WEX WEX is benefiting from its multi-channel offerings of corporate payment solutions across a wide spectrum of sectors, including fleet, travel and healthcare. Strong segment momentum, disciplined operational execution and artificial intelligence ("AI") innovation further support long-term growth.

The company’s second-quarter 2026 earnings are expected to increase 24.1% year over year. Earnings for 2026 and 2027 are projected to rise 17.6% and 5.3%, respectively, year over year. Revenues are expected to increase 6.8% in 2026 and 2.4% in 2027.

Factors That Bode Well for WEX

WEX is driving growth through strong financial performance across its segments. The Mobility, Benefits and Corporate Payments segments collectively provide a competitive advantage through exposure to large, growing and operationally complex markets.

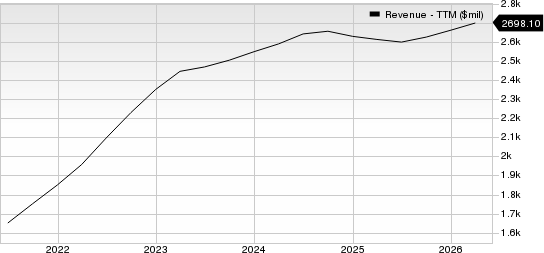

WEX Inc. Revenue (TTM)

WEX Inc. revenue-ttm | WEX Inc. Quote

The Mobility segment, which generates roughly half of WEX's total revenues, reported 3.2% year-over-year growth in the first quarter of 2026. Management emphasized that the company's focus on controlling pricing, sales productivity, product expansion and customer execution is producing significant results.

WEX’s Benefits segment is also generating higher revenues, supported by technology investments that are improving the customer experience. Revenues from this segment increased 8.5% year over year in the last reported quarter, supported by a successful open enrollment season and continued growth in health savings account ("HSA") offerings. HSA accounts on the platform rose 8% year over year to $9.4 million, while average HSA custodial cash assets increased 11.8% over the same period.

The Corporate Payments segment has also remained a strong growth catalyst for the company. WEX reported that this segment’s revenues increased 9.3% year over year to $113 million in the first quarter of 2026. Travel-related revenues in the segment grew approximately 12% year over year during this period, supported by strong customer demand and strategic partnerships.

The company also pursues AI innovation to drive long-term growth. Per management, leveraging AI and investing in AI are improving WEX’s customer-facing solutions by enhancing claims processing, spend visibility, customer service, credit management and payment outcomes. WEX is also planning to deliver approximately $50 million in cost-saving actions during 2026 through automation, modernization and process improvements.

Risks to Watch

WEX carries an elevated debt burden stemming from past buyouts and expansions. In the first quarter of 2026, total debt was 73.9% of WEX’s total capital, well above the industry average of 46.2%. Although these activities have benefited the company, the proportion of total debt to total capital is concerning compared with the industry average and its past performance.

Fluctuations in fuel prices affect WEX’s revenues, mainly through the Mobility segment, its largest top-line contributor. Consistently higher fuel prices are leading customers to reduce driving and fuel consumption. Limiting mileage to save on fuel costs can reduce overall transaction volumes.

WEX has never declared and has no plans to pay cash dividends. This may discourage income-seeking investors, leaving returns dependent solely on share price appreciation. Since share price appreciation is variable, dividend-focused investors may be reluctant to rely on it.

WEX currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

A couple of better-ranked stocks in the Business Services sector are FactSet Research Systems Inc. FDS and TransUnion TRU.

FactSet Research Systems Inc. carries a Zacks Rank #2 (Buy) at present. It has a long-term earnings growth expectation of 6.5%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

FDS' earnings beat estimates in two of the last four reported quarters and missed twice, delivering an average surprise of 0.4%.

TransUnion also holds a Zacks Rank of 2 at present. It has a long-term earnings growth expectation of 13.5%.

TRU's earnings beat estimates in each of the last four quarters, with the surprise being 6.3%, on average.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FactSet Research Systems Inc. (FDS): Free Stock Analysis Report

WEX Inc. (WEX): Free Stock Analysis Report

TransUnion (TRU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).