Lattice Semiconductor Corporation LSCC is steadily strengthening its position in the semiconductor equipment space with a holistic growth focus, balancing organic and inorganic initiatives. The company is benefiting from strong momentum in the artificial intelligence (AI) server market, driven by rising deployment of AI infrastructure across hyperscale and enterprise data centers. It continues to witness an increasing demand for its low-power field-programmable gate arrays (FPGAs), which are widely used in server management, connectivity, security and edge AI applications.

LSCC Rides on Portfolio Strength

Lattice Semiconductor’s differentiated low-power FPGA portfolio remains a major growth driver. The company focuses on power-efficient programmable solutions, which are increasingly preferred by customers looking to optimize thermal performance and reduce energy consumption in AI environments.

The company’s expanding portfolio is helping strengthen its presence across communications, computing, industrial and automotive end markets. Its newer FPGA platforms are witnessing solid adoption, supported by rising demand for flexible and energy-efficient solutions. Lattice Semiconductor’s focus on low-power applications differentiates it from its peers and positions it well to capitalize on the growing need for efficient AI infrastructure solutions.

Improving Demand Trends Support Outlook

The company is benefiting from improving inventory conditions and healthy booking activity, which are supporting better demand visibility. AI-related applications continue to remain a key growth catalyst. In addition, a favorable product mix and pricing discipline are supporting healthy profitability metrics. Increasing contribution from higher-value AI and server applications is expected to drive operating leverage over the long term.

Healthy Traction from Inorganic Growth

Lattice Semiconductor's acquisition of AMI marks a significant step toward expanding its presence in the rapidly growing AI infrastructure and datacenter markets. The transaction combines its low-power programmable logic portfolio with AMI's platform firmware and remote management software capabilities, creating a more comprehensive hardware-software offering for server and cloud customers. The deal strengthens LSCC's competitive position in system control, security and manageability applications, which are becoming increasingly important as AI deployments scale across enterprise and hyperscale environments.

The acquisition is expected to enhance Lattice Semiconductor's long-term growth prospects by broadening its addressable market and increasing its exposure to high-value software-driven revenue streams. Management expects AMI to contribute more than $200 million in revenue in 2026, while the transaction is projected to be accretive to non-GAAP earnings, gross margin and free cash flow. The addition of AMI's established customer relationships and software expertise should create cross-selling opportunities across Lattice Semiconductor's existing FPGA customer base, supporting revenue diversification and improving growth visibility.

Image Source: Zacks Investment Research

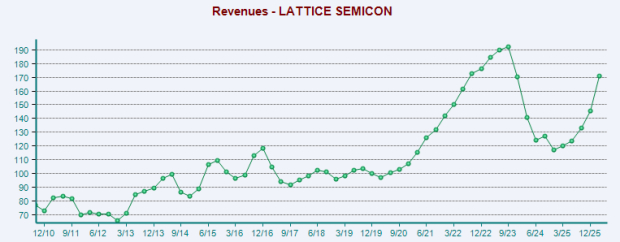

Price Performance

Lattice Semiconductor has surged a stellar 211% in the past year compared with the industry’s growth of 107%. It has outperformed peers like Diodes Incorporated DIOD but lagged ASE Technology Holding Co., Ltd. ASX. While Diodes has gained 118.8%, ASX has jumped 302.6% over this period.

One-Year Price Performance of LSCC

Image Source: Zacks Investment Research

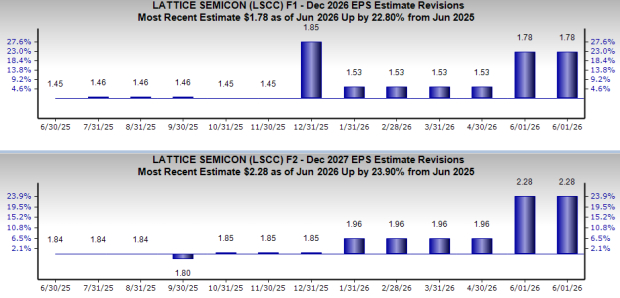

Estimate Revision Trend

Earnings estimates for Lattice Semiconductor for 2026 and 2027 have moved up 22.8% to $1.78 and 23.9% to $2.28, respectively, since June 2025. The positive estimate revision depicts bullish sentiments about the stock’s growth potential.

Image Source: Zacks Investment Research

Moving Forward

Lattice Semiconductor remains well-positioned to benefit from expanding AI infrastructure spending and increasing FPGA adoption across data center environments. As cloud providers continue to expand AI workloads, LSCC is benefiting from broader adoption opportunities across next-generation server architectures. Its strong low-power FPGA portfolio, growing exposure to AI servers and software expansion efforts provide multiple long-term growth drivers.

The firm delivered a trailing four-quarter average earnings surprise of 3.5%. It has a long-term earnings growth expectation of 39.8%. Lattice Semiconductor currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Riding on a robust earnings surprise history and favorable Zacks Rank, it appears primed for further stock price appreciation. Consequently, investors are likely to profit if they bet on this high-flying stock now.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lattice Semiconductor Corporation (LSCC): Free Stock Analysis Report

Diodes Incorporated (DIOD): Free Stock Analysis Report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).