Costco Wholesale Corporation COST used its fiscal third-quarter call to stress a familiar point with sharper urgency: in a volatile consumer and cost environment, management wants to protect member value first. That stance shaped the company’s pricing, fuel, digital and capital allocation commentary.

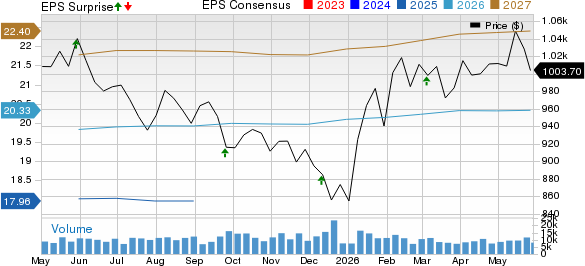

The setup around that message was solid. Costco reported earnings per share of $4.93, ahead of the Zacks Consensus Estimate of $4.91 by 0.41%. Revenues of $70.53 billion exceeded the consensus estimate of $69.5 billion by 1.47%. On the call, executives spent more time explaining how they are defending traffic, loyalty and share than recapping the quarter’s beat.

Costco Wholesale Corporation Price, Consensus and EPS Surprise

Costco Wholesale Corporation price-consensus-eps-surprise-chart | Costco Wholesale Corporation Quote

COST Doubles Down on Member Value

Chief executive officer Ron Vachris said Costco’s operating focus remains delivering quality goods and services at the lowest possible price, and he tied that directly to unusually strong gasoline volumes during the quarter. Management said each of the three four-week periods set company fuel-volume records as members responded to higher market prices.

Chief financial officer Gary Millerchip reinforced that the company used pricing as a strategic lever. He said Costco widened its value gap in gas and cut prices on everyday items such as eggs and beef, while also lowering select Kirkland Signature prices across categories.

That framing mattered because management was not describing a reactive promotion cycle. In Q&A, Vachris said the price moves were strategic and consistent with Costco’s long-standing approach of moving down first when costs fall and holding off on increases as long as possible.

Costco’s Growth Engine Stays Broad

The operating backdrop remained strong. Net sales rose 11.6% to $69.15 billion, comparable sales increased 9.8%, or 6.6% adjusted for gasoline and foreign exchange, and digitally enabled comparable sales rose 21.5%. Traffic increased 2.4% worldwide, while average ticket grew 7.3%.

Millerchip highlighted balanced category strength, with fresh and nonfoods each up in the high single digits and ancillary businesses up in the mid-20% range. Pharmacy was a standout, helped by GLP-1 demand, expanded offerings, and market share gains.

Membership trends also stayed favorable. Membership fee income rose 10.7% to $1.37 billion, paid executive memberships increased 9.6% to 41.2 million, and renewal rates reached 92.2% in the United States and Canada, and 89.7% worldwide. Management also said the executive tier rollout in China is running ahead of expectations.

COST Faces Margin and Cost Pressure

Costco’s call also made clear that growth is being managed alongside a more complicated cost picture. Reported gross margin fell 21 basis points to 11.04%, though it was up 1 basis point excluding gas inflation. Core-on-core margin declined 9 basis points as the company invested in lower prices and absorbed higher transportation costs.

Millerchip said fresh, and food and sundries were pressured by lower everyday pricing, while mix also shifted toward gas, e-commerce and pharmacy. Those businesses helped sales but changed the margin profile of the quarter.

On expenses, SG&A improved to 8.96% from 9.16%, but management said healthcare costs and a few one-time items limited underlying leverage. The company also flagged potential nonfood inflation from higher resin costs and said it is monitoring the longer-term effects of elevated oil prices and tariffs.

Costco Uses Q&A to Frame the Outlook

A UBS analyst pressed management on whether paid member growth of 4.1% points to a more modest same-store sales outlook. Millerchip pushed back on that reading, calling the current pace more normal absent major new-market entries and emphasizing executive membership growth and stable renewal trends.

He also said Costco continues to see comparable sales excluding gas in the 6% to 7% range, despite lapping tougher comparisons in categories such as gold and gift cards. That was one of the clearest signals from the Q&A that management sees current demand trends as steady rather than deteriorating.

Questions from Morgan Stanley and JPMorgan on margins and pricing produced a similar message. Management acknowledged tactical price investments but described the competitive environment as rational and urged investors to look at margin performance on a more holistic, ex-gas basis.

COST Sticks With Expansion and Digital Spend

Management kept its growth priorities intact. Costco opened four net new warehouses in the quarter and now expects 26 net new openings for fiscal 2026, down two from its prior view because of project timing. Vachris said the longer-term target remains more than 30 net new openings a year.

Digital also remained a major emphasis. Site and app traffic rose 37%, personalized recommendation tools drove nearly $5 billion in e-commerce sales, and AI-sourced traffic grew at a triple-digit rate from a small base while showing the highest conversion rate of any source.

Capital spending reflects that agenda. CapEx was $1.41 billion in the quarter, and management expects about $6.5 billion for the year to support warehouse growth, remodels, logistics capacity, and member-facing technology.

Costco Leaves a Controlled, Confident Tone

The clearest takeaway from the call was management’s discipline around member economics. Costco is accepting selective pressure in margin components where it believes lower prices, better fuel value, and faster digital execution can reinforce loyalty and share gains.

That tone carried into capital allocation as well. Millerchip said growth investment remains the priority, with special dividends considered only when excess cash builds beyond those needs. The company ended the period with $18.95 billion in cash and cash equivalents.

What COST’s Zacks Signals Show

COST carries a Zacks Rank #3 (Hold), with a Value Score of D, Growth Score of A, Momentum Score of A, and VGM Score of B. In Zacks’ framework, a #3 rank supports a more neutral stance, while the stronger Growth, Momentum and VGM grades point to better characteristics than the weaker Value grade. Stocks with stronger Style Scores generally compare more favorably within the Zacks system, especially when paired with higher ranks.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That said, the Zacks Rank is driven by earnings estimate revisions and can change after a company reports results. For COST, the current mix of a Zacks Rank #3 and a VGM Score of B indicates balanced near-term characteristics rather than a decisive signal on its own.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).