Dollar General Corporation DG used its first-quarter 2026 earnings call to make a forward-looking case centered less on the headline beat and more on execution. Management stressed that traffic growth, margin expansion and tighter inventory control offset weather disruptions and higher fuel costs.

That message mattered because the company also raised its full-year earnings outlook, while using the call to argue that its value positioning, delivery buildout and remodel program are gaining traction in a pressured consumer environment.

Dollar General Sees Pressure Drive Traffic

Chief executive officer Todd Vasos said the quarter showed Dollar General’s ability to serve a more financially constrained shopper while also pulling in higher-income trade-in customers. He highlighted same-store sales growth of 2.0%, driven by a 1.4% increase in traffic and a 0.5% rise in average ticket.

Vasos said all four merchandising categories posted positive comparable sales for the fifth straight quarter, with non-consumables again outpacing consumables. He also said March benefited from the Easter shift, while February was hurt by winter storms and temporary store closures.

A notable call theme was trade-in behavior. Vasos said customer penetration rose across income groups, with the biggest increase coming from households earning more than $100,000, while core lower-income shoppers remained under pressure from fuel prices and reduced SNAP benefits.

DG Leans on Margin and Inventory Gains

Chief financial officer Donny Lau framed the quarter as proof that multiple margin initiatives are working at once. Gross margin rose 65 basis points to 31.6%, helped by higher markups, lower shrink and lower inventory damages, partly offset by higher markdowns and transportation costs. Operating margin expanded 40 basis points to 5.9%.

Lau said shrink mitigation remained a major contributor, with shrink improving 28 basis points from a year earlier, even against a tougher comparison. He also pointed to better in-store execution on damages and supply chain productivity as support for the company’s longer-term margin framework.

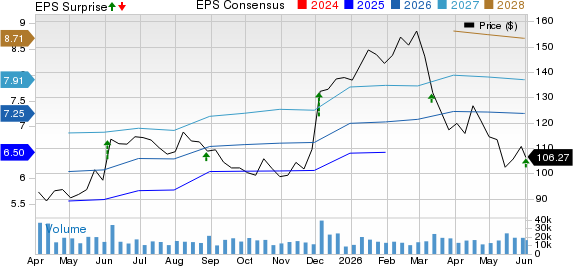

The financial backdrop was solid enough to support an earnings beat despite a revenue miss. DG reported earnings per share of $2.00, topping the Zacks Consensus Estimate of $1.89 by 6.06%. Revenues of $10.79 billion missed the Zacks Consensus Estimate of $10.82 billion by 0.33%. Merchandise inventories were essentially flat year over year at $6.6 billion and down 1.6% on a per-store basis.

Dollar General Corporation Price, Consensus and EPS Surprise

Dollar General Corporation price-consensus-eps-surprise-chart | Dollar General Corporation Quote

Dollar General Raises 2026 View

Management raised full-year 2026 earnings guidance to $7.20 to $7.45 from $7.10 to $7.35. Lau said the higher range reflects first-quarter outperformance, the balance-year outlook and a lower expected tax rate of about 24.5%.

The company now expects net sales growth of 3.7% to 4.2% and same-store sales growth of 2.2% to 2.7%. Capital spending guidance remained unchanged at $1.4 billion to $1.5 billion, and the outlook still assumes no share repurchases this year.

Lau also said the guidance excludes any effect from potential tariff refund payments. He acknowledged continued uncertainty around consumer behavior and elevated fuel costs, but said management still sees more gross-margin tailwinds than headwinds over the rest of the year.

DG Builds Around Delivery and Remodels

Beyond the quarter, management used the call to emphasize initiatives designed to widen the company’s convenience advantage. Chief operating officer Emily Taylor said delivery sales contributed about 70 basis points to comparable-sales growth in the quarter, with larger baskets and strong repeat usage supporting the economics.

Vasos said the company is now delivering from about 18,000 stores through myDG and third-party partners. Taylor added that most orders reached customers in an hour or less, which management sees as a differentiated proposition in rural markets.

Store refreshes were another focal point. Dollar General completed 659 Project Renovate remodels and 711 Project Elevate remodels in the quarter, while maintaining its target for 2,000 Renovate and 2,250 Elevate projects for the year. Management continues to target roughly 6% annualized comparative sales lift from Renovate and 3% from Elevate.

Dollar General Defends Promotions in Q&A

Analyst questions focused heavily on the durability of traffic gains and whether a more promotional retail backdrop could pressure profitability. Vasos told analysts from UBS and Barclays that the company’s added promotions were planned, targeted and proactive rather than reactive, with an emphasis on supporting the core customer and retaining newer trade-in shoppers.

Management also pushed back on the idea that sharper pricing activity signals weakening fundamentals. Vasos argued that Dollar General already holds a strong everyday value position and said the $1 price point, including Value Valley, remains central to both customer acquisition and basket-building behavior. He said Value Valley comparable sales rose 18.4% in the quarter.

Questions from Bernstein and Piper Sandler pressed on margin durability as shrink comparisons get harder and fuel stays high. Lau said the company expects continued, though more modest, gross-margin improvement through the year, supported by shrink, damages, media network growth, category management and supply-chain efficiencies.

DG Leaves the Call With a Clear Playbook

The overall tone of the call was confident but measured. Management repeatedly tied the quarter’s performance to controllable execution rather than a friendlier backdrop, emphasizing value, convenience and operational discipline as the core levers for the rest of 2026.

Just as important, executives used the Q&A to reinforce that the company sees room to grow sales, traffic and margins at the same time, even with macro pressure still evident across its customer base.

Zacks Signals Point to Mixed Near-Term Traits

DG carries a Zacks Rank #3 (Hold), along with a Value Score of A, Growth Score of A, Momentum Score of F and VGM Score of A. Under Zacks methodology, a stronger Style Score can help identify attractive value and growth characteristics, while the weak Momentum Score points to less favorable price-trend support.

A Zacks Rank #3 does not carry the same favorable setup as a Zacks Rank #1 (Strong Buy) or 2 (Buy), even when Style Scores are strong. The combination suggests balanced fundamental traits but a less decisive near-term signal, and that rank can still change as earnings estimate revisions adjust after the quarter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dollar General Corporation (DG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).