ICON plc ICLR is moving through a credibility and earnings reset that is now as much about controls as it is about demand. The company has laid out the scope of its accounting findings, flagged material weaknesses, and set expectations for a down year in 2026.

With profitability showing heightened sensitivity to mix and estimates, investors are likely to focus on execution and consistency. ICON currently carries a Zacks Rank #5 (Strong Sell).

ICLR’s Investigation Findings and Restatement Scope

ICON’s Audit Committee review concluded that improper adjustments were made to clinical trial services revenue from third-quarter 2023 through fourth-quarter 2024. The issue primarily impacted the timing of revenue recognition, rather than the underlying business activity.

The company disclosed the findings resulted in an overstatement of full-year revenue of $65 million in 2023 and $93 million in 2024. Beyond the revenue timing, the review also cited errors tied to cost-to-complete estimates, realizable value assessments, and certain manual adjustments that extended into 2025.

In the past year, ICLR shares have surged 9.9% against the industry’s 3.2% decline.

Image Source: Zacks Investment Research

For investors, the timing element matters because it goes to the reliability of reported trend lines. When revenue is shifted across periods, it can distort growth comparisons, backlog conversion assumptions, and margin expectations that are built from quarterly patterns.

ICON’s Control Weaknesses and Remediation Timeline Risk

Alongside the investigation findings, ICON identified material weaknesses in internal controls over financial reporting. The company cited gaps in both entity-level controls and controls over revenues and related accounts, which raises the bar for proving that the process is now repeatable and durable.

Management is implementing a remediation plan that includes organizational changes, revised policies and procedures, additional training, and tighter controls over manual adjustments. The direction is clear: reduce discretion, improve oversight, and standardize how revenue-related judgments are made and reviewed.

The confidence overhang is the timeline. Management has signaled that fully embedding remediation across 2026 remains a key risk for investor confidence, which can keep valuation and sentiment capped even if operating metrics begin to stabilize.

ICLR’s Q4 Profitability Drop Shows Estimate Sensitivity

Fourth-quarter 2025 results highlighted how quickly profitability can swing when mix and estimates move together. Adjusted earnings per share fell to $2.52 from $3.86 in the prior-year quarter, while adjusted EBITDA margin declined to 15.5%.

Two drivers stood out. First, pass-through revenue exceeded expectations by more than $150 million, pressuring margin because these revenues typically carry lower profitability than direct fees. Second, a comprehensive review of the full-service portfolio drove cost-to-complete and realizable value adjustments that management said reduced quarterly earnings by more than $50 million.

The takeaway is that the model’s near-term earnings power is highly sensitive to project mix and estimation discipline. Until that volatility fades, quarter-to-quarter results may be harder for investors to underwrite with confidence.

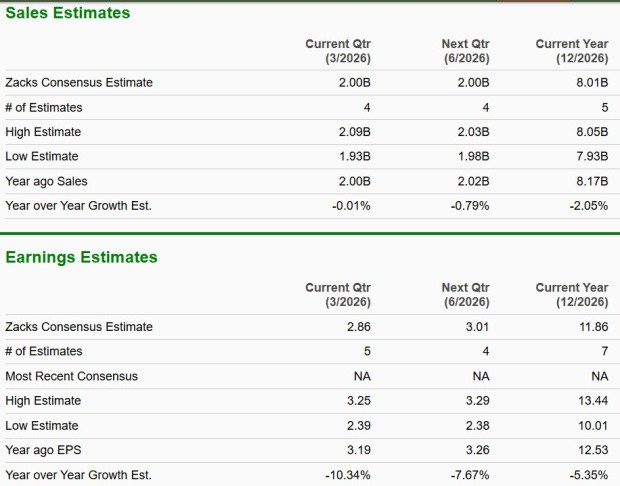

The Zacks Consensus Estimate for ICLR’s 2026 sales and EPS implies a year-over-year decrease of 2% and 5.3%, respectively. The bottom-line estimates have moved south in the past 30 days.

Image Source: Zacks Investment Research

ICON’s 2026 Guide Frames a Down Year and Reset

ICON’s guidance frames 2026 as a reset year. Management guided to revenue of $7.85-$8.15 billion and adjusted earnings per share of $10.00-$11.00, compared with full-year 2025 adjusted earnings per share of $12.53.

Management tied the outlook to weaker bookings that persisted from 2024 into the first three quarters of 2025 and to elevated cancellations in recent quarters, which are expected to weigh on conversion in 2026. The company also indicated that part of the projected revenue decline reflects the Symphony Health divestiture, with the rest tied to organic weakness.

Mix and pricing are also key. With pass-through revenue expected to remain broadly in line with 2025 levels, the guidance implies a steeper decline in direct fee revenue. That dynamic can constrain margins, particularly given earlier pricing limitations that management cited as part of the setup.

For context, investors often compare ICON with other large clinical research and services players such as IQVIA Holdings IQV and Thermo Fisher Scientific TMO. If sector peers show steadier conversion or cleaner margin trajectories, ICON’s reset period may look more demanding by comparison.

ICON’s What to Watch Into 2026 and Early 2027

Management expects first-quarter 2026 results to start near the weaker fourth-quarter run rate. That sets a low starting point and increases the importance of sequential execution as the year progresses.

ICON expects margin improvement through 2026, but sensitivity remains elevated. Investors should watch project mix, pass-through revenue timing, and whether operational efficiency initiatives translate into measurable margin progression.

The other key marker is whether remediation efforts become fully embedded across 2026. A cleaner control environment, paired with steadier conversion, would likely be the foundation for rebuilding confidence into early 2027.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Thermo Fisher Scientific Inc. (TMO): Free Stock Analysis Report

ICON PLC (ICLR): Free Stock Analysis Report

IQVIA Holdings Inc. (IQV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).