STMicroelectronics (STM) is a Geneva-headquartered global semiconductor leader serving customers across automotive, industrial, personal electronics, and cloud computing markets. Born from the merger of Italian and French semiconductor firms, STM designs and manufactures a broad portfolio spanning analog ICs, MEMS sensors, microcontrollers, power discretes, and advanced connectivity solutions.

What makes STM an increasingly compelling AI candidate is its expanded multi-year, multi-billion-dollar strategic collaboration with Amazon (AMZN) Web Services (AWS), positioning STM as a key supplier of high-bandwidth connectivity, mixed-signal processing, and energy-efficient power ICs that directly power next-generation hyperscale AI and cloud computing infrastructure. For investors seeking a differentiated, less-crowded entry into the AI semiconductor supply chain, STM presents a unique value proposition.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

STMicroelectronics Stock Surges

STM's 52-week return is approximately 165%, while its YTD return is around 159%, reflecting a recovery in auto chip demand, normalizing distributor inventories, and an expansion into the AI infrastructure market that boosted the stock's price. STM surged over 33% in just 30 days following its Q1 2026 earnings beat, driven by AI data center momentum and improving bookings.

Against the S&P 500 Information Technology Index ($SRIT), which has returned about 29%, STM has significantly over performed over the past year. Its accelerating revenue recovery, AWS partnership, and growing AI infrastructure exposure position it as a high-conviction stock within the broader semiconductor sector.

www.barchart.com

www.barchart.com STMicroelectronics Shines on Results

STMicroelectronics reported Q1 2026 net revenues of $3.10 billion, up 23% year-over-year and beating consensus estimates of approximately $3.05 billion. The revenue beat was fueled by strong momentum in personal electronics and cloud-edge computing products. Non-GAAP diluted EPS came in at $0.13, up 85.7% year-over-year but slightly below analyst expectations of around $0.18, as unused manufacturing capacity charges weighed on near-term profitability.

GAAP gross margin for Q1 came in at 33.8%, while non-GAAP gross margin reached 34.1%, both above the midpoint of the company's guidance range, driven by a favorable product mix. Net cash from operating activities was $534 million, down slightly from $574 million a year ago, primarily due to approximately $45 million in restructuring costs tied to the company's ongoing manufacturing footprint optimization program. Operating income on a non-GAAP basis stood at $171 million, with operating margins recovering meaningfully year-over-year.

Management guided Q2 2026 revenues to $3.45 billion at the midpoint, implying 11.6% sequential growth and 24.9% year-over-year growth, with non-GAAP gross margins expected at approximately 35.2%. Most notably, CEO Jean-Marc Chery confirmed that ST is now positioned to capture upside from new AI-driven programs, with data center revenues expected to exceed $500 million for 2026 and surpass $1 billion for 2027, a clear signal that this oft-overlooked chipmaker is becoming a meaningful player in the global AI infrastructure buildout.

Mizuho Bullish on STM

Mizuho analyst Vijay Rakesh has raised his price target on STMicroelectronics to $68 from $56, maintaining an “Outperform” rating, citing accelerating artificial intelligence tailwinds benefiting the analog semiconductor market. In a note to clients, Rakesh highlighted that analog chipmakers, including STM, are seeing growing content wins within high-power AI server architectures, with improving lead times and pricing dynamics, particularly within data center products. While near-term headwinds persist in the automotive segment, with light vehicle production now estimated down 2.3% year-over-year, the analyst views AI data center demand as a meaningful and durable offset.

The price target hike reflects growing conviction that STM's specialized analog and power semiconductor portfolio is increasingly mission-critical to the AI infrastructure buildout, reinforcing the bull case for this under-the-radar semiconductor name.

How to Play STM?

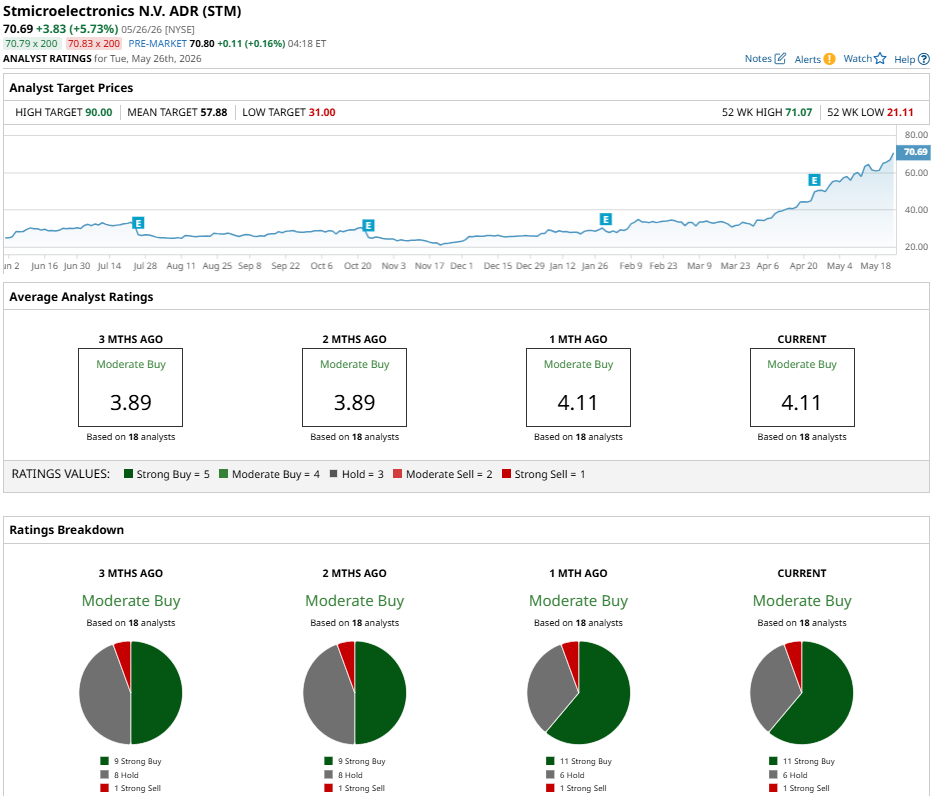

With Mizuho's upgraded price target of $68 reinforcing the AI data center tailwind narrative, STMicroelectronics is gaining institutional attention as a differentiated analog semiconductor play. However, broader Wall Street consensus remains cautious, with STM carrying a "Moderate Buy" rating across 18 analyst ratings, comprising 11 "Strong Buy," six "Hold," and one "Strong Sell," with a mean price target of $57.88, implying approximately 15% downside from current levels.

For investors, STM represents a higher-risk, higher-reward opportunity, best suited for those with conviction in its AI infrastructure pivot and willingness to look past near-term margin pressures.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SoFi Stock Is Down 51% from Its Highs. Don’t Miss this Chance to Buy the Dip. This One Decision Could Make or Break Apple Stock The Under-the-Radar AI Semiconductor Play You Shouldn’t Ignore Bank of America Says Nvidia Is Still the Top AI Compute Stock to Buy Despite YTD Underperformance. Here’s Why.