NGL Energy Partners LP NGL used its fourth-quarter 2026 call to sharpen the case for its water-focused transformation. Management emphasized stronger contracted growth, a cleaner portfolio and another year of expected EBITDA expansion.

That message mattered more than the headline earnings miss. Executives framed fiscal 2027 as a continuation of the same playbook that drove record Water Solutions results in fiscal 2026.

NGL Leans Further Into Water

Chief executive officer H. Michael Krimbill said fiscal 2026 marked another step toward a less volatile, higher-quality business centered on water infrastructure. Chief financial officer Brad Cooper echoed that theme, describing Water Solutions as the partnership’s core growth engine.

That emphasis was backed by results. Water Solutions delivered fourth-quarter adjusted EBITDA of about $153 million and full-year adjusted EBITDA of roughly $603 million, both company records. Produced water volumes disposed rose 10% year over year in the quarter to about 3.01 million barrels per day.

Cooper also highlighted improving contract quality. Disposal volumes under commitments increased to 53% from 45% during the fiscal year, while more than 90% of volumes are now supported by minimum volume commitments or acreage dedications.

NGL Energy Pushes 2027 Growth

Krimbill said NGL expects consolidated adjusted EBITDA of $715 million to $725 million in fiscal 2027, implying roughly 10% growth at the high end from fiscal 2026’s $660.2 million. Management said that growth should come primarily from Water Solutions and already contracted projects.

The call made clear that guidance rests on visible projects rather than new wins. Cooper said the outlook excludes any contracts signed after the call date and does not include benefits from current crude oil price levels.

Management also guided to about $200 million of growth capital and $45 million of maintenance capital in fiscal 2027. Cooper later told analysts that the bulk of the growth spending is tied to the LEX II expansion and will largely fall in the first two to three quarters of the fiscal year.

NGL Keeps Working the Balance Sheet

Cooper presented balance-sheet cleanup as another central pillar. NGL completed a $950 million refinancing transaction during the quarter, extending maturities and creating room to reduce its Class D preferred units.

Over fiscal 2026, the partnership repurchased 284,511 Class D preferred units, or about 47% of the original amount outstanding. It also bought back 8.7 million common units at an average price of $5.72 and later approved a new $100 million repurchase authorization.

Management’s tone was disciplined rather than aggressive. Cooper said the strategy remains to use free cash flow and noncore asset sales to keep reducing higher-cost capital, with broader capital-markets actions tied to leverage reaching an appropriate level.

NGL Energy Streamlines the Portfolio

Cooper said the sale of the wholesale propane and rack marketing businesses was a major step in reducing earnings volatility. The partnership is positioning itself as a pure-play water company, with the remaining Liquids assets still viewed as non-core.

That repositioning changed the earnings mix. Liquids Logistics generated about $17 million of fourth-quarter adjusted EBITDA and was described as smaller, more stable and less seasonal after divestitures.

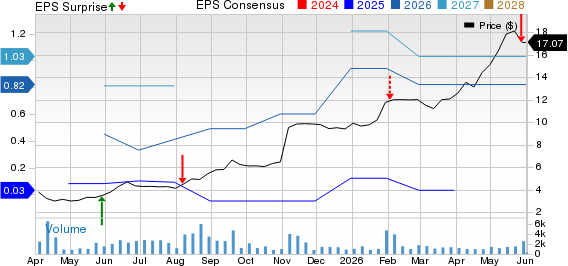

The quarter’s reported loss was heavily influenced by non-core items. NGL posted a loss from continuing operations of $286.8 million, including a goodwill impairment charge, while adjusted EBITDA from continuing operations was $176.4 million. Revenue of $949.5 million topped the Zacks Consensus Estimate of $776.04 million by 22.35%. The company incurred a loss of 71 cents per share in contrast to the consensus estimate of earnings of 18 cents per share, producing a negative surprise of 494.4%.

NGL Energy Partners LP Price, Consensus and EPS Surprise

NGL Energy Partners LP price-consensus-eps-surprise-chart | NGL Energy Partners LP Quote

NGL Sees More Demand in the Basin

Analyst Derrick Whitfield of Texas Capital Securities pressed management on how much more capacity the basin may need beyond the latest LEX II expansion. Executive vice president Douglas White responded with one of the clearest messages from the Q&A, saying demand for additional capacity remains extremely strong.

White said the latest expansion mainly amends and extends an existing customer agreement, adding longer-term volume commitments and a four-township dedication in Eddy County. Earlier in prepared remarks, Cooper said the project adds 165,000 barrels per day of capacity and can lift LEX II throughput to about 560,000 barrels per day, with room to expand to 650,000.

On activity levels, White said the recent pull-forward in drilling is less important than the broader shortage of available water-handling capacity. He tied demand growth to sustained development activity and operational efficiencies rather than commodity-price swings alone.

NGL Energy Leaves a Focused Message

The clearest takeaway from the call was consistency. Management presented fiscal 2027 as an extension of the same formula: invest behind contracted water projects, exit non-core businesses and keep simplifying the capital structure.

Executives also sounded constructive on adjacent opportunities. Cooper said NGL is making progress on previously discussed desalination and energy campus projects, including a draft permit process with TCEQ, but the company’s near-term message stayed centered on its existing water franchise.

Zacks' Signals on NGL

NGL carries a Zacks Rank #3 (Hold), along with a Value Score of B, Growth Score of D, Momentum Score of A and VGM Score of C. In Zacks’ framework, a Rank #3 can be held, while better Style Scores signal stronger expected performance within that rank. A strong Momentum Score stands out, while the weaker Growth Score tempers the profile.

The broader read is mixed rather than directional. Zacks says the most favorable setups tend to pair a Zacks Rank #1 (Strong Buy) or #2 (Buy) with Style Scores of A or B, while Rank #3 names can still be held with attention to the score hierarchy. That also means NGL’s current rank and scores should be viewed as fluid after earnings, since estimate revisions can change the Zacks Rank over time.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NGL Energy Partners LP (NGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).