Snowflake SNOW used its first-quarter fiscal 2027 call to make a broader point than a simple earnings beat. Management argued that the company is moving beyond data storage and analytics into a platform meant to power what CEO Sridhar Ramaswamy called an “agent enterprise.”

That message stood out because it was accompanied by stronger guidance, improving AI adoption metrics, and a Q&A centered less on demand concerns and more on the durability of AI-driven revenue contributions.

Snowflake Pitches a Broader AI Role

Ramaswamy framed the quarter around Snowflake’s attempt to become the governed layer where enterprise data, AI models, applications and workflows come together. He said that vision is now taking shape through Snowflake Intelligence for business users and Cortex Code, or CoCo, for developers.

The company’s pitch was that these products do more than add new features. Management said they pull more workloads onto the platform by helping customers move from prompts and queries into production workflows.

That theme gave the call a more forward-looking tone than a standard software earnings update. Snowflake positioned AI less as an adjacent opportunity and more as a force that can deepen use of its core data platform.

SNOW Says AI Is Feeding Core Consumption

Ramaswamy said adoption of Snowflake Intelligence more than doubled from the prior quarter, while CoCo was active in more than 7,100 accounts. He described that uptake as evidence that customers are beginning to use the products in real production settings.

Management also tied that adoption to heavier platform use. Executives said customers using CoCo are growing faster, supporting the view that AI tools are expanding consumption rather than merely shifting existing spend.

The quarter’s customer metrics supported that argument. Snowflake ended the period with 13,912 customers after adding 616 net new accounts, and management said the pace of new additions accelerated from a year earlier.

Snowflake Highlights Bigger, Faster Use Cases

Ramaswamy used customer examples to show where the company thinks the story is heading. He pointed to a large U.S. bank that completed a Teradata migration and is now building AI-powered regulatory intelligence and natural-language analytics on Snowflake.

He also pointed to Nestle’s broader data and AI transformation initiatives, arguing that customers increasingly want a single platform where they can ask questions, interpret insights and initiate actions. Snowflake says its agentic control plane is designed to enable exactly that kind of workflow.

Christian Kleinerman, senior vice president of product, reinforced that point in the Q&A. He said Snowflake’s metadata, activity signals and governance tools give the company an advantage in producing better AI outcomes inside customer environments.

SNOW Reworks Execution Around the AI Buildout

Management also used the call to show that the internal organization is being reshaped around this opportunity. Ramaswamy said Snowflake delivered more product capabilities in the quarter than a year earlier and is using AI internally to move faster across functions.

He paired that message with leadership changes. The company highlighted Jonathan Ballon’s transition into the chief revenue officer role while noting that co-founder Benoit Dageville will step back from day-to-day work and remain on the board.

The message was that execution is being tightened rather than reset. Snowflake said it is investing where demand is strongest, but AI-driven productivity is also allowing it to avoid simply scaling headcount in parallel with growth.

Snowflake Raises Outlook as CoCo Builds Momentum

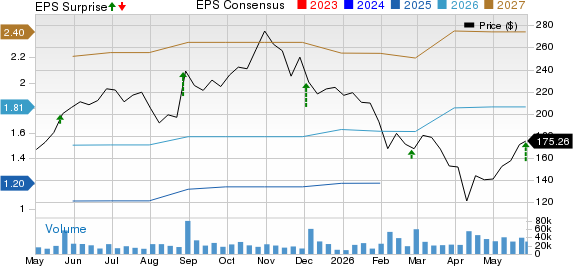

The financial context supported the stronger tone. Snowflake reported adjusted earnings of $0.39 per share, above the Zacks Consensus Estimate of $0.32, a 21.88% surprise, while revenues of $1.39 billion topped the $1.32 billion consensus by 5.23%.

Snowflake Inc. Price, Consensus and EPS Surprise

Snowflake Inc. price-consensus-eps-surprise-chart | Snowflake Inc. Quote

Chief financial officer Brian Robins said the company is now raising full-year product revenue guidance to $5.84 billion and expects second-quarter product revenues of around $1.42 billion.. He said there was no change in guidance philosophy, but CoCo had enough observed usage in the quarter to be incorporated into the model.

Robins also said Snowflake still expects a 75% non-GAAP product gross margin for the year. He linked that stability in part to lower bandwidth costs under a new five-year, $6 billion AWS agreement, even as AI products carry lower gross margins than the core platform.

SNOW Q&A Focuses on Costs, Speed and Moat

The analyst Q&A centered on whether CoCo is creating a temporary spike or a durable new layer of growth. A Morgan Stanley analyst asked what changed in the quarter to produce unusually strong sequential growth and higher guidance, and management pointed to both CoCo adoption and acceleration in the core business.

Questions from Evercore ISI, UBS and Barclays pressed Snowflake on use cases, economics and sales capacity. Ramaswamy said CoCo is shortening migration timelines, helping internal teams and customers move faster, and making the go-to-market organization more fluent in demonstrating AI value.

When asked about margin pressure and customer cost discipline, Robins acknowledged that AI products run below core gross margins, while Ramaswamy stressed governance controls, account-level limits and model efficiency. The tone was confident, but management also showed it knows cost control will be central to enterprise-scale AI adoption.

Snowflake Leaves the Call With a Sharper Agenda

Coming out of the call, Snowflake’s message was that AI is no longer just a tailwind to the core warehouse business. Management described it as a meaningful revenue engine that also drives more activity across the broader platform.

Just as important, executives framed the company’s next phase around governed action, not just governed data. That left investors with a clearer sense that Snowflake intends to compete on workflow, automation and enterprise trust as much as on analytics.

Zacks Signals Remain Mixed

SNOW currently carries a Zacks Rank #3 (Hold), with a Value Score of F, Growth Score of A, Momentum Score of C and VGM Score of C. That mix points to strong growth characteristics, but a less compelling value profile and a more balanced overall style setup. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In Zacks terms, the strongest near-term setups usually combine a Zacks Rank #1 or #2 (Buy) with A or B Style Scores. A Zacks Rank #3 and middling composite score suggest a more neutral signal for the next one to three months, and that rank can still change as earnings estimate revisions adjust after the quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Snowflake Inc. (SNOW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).