The price-action in CrowdStrike (CRWD) stock has been characterized by significant volatility in 2026. From $469 at the end of 2025, CRWD stock plunged to 52-week lows of $342.77 in February 2026. The correction was triggered by Anthropic confirming Claude Code Security, a next-gen AI model with advanced cybersecurity capabilities.

However, it didn’t take long for the markets to realize that the fears were exaggerated. What followed was a stellar comeback by CRWD stock to recent highs of $677.50. This rally has been backed by strong financial performance.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Further, growth in AI has translated into a big opportunity for CrowdStrike. According to Wedbush, Palo Alto Networks (PANW) and CrowdStrike are in “prime position to benefit from the most significant catalyst to hit the cybersecurity industry in decades.” As a result, Wedbush has increased the price target for CRWD stock to $700.

The optimism seems realistic with CrowdStrike guiding for annual recurring revenue in the range of $6.47 billion to $6.52 billion for FY27. This would imply a year-on-year growth of 23% to 24%. Healthy growth is likely to be backed by the rapid adoption of Falcon Flex subscription.

About CrowdStrike Stock

Founded in 2011 and headquartered in Austin, CrowdStrike is a provider of cybersecurity solutions. With global presence, CrowdStrike offers a software subscription-based model for its cloud-delivered protection of endpoints, cloud workloads, identity, and data.

With evolving customer needs, the company’s AI-native CrowdStrike Falcon platform is an AI-build unified platform to fight AI-enabled adversaries. The company ended FY26 with a record annual recurring revenue of $5.25 billion, which was higher by 24% on a year-on-year basis. For the same period, the company reported healthy free cash flows of $1.24 billion.

With AI as the key growth driver, CrowdStrike believes that the company’s addressable market for 2026 is $149 billion. Further, the addressable market is expected to swell to $325 billion by the end of the decade. This provides ample headroom for growth in the coming years.

With strong results, an optimistic growth outlook, and industry tailwinds, CRWD stock has rallied by 32% in the last six months.

www.barchart.com

www.barchart.com Business Is a Cash Flow Machine

Ultimately, businesses are valued on their potential to generate and increase cash flows. From that perspective, CrowdStrike is attractive as subscription-based revenue swells.

For FY26, CrowdStrike reported 22% non-GAAP operating margin and 26% free cash flow margin. With the Falcon gaining growth traction, it’s likely that FCF will continue to swell in the next few years. This positions the company to pursue aggressive share repurchase.

At the same time, CrowdStrike has been pursing inorganic growth. In January 2026, the company acquired SGNL, a player in continuous identity. This will enable CrowdStrike to make inroads in the next-generation identity security market that’s expected to be worth $56 billion by 2029.

CrowdStrike also acquired Seraphic Security, which is in the business of browser runtime security. High financial flexibility provides visibility for potential acquisitions to gain market share and drive the ARR higher.

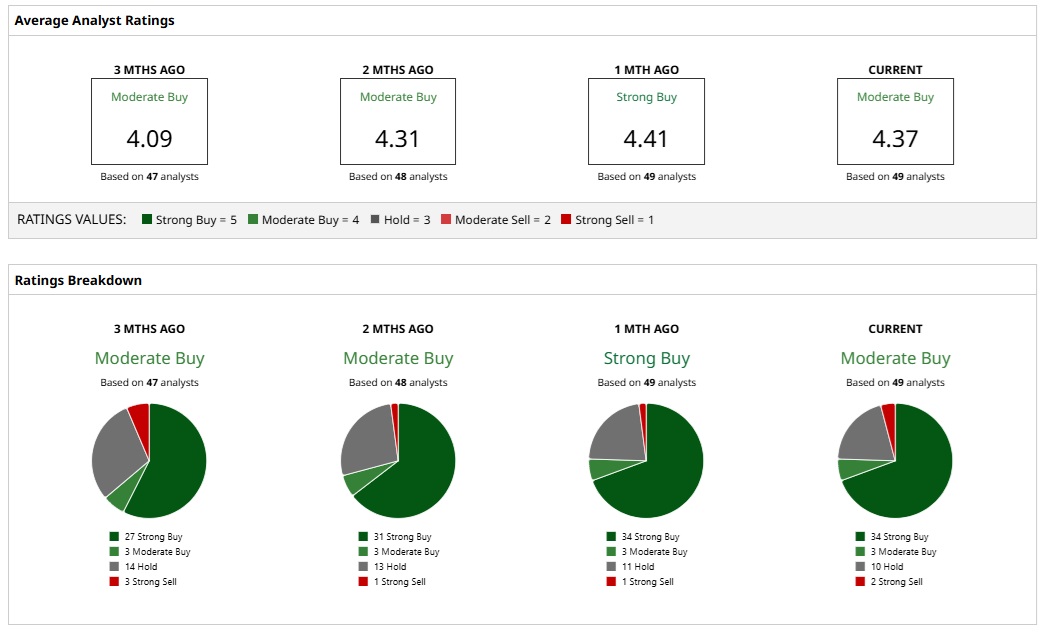

What Do Analysts Say About CRWD Stock?

Based on 49 analysts with coverage, CRWD stock has a consensus “Moderate Buy” rating. While 34 analysts have a “Strong Buy” rating for CRWD stock, three have a “Moderate Buy,” and 10 have a “Hold” rating. Among the bears, two analysts have a “Strong Sell” rating.

The mean price target of $547.30 represents potential downside of 18% from current levels. However, the most bullish price target of $706 suggests that CRWD could climb 5% from here.

www.barchart.com

www.barchart.com Concluding Views

CrowdStrike has made a strong comeback from over bearish sentiments related to SaaS earlier this year. It’s worth noting that the company continues to target research and development expense at 15% to 20% of revenue. These investments are likely to ensure that CrowdStrike maintains a strong position in the cybersecurity solutions industry.

Further, the AI-driven structural industry tailwinds coupled with high gross retention rates will ensure stability in cash flows. The business model therefore looks attractive from the perspective of continued shareholder value creation.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lululemon Stock Has Crashed 60% Over the Past Year, But 1 Ugly Distraction Is Finally Gone Micron Stock Just Joined the Trillion-Dollar Club. Wall Street Says MU Still Has Room to Run. As ARR Swells on AI Tailwinds, CrowdStrike Stock Is a Cash Flow Machine Marvell’s Q1 Earnings Strengthen Its Bull Case — But MRVL Stock Isn’t a Screaming Buy Yet