Western Digital Corporation WDC is gaining from strong demand across its cloud, consumer and client businesses, which helped drive significant gross margin expansion in the third quarter of fiscal 2026. The company reported a gross margin of 50.5%, up 1,040 basis points year over year and 440 basis points sequentially. Management stated that the improvement was driven by a favorable mix shift toward higher-capacity drives, continued execution of its pricing strategy and disciplined cost controls across the supply chain.

Western Digital highlighted that its focus on delivering better total cost of ownership for customers through higher-capacity drives and increasing adoption of UltraSMR technology continued to support profitability. The company noted that strong pricing trends also contributed to margin expansion, as the value created through higher-capacity products and technology innovation enabled improved pricing across cloud, client and consumer businesses. Revenues for the fiscal third quarter increased 45% year over year to $3.3 billion, supported by strong demand for nearline storage products and higher-capacity ePMR drives.

Management emphasized that pricing, product mix and cost reductions remain the three primary drivers of gross margin improvement. WDC stated that pricing during the quarter was slightly better than expected, while the transition toward higher-capacity drives and broader UltraSMR adoption continued to improve product mix. At the same time, operational teams continued executing on supply chain efficiencies and cost-reduction initiatives.

Looking ahead, Western Digital expects additional gross margin improvement in the fiscal fourth quarter, guiding margins in the range of 51% to 52%. The company believes ongoing adoption of UltraSMR technology, increasing shipments of higher-capacity ePMR drives and the future ramp of HAMR drives will continue supporting margin expansion. Management also noted that the strong pricing environment and continued operational execution position the company well for sustained profitability improvement going forward.

Taking a Look at WDC’s Competitors’ Margin Growth

Seagate Technology Holdings plc STX has been sustaining strong gross margin expansion through a combination of disciplined pricing, improving product mix and the rapid adoption of its HAMR-based Mozaic platform. In the third quarter of fiscal 2026, Seagate reported a record non-GAAP gross margin of 47%, up 480 basis points (bps) sequentially and roughly 1,080 bps year over year. For the fiscal fourth quarter, it expects revenues of $3.45 billion (+/- $100 million). At the midpoint, this indicates a 41% year-over-year improvement. At the midpoint of revenue guidance, non-GAAP operating margin is projected to increase in the low 40% range.

Sandisk SNDK is benefiting from AI-led demand that is lifting enterprise SSD adoption and supporting pricing across NAND end markets. Recent margin expansion and rising free cash flow have moved Sandisk to a net cash position and enabled a share repurchase authorization. Non-GAAP gross margin expanded to 78.4% from 51.1% in second-quarter fiscal 2026, and management guided to 79% to 81% for fourth-quarter fiscal 2026. Even with bit shipments down high-teens sequentially in third-quarter fiscal 2026 as inventory builds ahead of the QLC ramp and new contracts, the margin profile indicates Sandisk is prioritizing value over volume. For the fourth quarter of fiscal 2026, Sandisk expects revenues of $7.75-$8.25 billion and non-GAAP earnings of $30-$33 per share. Management guided to a non-GAAP gross margin of 79%-81%.

WDC’s Price Performance, Valuation & Estimates

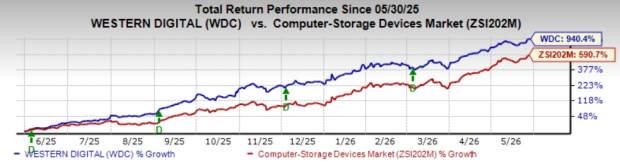

In the past year, shares of WDC have skyrocketed 940.4% compared with the Zacks Computer-Storage Devices industry’s growth of 590.7%.

Image Source: Zacks Investment Research

In terms of forward price/earnings, WDC shares are trading at 33.03X, higher than the industry’s 13.71X.

Image Source: Zacks Investment Research

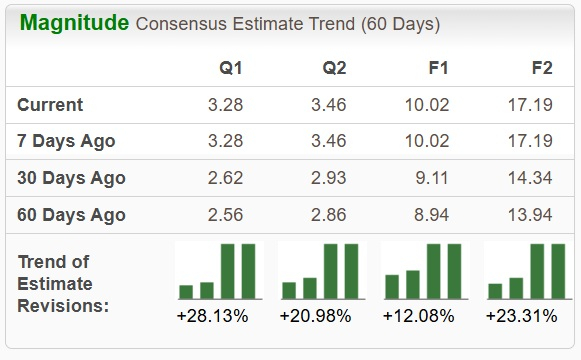

WDC’s estimate revisions are currently on an upward trajectory. The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised north 12% to $10.02 over the past 60 days, while the same for fiscal 2027 has gone up 23.3% to $17.19.

Image Source: Zacks Investment Research

Currently, Western Digital sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

Sandisk Corporation (SNDK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).