The Zacks Property and Casualty (P&C) Insurance industry has been benefiting from Solid retention, exposure growth across business lines and improved pricing, driving higher premiums and helping insurers maintain profitability. The industry remains focused on personalized offerings to enhance customer experience, leveraging digitalization. However, catastrophic activities, both natural and man-made, might have weighed on underwriting profit.

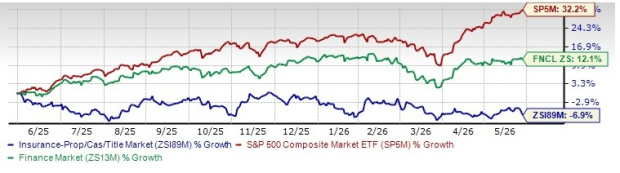

The industry has lost 6.9% over the past year against the Zacks S&P 500 composite's growth of 32.2% and the Finance sector’s return of 12.1%.

Image Source: Zacks Investment Research

Here we focus on two property and casualty insurers, namely Cincinnati Financial Corporation CINF and W.R. Berkley Corporation WRB.

Cincinnati Financial, with a market capitalization of $24.75 billion, provides property casualty insurance products in the United States. W.R. Berkley, with a market capitalization of $23.93 billion, is an insurance holding company that provides property and casualty reinsurance products and operates as a commercial line writer worldwide. CINF and WRB carry a Zacks Rank #3 (Hold) each at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Driving Forces

Global commercial insurance rates declined, on average, by 5% in the first quarter of 2026, following a 4% decline in the fourth quarter of 2025. This marked the seventh consecutive quarter of rate decreases, per the Marsh Global Insurance Market Index. The downward rate movement continues to be driven by abundant capacity and intense insurer competition across most major product lines, per the Marsh Global Insurance Market Index.

Price hikes, operational strength, higher retention, strong renewal and the appointment of retail agents should help write higher premiums. Per Deloitte Insights, gross premiums are estimated to exceed $722 billion by 2030.

Aon has estimated that global insured catastrophe losses amounted to at least $20 billion in the first quarter of 2026, 6% above the 21st-century average. Aon’s report also noted that natural catastrophes in the United States accounted for more than 75% of global insured losses in the first quarter of 2026, reaching around $16 billion.

Per Gallagher Re, global natural catastrophe events in the first quarter of 2026 resulted in an estimated $58 billion in direct economic losses. Per Gallagher Re, in the first quarter of 2026, global and regional natural catastrophe activity and loss totals were comparatively lower than the first three months of previous years.

Underwriting profit is likely to have benefited from better pricing, reinsurance arrangements, portfolio repositioning, reinsurance covers and favorable reserve development.

The Fed left the federal funds rate steady at the 3.5-3.75% target range for a second consecutive meeting in March 2026, in line with expectations. The Fed still projects a single rate cut in 2026, but also expects inflation and economic growth to rise from its previous projections.

A larger investment asset base, strong cash flow from operating activities, higher bond yields and an increase in interest income from fixed-maturity securities are expected to have aided net investment income.

The insurance industry’s increased use of technology like blockchain, artificial intelligence, advanced analytics, telematics, cloud computing and robotic process automation expedites business operations. Insurers continue to invest heavily in technology to improve basis points, scale and efficiencies. These investments are likely to have curbed costs and aided the margins of insurers in the first quarter.

A solid capital position is likely to have aided insurers in strategic mergers and acquisitions to sharpen their competitive edge, expand geographically and diversify their portfolio. Sustained wealth distribution to shareholders via dividend hikes, special dividends and share repurchases instill confidence in the insurers.

Let’s delve deeper into specific parameters to ascertain which P&C insurer is better positioned at the moment.

Price Performance

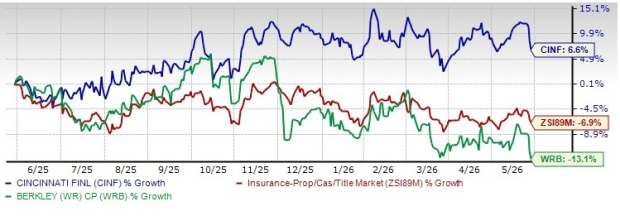

Shares of Cincinnati Financial have climbed 6.6% in the past year against W.R. Berkley’s decline of 13.1%.

Image Source: Zacks Investment Research

Return on Equity

W.R. Berkley, with a ROE of 18.9%, exceeds Cincinnati Financial’s ROE of 10.5% and the industry average of 7.4%.

Image Source: Zacks Investment Research

Valuation

The price-to-book value is the best multiple used for valuing insurers. Compared with WRB’s P/B ratio of 2.46, CINF is cheaper, with a reading of 1.58. The P&C insurance industry’s P/B ratio is 1.35.

Image Source: Zacks Investment Research

Growth Projection

The Zacks Consensus Estimate for 2026 earnings indicates 8.3% growth from the year-ago reported figure for CINF, while the same for WRB implies an increase of 7.8%.

Dividend Yield

Cincinnati Financial’s dividend yield of 2.3% is better than W.R. Berkley’s dividend yield of 0.5%. Thus, Cincinnati Financial has an advantage over W.R. Berkley on this front.

Revenue Estimates

The Zacks Consensus Estimate for CINF and WRB's 2026 revenues implies a year-over-year increase of 7.9% and 2.8%, respectively.

Therefore, CINF is at an advantage on this front.

Earnings Surprise History

Cincinnati Financial has a solid record of beating earnings estimates in each of the last four quarters, with an average being 27.54%. W.R. Berkley beat earnings estimates in three of the last four quarters and missed in one, with an average being 4.73%.

Hence, CINF has an edge in this regard over WRB.

To Conclude

Our comparative analysis shows that Cincinnati Financial is better positioned than W.R. Berkley with respect to price, valuation, growth projection, dividend yield, earnings surprise history and revenue estimates. Meanwhile, WRB scores higher in terms of return on equity. With the scale majorly tilted toward CINF, the stock appears to be better poised.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Cincinnati Financial Corporation (CINF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).