Micron Technology MU) is back on the coveted Zacks Rank #1 (Strong Buy) list after a very brief hiatus.

Before slipping from this top rank, MU had been the longest-running Strong Buy recommendation from Zacks, climbing more than 700% from the time it first earned the designation in August of last year, when I covered the stock shortly after as the Bull of the Day, stating it was still flying somewhat under the radar…..

Fast forward, and MU has climbed from $117 a share at the time of that Bull of the Day writing to nearly $1,000 a share at the time of this one.

While Micron has already delivered monster gains for investors, the semiconductor leader still looks poised for further upside as artificial intelligence spending continues to reshape the memory chip market.

Of course, some investors may feel like they’ve already missed the big move higher, but Micron’s combination of record earnings growth, expanding margins, and unprecedented visibility into future demand suggests the rally may be far from over.

To that point, Micron has become one of the most important suppliers in the AI ecosystem, and Wall Street may still be underestimating how dramatically the memory chip industry has evolved beyond its traditionally cyclical nature.

Image Source: Zacks Investment Research

AI Has Transformed the Memory Market

For years, memory manufacturers were viewed as highly cyclical businesses prone to boom-and-bust swings. However, the AI revolution is creating a fundamentally different demand environment.

High-bandwidth memory (HBM) has become a critical component in advanced AI accelerators from companies like Nvidia NVDA). These chips require enormous amounts of ultra-fast memory to process and move data efficiently. As AI infrastructure spending continues to surge, demand for HBM remains significantly ahead of supply. Micron has stated that its HBM production is effectively sold out through 2026, providing a level of revenue visibility that memory companies have historically never enjoyed.

This supply-demand imbalance has created substantial pricing power for Micron, allowing the memory chip leader to generate record profitability while securing long-term customer commitments.

Record Results Continue to Impress

Micron's recent financial performance highlights the strength of this long-term growth trend.

Most recently reporting results for its fiscal second-quarter at the end of March, Micron’s Q2 revenue nearly tripled year over year to $23.86 billion from $8.7 billion a year ago. Furthermore, this was up 75% sequentially, from revenue of $13.64 billion in Q1.

Meanwhile, adjusted earnings skyrocketed 682% YoY to $12.20 per share while operating cash flow ballooned to nearly $12 billion. Management also projected another record quarter ahead, citing strong demand, tight industry supply, and continued momentum across AI-related products.

CEO Sanjay Mehrotra noted that Micron set records for revenue, gross margin, earnings per share, and free cash flow, with expectations for additional records in Q3 when the company reports on Wednesday, June 24.

Perhaps most importantly, these gains aren't being driven solely by a one niche product category. Growth has spread across DRAM, NAND, data-center memory, mobile, automotive, and embedded markets, demonstrating broad-based strength throughout Micron’s business segments.

Why MU's Rally May Continue

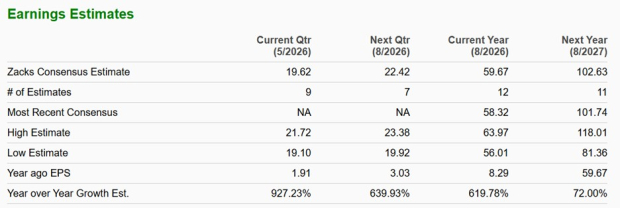

Notably, several catalysts could keep driving MU shares higher, with it noteworthy that Micron’s annual earnings are now expected to soar over 600% this year to $59.67 per share. Plus, FY27 EPS is projected to spike another 72% to an astonishing $102.63.

Image Source: Zacks Investment Research

1. First, hyperscale cloud providers continue investing aggressively in AI infrastructure. Every new generation of AI servers requires larger quantities of high-performance memory, creating a powerful tailwind for Micron.

2. Second, industry supply remains constrained. The technical complexity of HBM manufacturing limits how quickly competitors can add capacity. Even as companies like Samsung and SK Hynix increase HBM production, demand continues to outpace available supply. Analysts estimate the HBM market could roughly double between 2026 and 2027.

3. Third, Micron's earnings power has increased dramatically. Higher-margin AI products are becoming a larger percentage of revenue, supporting significant gross-margin expansion and cash-flow generation. Several Wall Street firms have recently raised their price targets as EPS expectations keep moving higher.

(4). Micron’s Valuation is Still Very Reasonable

Despite Micron’s impressive run, valuation remains one of the strongest parts of its bull case, even with MU commanding quite a lofty price tag but trading at just 15X forward earnings.

Many AI beneficiaries trade at much higher premium multiples reflecting years of anticipated growth. Micron, however, continues to trade at a valuation that suggests investors remain skeptical about the durability of current earnings levels.

That said, some analysts are increasingly arguing that AI-driven memory demand is more structural than cyclical, which could justify a higher earnings multiple over time. If Micron continues to deliver strong execution while AI spending remains robust, investors could see both earnings growth and further multiple expansion.

Image Source: Zacks Investment Research

Conclusion & Final Thoughts

Micron has evolved from a traditional memory-chip manufacturer into one of the most important enablers of the AI revolution. Record earnings, sold-out HBM capacity, strong pricing power, and expanding margins provide a compelling foundation for continued growth.

Although volatility should be expected after such a powerful rally, the fundamental drivers behind Micron's business remain firmly intact. As long as AI infrastructure spending continues to accelerate, Micron appears well-positioned to remain one of the biggest winners in the semiconductor space.

For growth investors looking for continued exposure to the AI buildout, Micron Technology still looks like a stock worth buying.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Micron Technology, Inc. (MU): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).