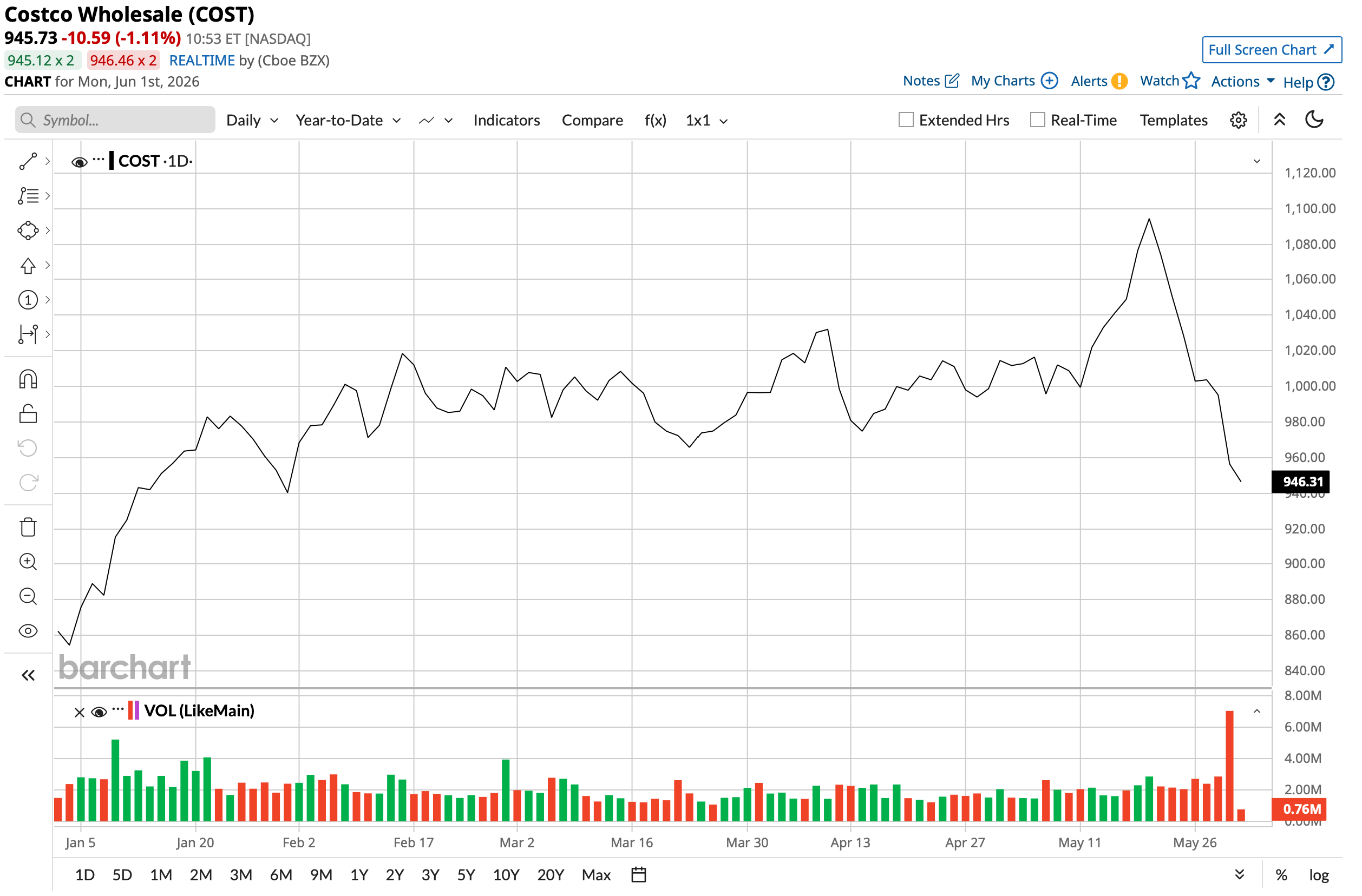

Retail giant Costco Wholesale (COST) hinted on its most recent earnings call that it is looking to pass the benefits of tariff refunds on to customers in some form. However, the market reacted negatively to the news, with COST stock falling by about 4% on May 29.

The negative reaction may not be misplaced. How will the tariff refunds affect COST stock as a whole? Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Costco Stock

Founded in 1983, Costco is one of the most successful retailers in modern history and widely regarded as one of the highest-quality consumer businesses in the world. Unlike traditional retailers, Costco operates a membership-based warehouse club model that prioritizes low prices, limited product selection, high inventory turnover, and exceptional customer loyalty.

Valued at a market capitalization of $426.7 billion, COST stock is up 13% on a year-to-date (YTD) basis. Although the stock offers a modest forward yield of just 0.62%, the company has also raised its dividend for more than two decades now. The payout ratio of 27.2% points to a path of continued growth for the coming years as well.

www.barchart.com

www.barchart.com Costco Reports Q3 Results

The optics of Costco's planned tariff refund returns may be good, but the economic rationale is not, especially considering the company's operating margins which have remained low in the 2.5% to 4% range for years. Instead of being returned to customers, the refunds could have been used to increase the same.

Overall, Costco's third-quarter fiscal 2026 results were decent but not spectacular. Total revenue rose 11.6% year-over-year (YOY) to $70.5 billion, with operating margins at about 4%, flat from the prior-year period. Although Costco's revenue surpassed Street estimates by a wide margin, EPS of $4.93 managed to just match expectations, up 15% YOY. Over the past eight quarters, Costco's earnings have beaten expectations on six occasions.

For the six months ended May 10, 2026, net cash from operating activities rose to $11.1 billion, up from $9.5 billion in the year-ago period. Overall, Costco ended fiscal Q3 with a cash balance of about $18.9 billion.

Despite its relatively unimpressive share price performance, COST stock is trading at overvalued levels. Its forward price-to-earnings (P/E) and price-to-cash flow (P/CF) ratios of 46.8 times and 40.5 times, respectively, are both well above the sector medians. Forward growth rates are also not that exciting at 9% for revenue and 13% for earnings.

Stability in Unstable Times

If Costco's growth is nothing to write home about, what is fueling its punchy valuations? Well, it is the certainty — the stability that Costco offers in tumultuous times.

No matter how dire the situation, essentials will sell, and with a name as credible as Costco's, the retailer will continue to find takers. Further, the durability of consumer demand, a growing membership base, and the ongoing expansion of its warehouse network collectively position the company well for what lies ahead.

Costco's membership model is the engine that makes everything else work, and the numbers in 2025 made a strong case for why Costco remains one of the most durable business moats in retail. Net sales grew 8%, and membership fee revenue climbed 10% in fiscal 2025, even after the company raised fees in September 2024, pushing Gold Star and Business memberships to $65 annually and Executive memberships to $130. The fee hike did not dent loyalty in any meaningful way. In Q3 2026, paid memberships rose 4.1% to 82.9 million while the renewal rate in the U.S. and Canada held at 92.2%, with a global rate of 89.7%.

Higher-paying Executive memberships grew to 41.2 million, and to keep upgrades flowing, Costco introduced extended warehouse hours and a $10 monthly Instacart credit exclusively for Executive members. Management has acknowledged a slight softening in renewal rates tied to younger, digitally acquired members renewing at lower rates. The firm is countering this through auto-renewal features and more targeted digital engagement. Against Walmart's (WMT) Sam's Club and BJ's Wholesale (BJ) — both of which are making real strides in membership income — Costco's sheer scale and Kirkland-driven loyalty keep the gap wide.

Finally, Costco's digital capabilities are resulting in substantial tangible payoffs. AI-powered personalized product recommendation carousels on the online store drove about $5 billion in e-commerce sales in a single quarter. Digitally enabled comparable sales surged 21.5%. On the in-store side, Costco is also piloting automated pay stations that allow members to complete checkout in seconds on pre-scanned orders.

What Do Analysts Think of COST Stock?

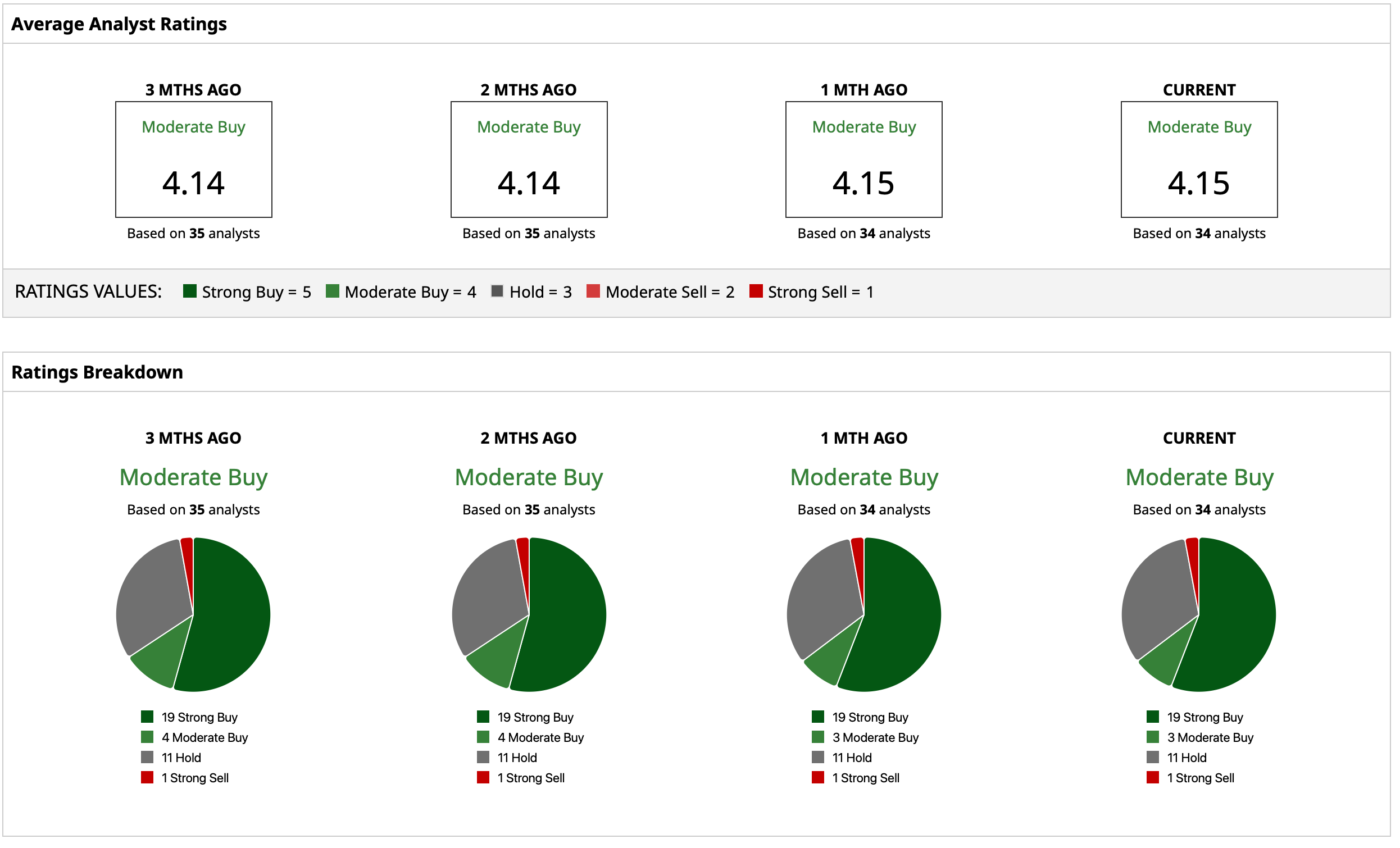

Analysts have a consensus “Moderate Buy” rating on COST stock. The mean target price of $1,099.37 indicates potential upside of about 13% from current levels. Out of the 34 analysts covering Costco stock, 19 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 11 have a “Hold” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Analysts Are Betting Big on DigitalOcean Stock for the Next Era of AI Costco Slips on Plans to Refund Tariff Returns to Customers. The Negative Reaction May Be Deserved. 3 Reasons Why Unusual Options Activity in Progressive Stock May Point to a Bottom IBM Stock’s $10 Billion Quantum Catalyst Is Here