Broadcom (AVGO) has been one of the undisputed champions of the artificial intelligence (AI) boom. As a leading designer of custom AI chips for hyperscale cloud giants, the company has become a cornerstone of the rapidly expanding AI infrastructure market, helping drive its stock nearly 380% higher over the past three years. Yet, despite delivering another standout quarter recently, investors hit the sell button. Following its fiscal second-quarter earnings report on June 3, Broadcom shares sank 12.6% in the next trading session and extended those losses with another 8% decline a day later.

The market's reaction is puzzling. Broadcom not only beat Wall Street's expectations on both revenue and earnings, but it also reported surging AI semiconductor demand and projected AI chip revenue to grow further by more than 200% in the third quarter of fiscal 2026. In almost any other industry, that kind of outlook would have sent shares soaring. Instead, the headline appears to have been drowned out by impossibly high expectations surrounding AI chipmakers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Even so, in a market obsessed with perfection, Broadcom's stunning growth forecast may have been overshadowed by sky-high expectations. But for long-term investors, that overlooked 200% growth projection could ultimately prove to be the real story. Thus, let’s take a closer look at Broadcom stock.

About Broadcom Stock

Headquartered in San Jose, Broadcom has emerged as one of the most important companies underpinning the modern digital economy. While it lacks the consumer visibility of many Big Tech names, the company plays a critical behind-the-scenes role, supplying the chips and infrastructure software that power data centers, broadband networks, enterprise systems, and cloud platforms. Its business spans a broad semiconductor portfolio centered on connectivity and data processing, alongside a growing infrastructure software division built through a series of strategic acquisitions.

That unique combination has positioned Broadcom at the center of several of technology's most powerful secular trends, most notably artificial intelligence and cloud computing. In 2026, the company's growth has been fueled by surging demand for custom AI accelerators and the high-speed networking hardware required to link together the massive GPU clusters driving advanced AI workloads. Unsurprisingly, that pivotal role in the AI ecosystem has kept Broadcom firmly on investors' radar.

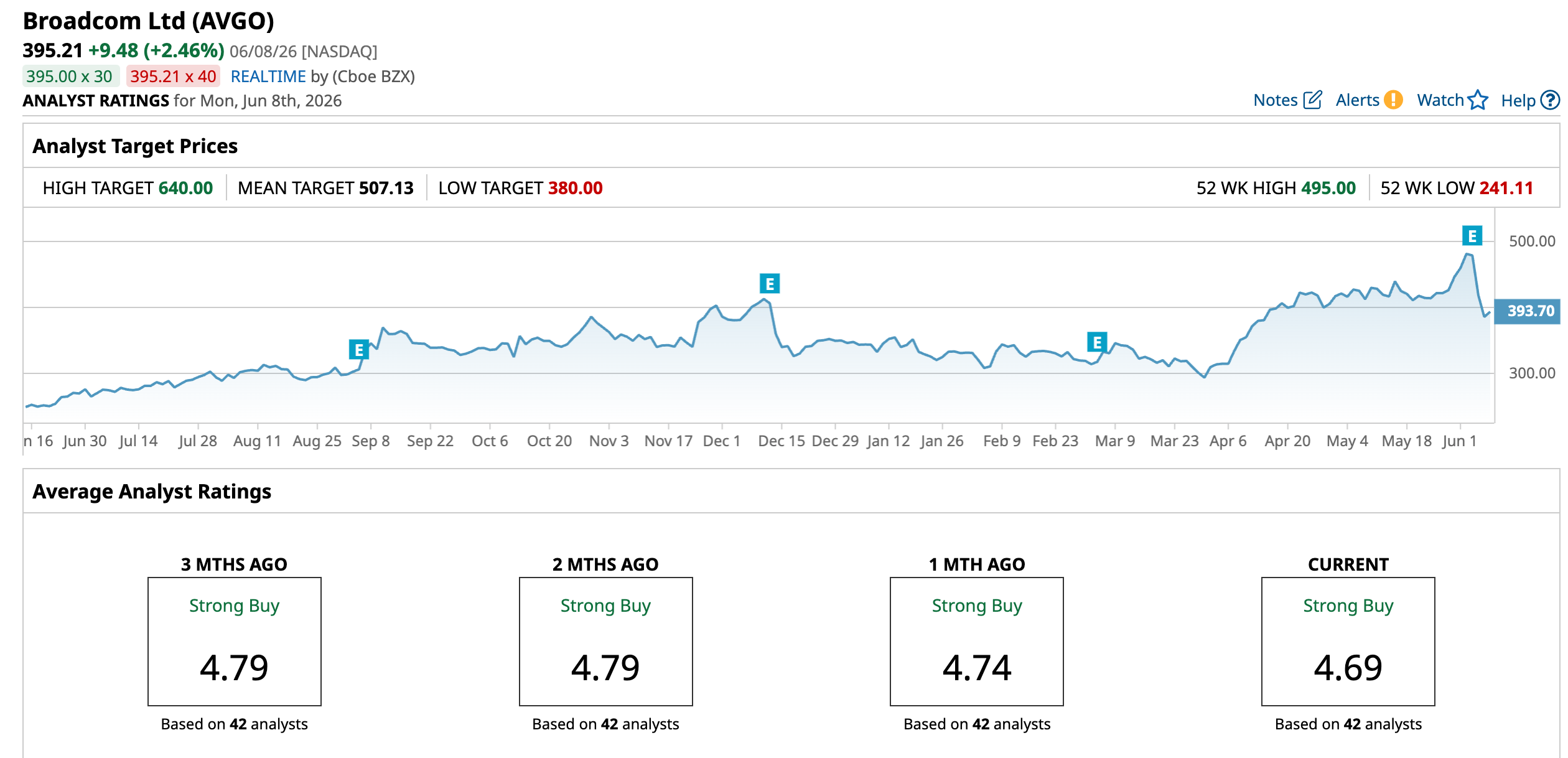

However, after delivering a staggering triple-digit rally over the past three years, Broadcom's stock is beginning to show signs of the lofty expectations now embedded in its valuation. The semiconductor giant, which currently boasts a market capitalization of roughly $1.83 trillion, climbed to an all-time high of $495 on June 3 as investors eagerly awaited its latest quarterly earnings report. But despite posting another strong set of results, the market's reaction was swift and unforgiving.

Shares tumbled in the days following the release and are now down 24.7% from that record peak. But even with the recent pullback, Broadcom's longer-term performance remains impressive. The stock has gained 60.42% over the past year, comfortably outperforming the broader S&P 500 Index ($SPX), which returned 23.95% over the same period. The trend has continued into 2026, with Broadcom advancing 14.46% year to date (YTD), ahead of the broader market’s 8.65% gain.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Inside Broadcom’s Q2 Earnings Report

Broadcom delivered what would ordinarily be considered a blockbuster fiscal 2026 second-quarter earnings report on June 3, further cementing its role as one of the key companies powering the global AI infrastructure buildout. Fueled by relentless demand for its custom AI application-specific integrated circuits (ASICs) and high-performance networking solutions, the technology giant generated record net revenue of $22.19 billion, up 48% from the $15 billion reported a year earlier and comfortably ahead of Wall Street's $22.04 billion consensus estimate.

The standout performer was once again Broadcom's AI semiconductor business. AI-related semiconductor revenue reached a record $10.8 billion during the quarter, surging 143% year-over-year (YOY) and modestly exceeding management's own projections. The rapid expansion underscores the quick pace at which hyperscalers are deploying custom silicon, with AI products now accounting for nearly half, roughly 49%, of Broadcom's total consolidated revenue.

Profitability was equally impressive. Non-GAAP earnings came in at $2.44 per share, an increase of 54% from the prior year and ahead of analyst expectations of $2.40. The company also converted that growth into substantial cash generation, reporting record adjusted EBITDA of $15.24 billion, up 52% YOY and representing an exceptional 69% of total revenue. Meanwhile, free cash flow climbed 60% YOY to $10.26 billion, highlighting the strength of Broadcom's operating model.

Looking ahead, management painted an even stronger picture. Broadcom expects fiscal third-quarter 2026 revenue to reach approximately $29.4 billion, implying an 84% YOY increase. More notably, the company forecast AI semiconductor revenue of $16 billion for the quarter. If realized, that would represent an extraordinary annual growth rate of more than 200% compared with the $5.2 billion generated in the third quarter of the prior fiscal year, reinforcing the view that demand for custom AI silicon continues to accelerate at a remarkable pace.

Yet, despite these eye-catching numbers, the market's response was surprisingly negative, with the stock suffering a double-digit decline in the following trading session. Much of the disappointment appeared to stem from management's decision to reaffirm, rather than raise, its longer-term outlook, a sign of just how elevated investor expectations have become for AI chipmakers.

At the same time, some investors focused on subtle shifts within the business mix. Broadcom's Infrastructure Software segment, anchored by the VMware acquisition, generated $7.18 billion in revenue, a solid 9% increase from a year ago. However, that growth looked modest when compared with the blistering 79% YOY expansion recorded by the company's Semiconductor Solutions segment, adding to concerns that not every part of the business is keeping pace with its rapidly growing AI franchise.

How Are Analysts Viewing Broadcom Stock?

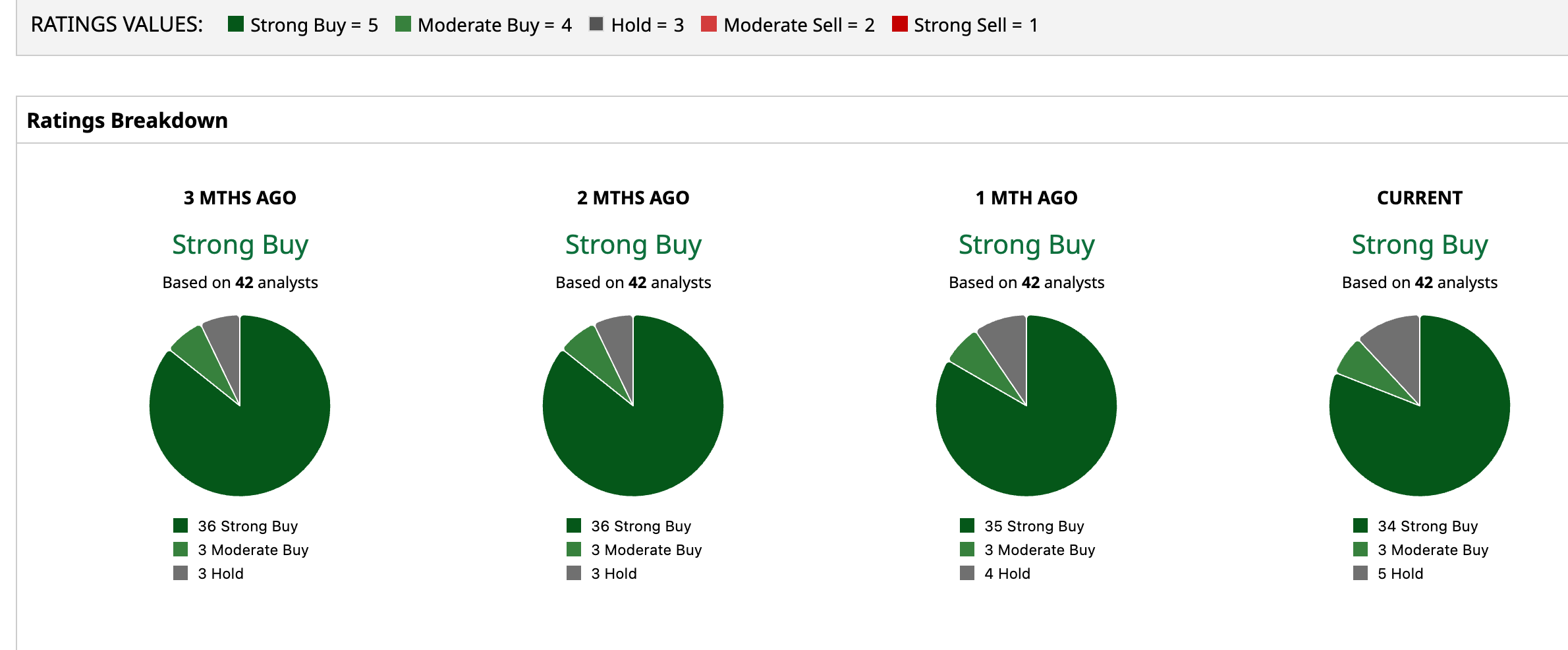

Despite the recent post-earnings selloff, Wall Street's confidence in Broadcom remains firmly intact. The stock currently carries a consensus "Strong Buy" rating, with 34 of the 42 analysts covering the company recommending a "Strong Buy," three assigning a "Moderate Buy," and just five opting to remain on the sidelines with a "Hold" rating. Analysts also see considerable room for further gains, with the average price target of $507.13 implying upside potential of 28.32% from current levels, while the Street-high target of $640 suggests the shares could rally nearly 61.9%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Suddenly, SpaceX's $1.75 Trillion IPO Seems Like It's Undervalued Dear Oracle Stock Fans, Mark Your Calendars for June 10 Investors Are Punishing Broadcom Stock After Earnings. They’re Missing a 200% Spike in Semiconductor Revenue Ahead. Dear Datadog Stock Fans, Mark Your Calendars for June 9