DigitalOcean (DOCN) looks like one of the most compelling AI infrastructure plays in the public markets right now, and Wall Street is finally catching on. KeyBanc Capital Markets just initiated coverage on DigitalOcean with an “Overweight” rating and a $200 price target.

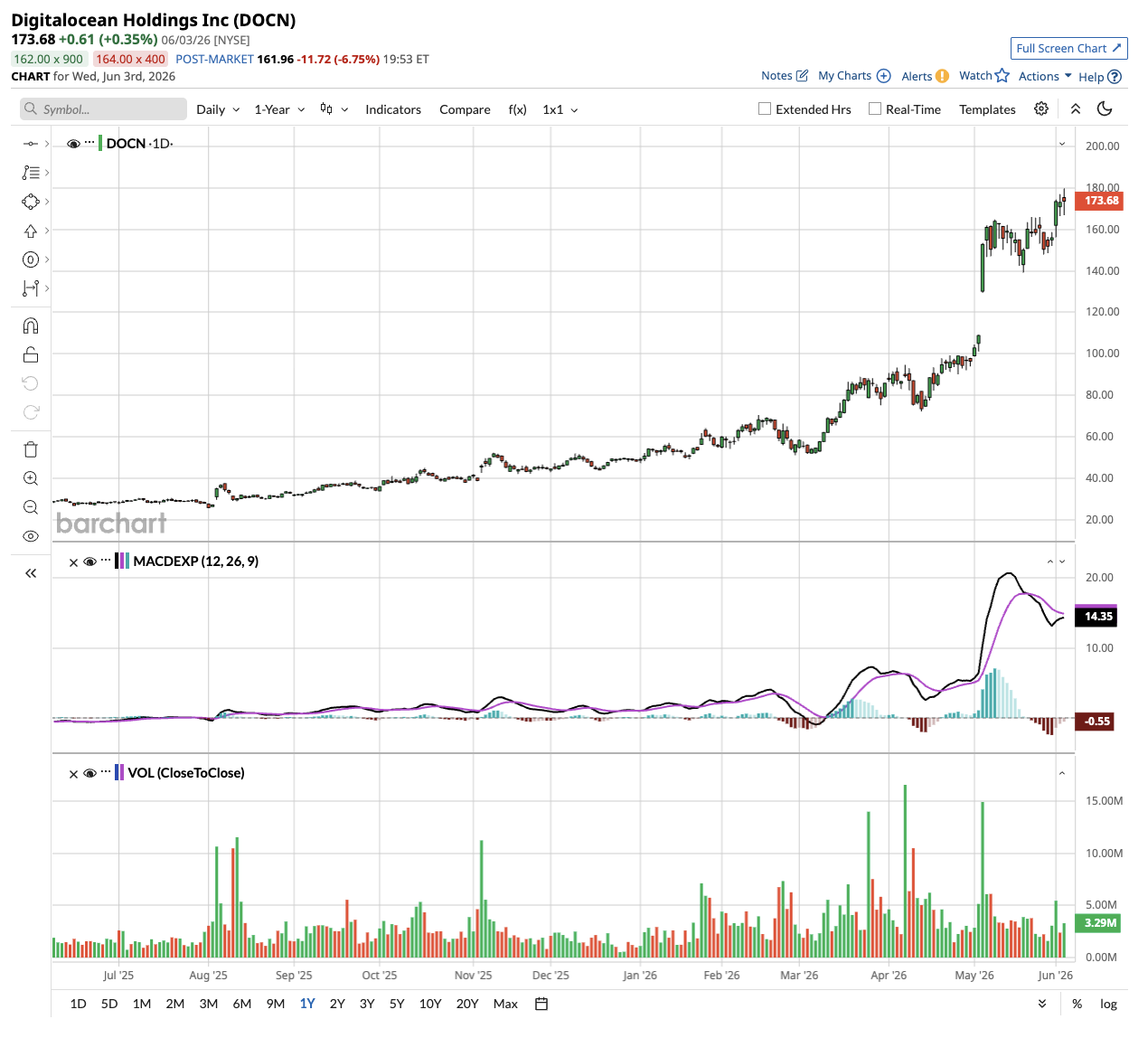

DOCN stock is up over 500% in the past year and could surge 10% from current levels, according to KeyBanc.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comWhy KeyBanc Is Betting Big on DigitalOcean's AI Opportunity

KeyBanc analyst Jackson Ader summed up his core view plainly. The moment arrived for DigitalOcean in 2024, when businesses realized the major hyperscalers couldn't keep up with the surge in demand for artificial intelligence workloads.

Both legacy tech customers and newer AI startups turned to DigitalOcean for AI inference needs. What they found was easy deployment, access to storage, memory, and central processing unit compute that had already been DigitalOcean's specialty.

Ader also laid out the capacity picture in specific terms.

DigitalOcean entered the second quarter of 2026 with just under 50 megawatts of cloud capacity online. Another 25 megawatts are planned to go live over the coming quarters, followed by a recently announced 60-megawatt tranche in 2027. That puts the company at 135 megawatts of contracted capacity. With additional equipment financing and a cleaned-up balance sheet, Ader sees room for even more megawatts coming online in 2028 and 2029.He estimates roughly $15 million in incremental annual recurring revenue per megawatt across the full artificial intelligence and central processing unit cloud stack, which would push estimates meaningfully higher in those years.

DigitalOcean Is Not Just Renting Out GPUs

DigitalOcean is not just a bare metal GPU rental shop. Over 80% of its artificial intelligence revenue now comes from non-bare metal services. The company has built a five-layer integrated software stack that runs from silicon all the way up to the agent layer, and AI-native customers are using it across the stack.

CEO Paddy Srinivasan made the point at a recent JPMorgan conference that agentic applications consume 15 times as many tokens and four times as much central processing unit power as simpler AI tasks.

It is an enormous tailwind for a company whose entire platform is built to handle such layered, complex workloads. And the customers now landing on that platform include AI disruptors such as Cursor, Character.ai, Hippocratic AI, and Ideogram.

These are production workloads for real businesses that cannot afford downtime and winning them away from hyperscalers by delivering 30% to 40% lower total cost of ownership is showing up in the financials.

A Focus on AI Growth

Annual recurring revenue from AI customers is growing at 221% year-over-year. The company's $1 million-plus customer cohort grew 179% year-over-year, with zero churn in that tier over the past four quarters.

CFO Matt Steinfort has noted at multiple investor conferences that the company is adding record levels of incremental organic annual recurring revenue each quarter, and that demand still exceeds available supply by a factor of 3 to 4.

Revenue is now on a path to 25% or more growth in 2027, a dramatic step up from mid-teens growth just a couple of years ago. All of this is being delivered while the company maintains earnings before interest, taxes, depreciation, and amortization (EBITDA) margins around 40%.

What Is the DOCN Stock Price Target?

I think DigitalOcean has built one of the more defensible positions in AI infrastructure for customers that are not yet large enough to be hyperscaler clients but are far too sophisticated for generic cloud commodity providers. That gap in the market is real, it is large, and DigitalOcean is filling it.

www.barchart.com

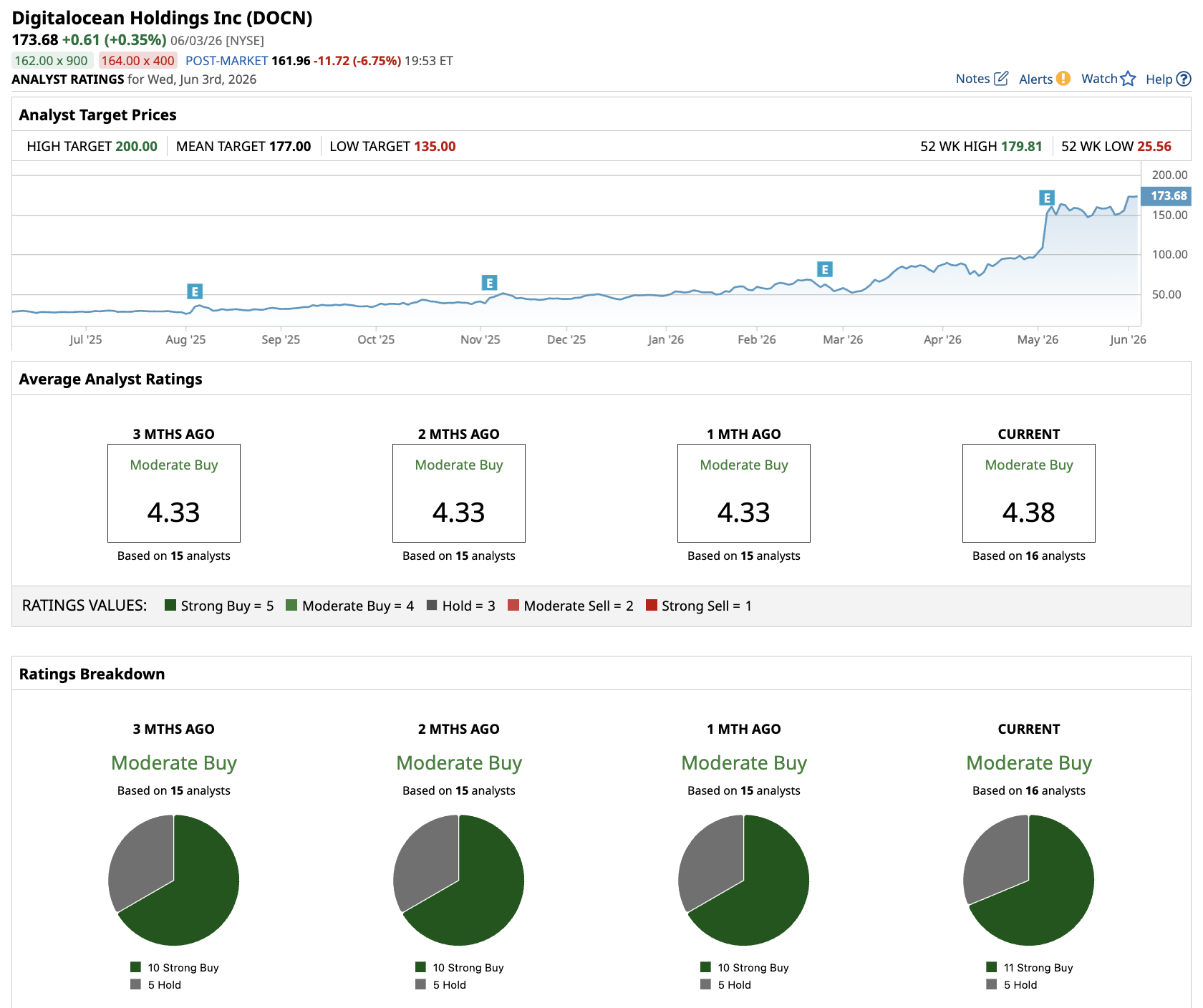

www.barchart.comOut of the 16 analysts covering DOCN stock, 11 recommend “Strong Buy” and five recommend “Hold.” The average DigitalOcean stock price target is $178, slightly the current price of $182.

If you are looking for a stock with a clear growth runway, improving fundamentals, and a management team that is executing ahead of schedule, DOCN deserves a serious look.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Analysts Are Betting Big on DigitalOcean Stock for the Next Era of AI Costco Slips on Plans to Refund Tariff Returns to Customers. The Negative Reaction May Be Deserved. 3 Reasons Why Unusual Options Activity in Progressive Stock May Point to a Bottom IBM Stock’s $10 Billion Quantum Catalyst Is Here