Costco Wholesale closed out an extraordinary week of mass-retail earnings with a fiscal third-quarter report that showed why the Issaquah-based warehouse giant remains one of the world’s leading retailers.

The company delivered adjusted EPS of $4.93, up 15.2% year over year, on net sales of $69.2 billion, an 11.6% increase from $61.96 billion in the prior-year period. Adjusted EPS topped the Zacks Consensus Estimate of $4.91, while total revenues of $70.5 billion also beat the $69.5 billion consensus expectation. The +11.6% headline growth ran well ahead of what most large-cap retailers managed this earnings cycle.

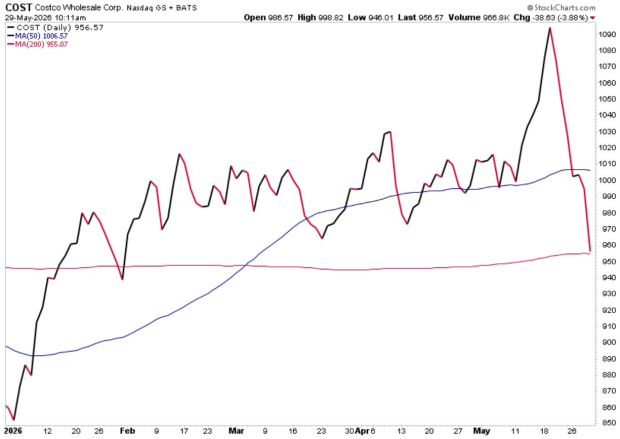

Despite the seemingly solid quarter, Costco shares were down roughly 4% in early trading on Friday morning. Even with today’s decline, the stock is still up nearly 11% year-to-date.

Image Source: StockCharts

Digging Deeper into Costco’s Results

The comparable sales figures continued to underscore Costco's structural advantage in the current retail environment. Total company comp sales rose 9.8%, or 6.6% on an adjusted basis excluding gasoline and foreign exchange impacts. More importantly, U.S. comparable sales advanced 9.4% (6.8% adjusted), Canada came in at 10.7% (6.2% adjusted), and other international markets posted 11.2% (5.9% adjusted).

Comparable traffic grew 2.4% globally, which matters because it means actual member visits are still rising — Costco isn't simply benefiting from inflation in average ticket. Digitally-enabled comparable sales surged 21.5% reported (20.8% adjusted), with site and app traffic up 37%. Stack those numbers against Walmart's +4.1% U.S. comp last week, Sam's Club's +3.9% ex-fuel, and the +0.6% comps at Home Depot and Lowe's, and Costco's continued separation from the rest of the retail pack is hard to miss.

The membership engine — the single best indicator of long-term franchise health — once again held up under scrutiny. The worldwide renewal rate came in at 89.7%, with the U.S./Canada rate at a robust 92.2%. Total cardholders reached 148.5 million, up 4.0%, while paid memberships grew 4.1% to 82.9 million, and Executive memberships expanded to 41.2 million.

Critically, Executive members now account for 75% of total sales, a remarkable concentration that reflects the success of management's strategy to push higher-tier engagement. Membership income grew 10.7% reported and 9.9% excluding foreign exchange, continuing to benefit from the September 2024 fee hike that is still flowing through the model. These are precisely the high-margin, low-capital-intensity dollars that justify the premium Costco multiple, and there were no warning signs anywhere in the membership data.

That said, the margin picture is where the bears found something to chew on. Reported gross margin compressed 21 basis points year over year to 11.04%, though it expanded a single basis point excluding gasoline. The "core on core sales" gross margin, which strips out gas, FX, and the LIFO benefit, declined 9 basis points — modest in absolute terms but notable given that tariffs and elevated input costs have begun pressuring the categories where Costco competes hardest on price.

Importantly, management used the supplemental disclosure to highlight aggressive price investments on key Kirkland Signature items, including price reductions on Kirkland Crispy Wings, milk chocolate almonds, golf balls, and sheets. That investment in everyday-low-price positioning during a period of macroeconomic uncertainty is classic Costco — playing offense on value while peers manage tariff pass-through — but it does suggest that the gross margin line could face modest near-term pressure as the company prioritizes member loyalty over rate.

Costco is taking meaningful share from virtually every adjacent format, and the bifurcated consumer narrative that has dominated the last few earnings seasons continues to favor the warehouse model. The trade-down dynamic that lifted Walmart's transactions has lifted Costco's transactions even more sharply on a relative basis.

Pharmacy, gold and jewelry, home furnishings, tires, housewares, and majors led category growth this quarter — a mix that reflects both staple essentials and select higher-ticket discretionary purchases, suggesting the Costco member is in a noticeably better financial position than the average shopper at a traditional dollar store or mass merchandiser. For BJ's Wholesale, Sam's Club, and the broader discount space, that's both a positive industry tailwind and a competitive warning shot: Costco is not ceding any ground in either price or experience.

Bottom Line

Overall, this was a high-quality quarter from one of retail's most consistent operators. Warehouse expansion remains on track for 940 locations by fiscal year-end, the Executive member penetration is hitting new highs, and digital growth has finally moved from a concern to a contributor.

For long-term investors, any post-earnings weakness in Costco COST has historically been a gift more often than a warning, and the structural advantages — membership economics, supplier leverage, digital acceleration, international runway — remain firmly in place.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).