Meta Platforms (META) is entering a delicate new phase of the artificial intelligence (AI) race. After spending tens of billions of dollars on AI infrastructure, custom chips, and massive data center expansion, the social media giant is now searching for ways to convince investors that the spending spree will eventually pay off. That pressure is becoming increasingly visible. Meta recently unveiled paid subscription tiers for its AI chatbot across Facebook, Instagram, and WhatsApp, while simultaneously pushing through another major round of layoffs, as soaring AI compute costs weigh on margins.

The new monetization push is expected to include Meta AI subscription plans priced at $7.99 per month for the basic tier and $19.99 per month for the Premium tier, alongside new Facebook Plus and Instagram Plus subscriptions at $3.99 monthly and WhatsApp Plus at $2.99. Meta says the paid offerings will unlock higher AI usage limits, advanced image and video generation tools, and premium engagement features across its platforms.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For META stock bulls, the challenge is no longer convincing Wall Street that AI is transformative. It is proving that the economics can work before infrastructure costs spiral too far ahead of revenue. With projected 2026 capital expenditures reaching as high as $145 billion, Meta is increasingly being forced to monetize AI faster than originally expected. Subscription products, workforce reductions, and aggressive efficiency measures are all becoming part of Zuckerberg’s strategy to fund one of the largest AI buildouts in corporate history.

About Meta Stock

Meta Platforms is a technology conglomerate headquartered in Menlo Park, California, best known for owning and operating some of the world’s most influential social media and communication platforms, including Facebook, Instagram, WhatsApp, Messenger and Threads. Originally founded as Facebook in 2004, the company rebranded to Meta in 2021 to reflect its strategic pivot toward immersive technologies such as virtual reality, augmented reality, and the metaverse.

In addition to its flagship apps, Meta develops hardware and AI-driven products through divisions like Reality Labs, spanning VR headsets and smart glasses. Meta’s market cap stands at $1.6 trillion, ranking it among the largest technology companies globally.

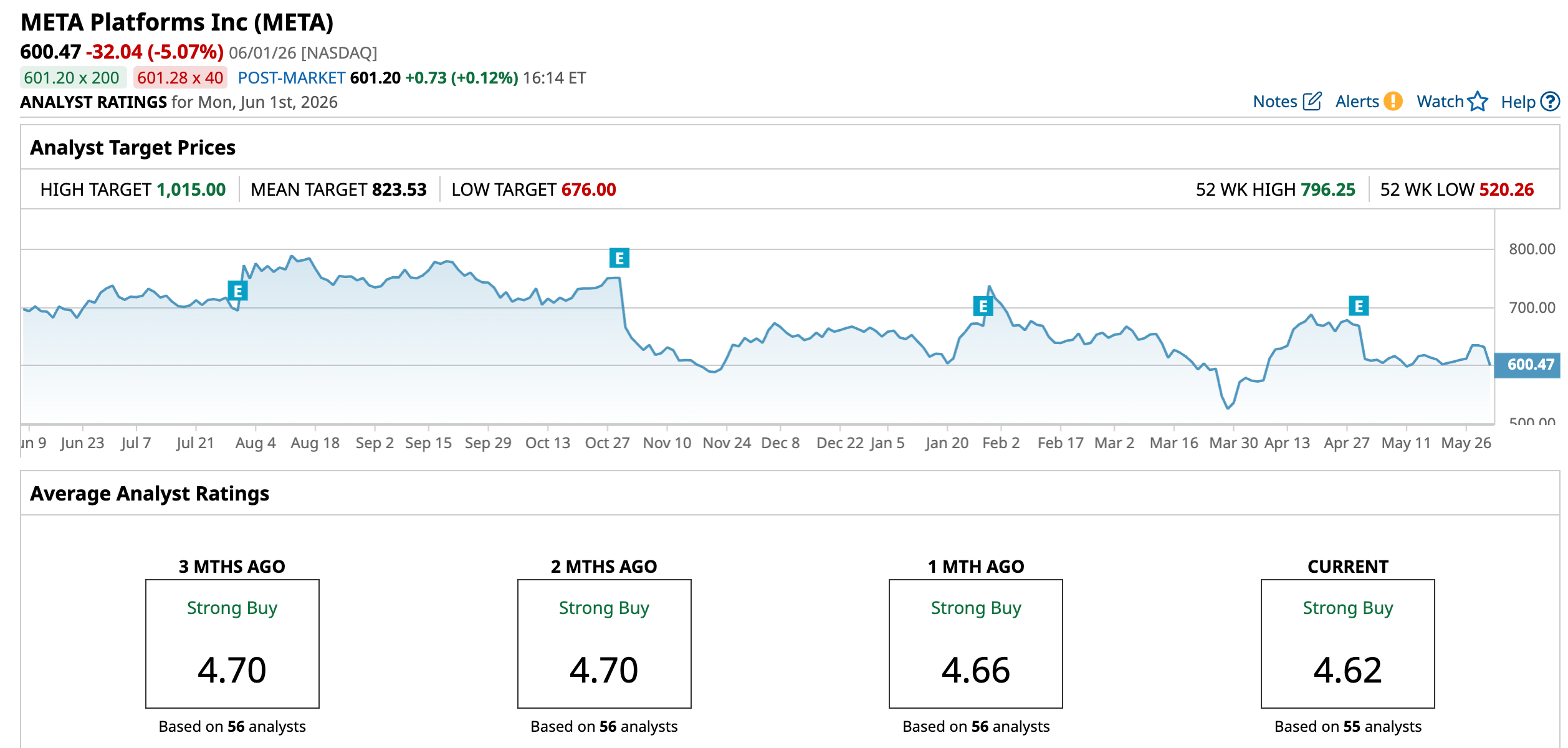

Meta stock has lost momentum in 2026 as investors grow increasingly uneasy about the company’s enormous AI spending plans. After hitting a 52-week high of $796.25 last August, META has fallen 24.6% from those peak levels. The stock is down 8.45% year-to-date (YTD) and has declined 6.67% over the past 52 weeks despite continued strength in Meta’s advertising business.

The recent weakness accelerated after Meta sharply raised its 2026 higher end of the capital expenditure forecast to as much as $145 billion, intensifying Wall Street concerns about whether the company can monetize AI investments quickly enough to justify the spending. Shares dropped 8.6% on April 30, following the latest earnings report as investors reacted to soaring costs.

In spite of the muted performance, Meta remains one of the market’s largest and most profitable technology companies, with many analysts arguing that the stock’s pullback reflects short-term fears surrounding AI monetization rather than deterioration in the core business. Bulls believe the company’s push into chatbot subscriptions, AI-powered advertising, and premium social platform features could eventually help offset the massive compute costs currently pressuring investor sentiment.

www.barchart.com

www.barchart.com META currently trades at a premium compared to the sector median but below its own historical average at 22.45 times forward earnings (Non-GAAP).

Steady Top-Line Growth

Meta Platforms released its first quarter 2026 financial results on Aprik 29, delivering another strong quarter of advertising-driven growth while dramatically increasing its AI infrastructure spending plans. Revenue surged 33% year-over-year (YOY) to $56.3 billion. The strong top-line growth was fueled by continued improvements in AI-powered ad targeting, higher user engagement across Instagram and Facebook, and rising monetization efficiency.

Operating income increased 30% YOY to $22.9 billion, while operating margin remained steady at 41% despite sharply higher infrastructure spending. Total costs and expenses climbed 35% to $33.4 billion as Meta accelerated investments in AI chips, data centers, and computing capacity.

Net income jumped 61% YOY to $26.8 billion, while earnings per share rose 62% to $10.44 from $6.43.

Meta’s core advertising engine remained exceptionally strong during the quarter. Ad impressions increased 19% YOY while the average price per ad rose 12%. Family Daily Active People climbed 4% YOY to 3.6 billion users.

Also, cash generation remained robust. Operating cash flow reached $32.2 billion, while free cash flow rose to $12.4 billion. Cash, cash equivalents, and marketable securities stood at $81.2 billion at quarter-end.

The biggest investor concern came from Meta’s updated guidance. Management projected second-quarter 2026 revenue between $58 billion and $61 billion, implying continued strong growth momentum. However, the company sharply raised its full-year 2026 capital expenditure forecast to between $125 billion and $145 billion, up from the prior range of $115 billion to $135 billion. Meta cited higher AI chip pricing and additional data center expansion costs as the primary drivers behind the increase.

And, Meta reaffirmed its expectation for full-year 2026 expenses between $162 billion and $169 billion. The massive AI spending escalation overshadowed the otherwise impressive earnings report and triggered a sharp selloff in the stock after results were released.

Analysts predict EPS to be around $29.35 for fiscal 2026, down 1.15% YOY, before surging by 19.28% annually to $35.01 in fiscal 2027.

What Do Analysts Expect for Meta Stock?

Most recently, Citizens reiterated a “Market Outperform” rating and $825 price target on Meta Platforms, arguing the company could revive its push into on-platform shopping through a new partnership with Stripe. The collaboration uses Stripe’s Agentic Commerce Suite to create a streamlined checkout experience that allows users to complete purchases with saved payment credentials in just a few taps.

Plus, Rosenblatt reiterated a “Buy” rating and $1,015 price target on Meta Platforms after the company unveiled plans to launch subscription offerings across Instagram, Facebook, WhatsApp, and Meta AI.

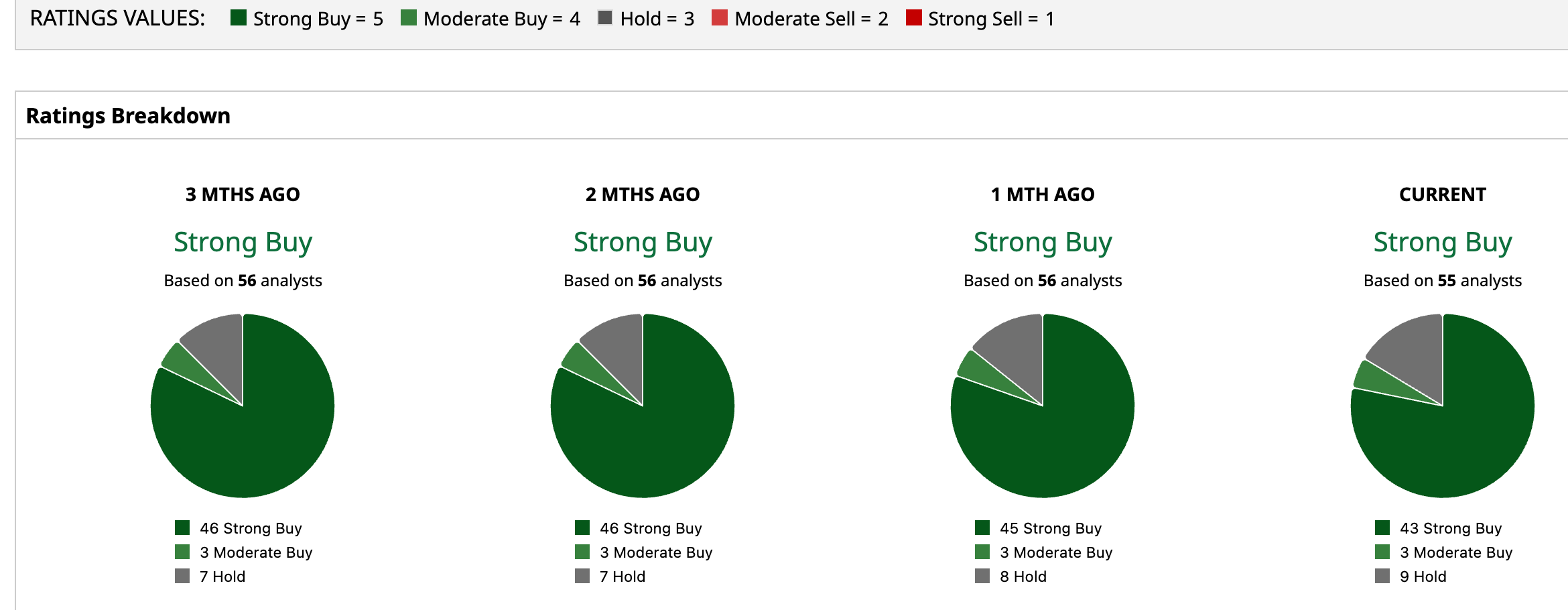

Overall, META has a consensus “Strong Buy” rating. Of the 55 analysts covering the stock, 43 advise a “Strong Buy,” three suggest a “Moderate Buy,” and the remaining nine analysts are on the sidelines, giving it a “Hold” rating.

The average analyst price target for META is $823.53, indicating a potential upside of 37.15%. Rosenblatt’s Street-high target price of $1,015 suggests that the stock could rally as much as 69%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FedEx Freight Stock Starts Trading June 1 as a Member of the S&P 500. How to Play FDXF Here. Meta Is Launching Chatbot Subscriptions. META Stock Bulls Need a Way to Justify AI Costs. Citi Just Raised Its Price Target on Nebius to a New Street High of $287. What This Means for NBIS Stock. Nvidia’s AI Monopoly Could Push It to Become a $10 Trillion Company by 2030