, Latin America, the Asia Pacific, Europe, the Middle East, Africa and Canada. At present, COLM flaunts a Zacks Rank of 1.

The Zacks Consensus Estimate for COLM’s current fiscal-year sales implies growth of 2.6%, and the same for earnings indicates a decline of 0.8% from the year-ago figures. COLM delivered a trailing four-quarter earnings surprise of 44.1%, on average.

Superior Group of Companies, Inc. SGC produces, manufactures and sells promotional products and branded uniforms, and healthcare apparel and accessories in the United States and internationally. At present, SGC carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for SGC’s current fiscal-year sales and earnings implies a growth of 2% and 28.3%, respectively, from the year-ago figures. SGC delivered a trailing four-quarter negative earnings surprise of 81.9%, on average.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Columbia Sportswear Company (COLM): Free Stock Analysis Report

Carter's, Inc. (CRI): Free Stock Analysis Report

Vince Holding Corp. (VNCE): Free Stock Analysis Report

Superior Group of Companies, Inc. (SGC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).