Billionaire Daniel Loeb just wrote a sizable check to Hut 8 (HUT), and he did it after the stock had already taken off. In Q1 2026, his hedge fund, Third Point LLC, opened a new position in Hut 8, buying about 869,563 shares worth roughly $40.8 million.

This move comes as Hut 8 has been changing from a traditional Bitcoin miner into a fast‑growing energy and computing business. Its shares have climbed 102.57% over the past three months, and that rise is tied to specific decisions rather than buzz or headlines.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Within five months, the company says it has more than doubled its contracted capacity. It also secured $9.8 billion in incremental base‑term contract value through long‑term agreements, giving it a much clearer line of sight on future revenue.

That progress sets up a simple but important question. What does this high‑conviction bet really signal for the next phase of HUT stock?

HUT’s Financial Check

Hut 8 develops digital infrastructure that links Bitcoin mining with high‑performance computing and data centers, using long‑term power and hosting contracts to build steady, recurring revenue.

This Miami‑based company's stock has a year‑to‑date (YTD) gain of 131.73% and a 52‑week return of almost 567%.

www.barchart.com

www.barchart.com HUT has a market capitalization of $11.9 billion, a trailing price‑to‑earnings multiple of 3,508.66 times, far above its sector median of 26.18 times, and a price‑to‑cash‑flow ratio of 235.15 times, also elevated against its sector median of 18.71 times.

Their recent earnings history shows the quarter ending March 26 delivered a reported loss per share of $0.12 against a consensus estimate for a $0.28 loss, a 57.14% positive surprise. Their revenue for the three months ended March 31, was $71.0 million, up from $21.8 million in the prior‑year period, pointing to a strong jump in sales.

This breakdown shows $3.7 million from Power, $1.3 million from Digital Infrastructure, and $66.0 million from Compute, so most of the growth is coming from compute‑related activity. Their bottom line reflects the digital‑asset exposure, with a net loss of $253.1 million versus $134.3 million a year earlier.

This loss includes $295.7 million of primarily unrealized losses on digital assets, compared with $112.4 million in the prior‑year period, which explains net income looking so weak despite the revenue improvement.

HUT’s Infrastructure Build‑Out

Hut 8 has moved quickly to lock in its AI ambitions with firm, long‑dated contracts. The company has brought the first phase of its 1 GW Beacon Point data center campus in Texas online with a 15‑year, 352 MW IT lease that carries a base‑term contract value of $9.8 billion. This single agreement gives the business clear visibility on a large block of demand and lays down a solid base of contracted revenue to support its buildout.

The expansion plans do not stop in Texas. The company has put $16 million toward expanding water infrastructure in West Feliciana Parish in Louisiana, a move tied directly to future data center development in that region.

The funding playbook is evolving in step with these projects. The company has closed $3.25 billion of investment‑grade senior secured notes in a major financing for its River Bend data center project. This structure locks in long‑term capital for the build and reduces the need to lean on new equity for each large development.

Put together, these milestones show a company that is methodically lining up big‑ticket AI leases, critical infrastructure investments, and large, investment‑grade financing.

How the Street Is Framing HUT

Hut’s next earnings release is scheduled for August 6, and the current consensus for the June 2026 quarter calls for earnings per share of -$0.29. That compares with -$0.14 in the same quarter a year earlier, implying a year‑over‑year (YOY)growth rate of -107.14%.

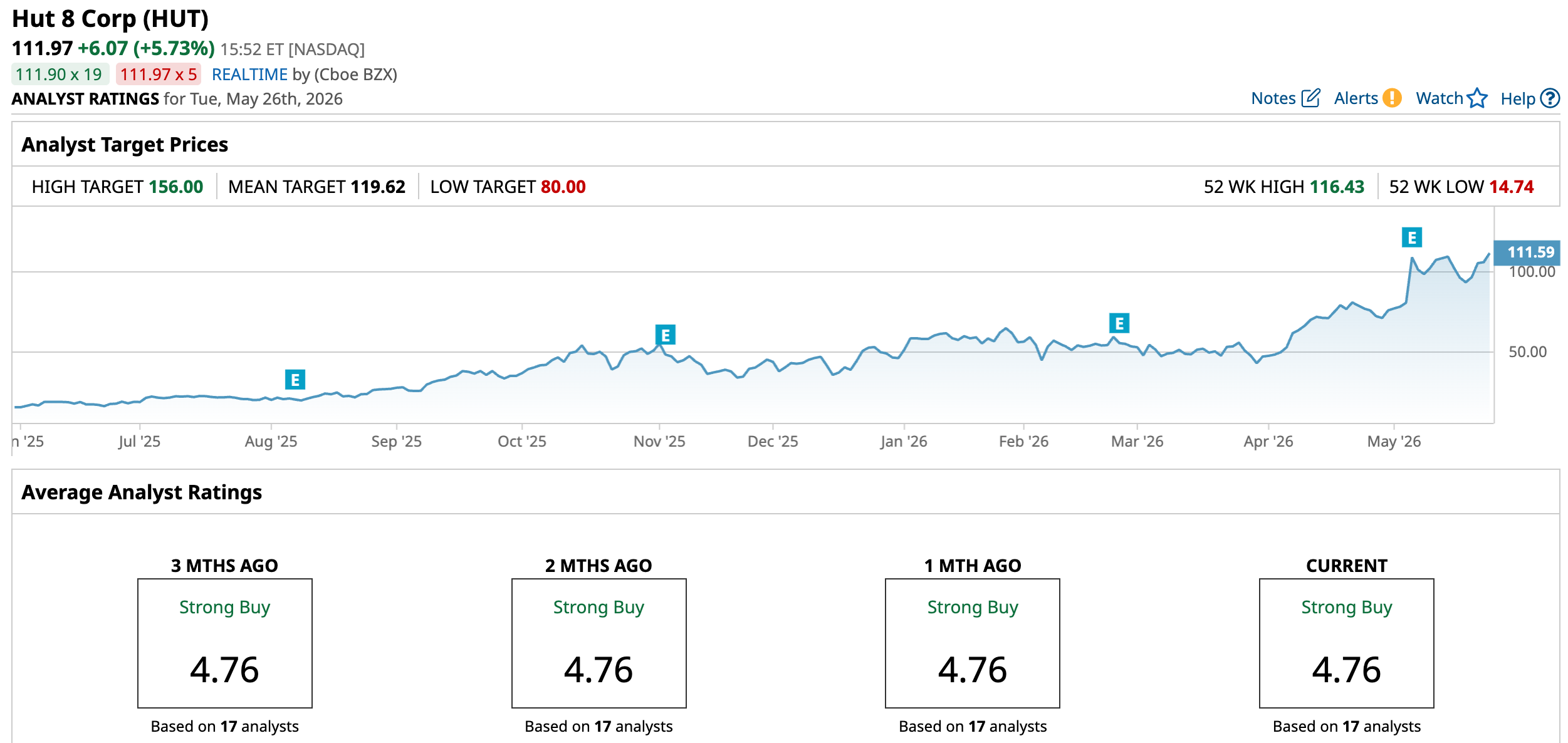

Nevertheless, the story around HUT is not about the next quarter alone. Jefferies Financial Group recently initiated coverage of Hut 8 with a “Buy” rating and a price target of $156, implying about 47.3% upside from current levels.

They tied that view mainly to the company’s two AI data center leases, which they see as key to the long‑term case. Those contracts give Hut 8 multi‑year visibility on demand and support the idea that earnings can improve over time, even though EPS is still negative today.

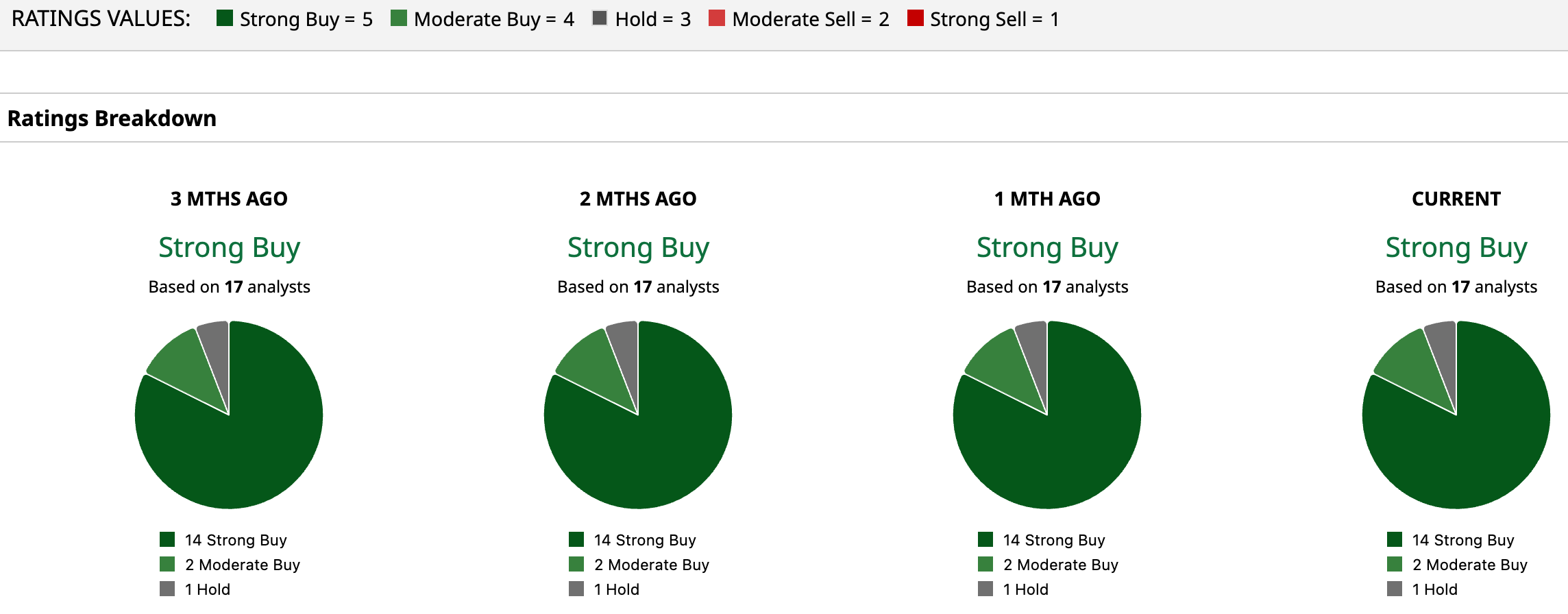

This optimism lines up with the broader Street view. Hut carries a consensus “Strong Buy” rating from 17 analysts, with an average price target of $119.62 that works out to roughly 6.8% upside from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Dan Loeb’s new stake shows HUT is now being treated as a serious bet on future infrastructure, not just a side play on crypto. With multi‑billion‑dollar leases already in place and analysts leaning “Strong Buy,” the odds still favor higher prices over the next few years, even if the moves remain big in both directions. Anyone buying at this stage is really betting that the company's delivery on those contracts will matter more than the next big move in bitcoin.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Jefferies Just Upgraded Generac Stock. Here’s Why. Billionaire Dan Loeb’s Third Point Just Took a New Position in Hut 8. What This Means for HUT Stock. Wall Street Is Only Just Beginning to Recognize Advanced Micro Devices’ Agentic AI Upside Potential Why You Should Buy Marvell Technology Stock Before May 27