Logan Nicholson, the president of private credit firm Blue Owl Capital (OBDC), has bought 3,000 shares of his own company to increase his holdings to 88,000. This was Nicholson's second purchase of his company's shares this year, following one in February when he bought 10,000 shares.

This was just before things took a turn for the worse in April 2026, when the company imposed caps on withdrawals for two of its key funds after receiving redemption requests totaling about $5.4 billion.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Blue Owl Capital

Founded in 2016 as Owl Rock Capital Corporation, Blue Owl Capital is one of the largest publicly traded Business Development Companies (BDCs) in the U.S. It provides direct loans to middle-market companies and allows public-market investors to gain exposure to the fast-growing private credit market. It is externally managed by the credit platform of Blue Owl Capital, one of the largest private credit managers globally.

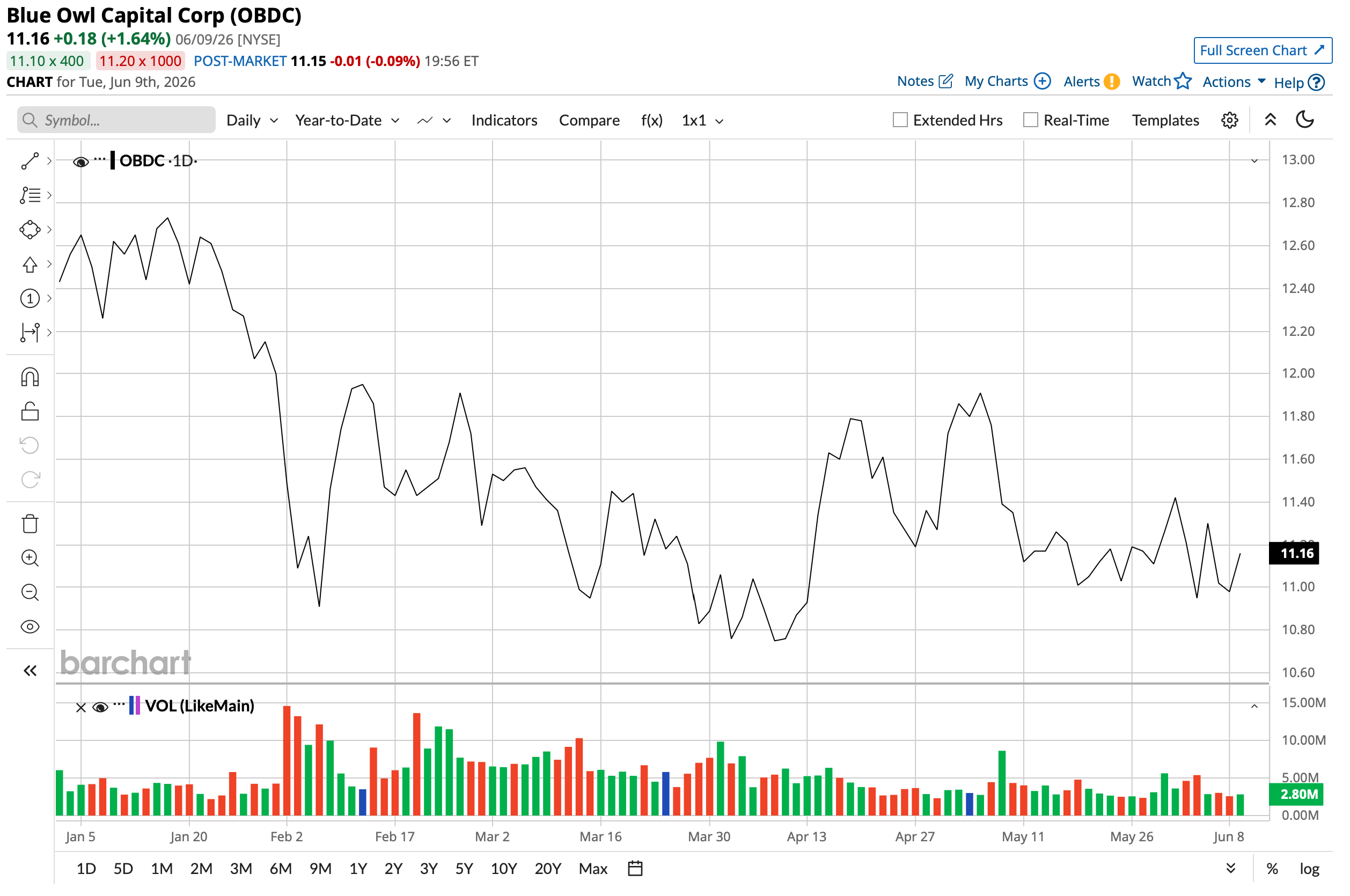

Valued at a market cap of $5.54 billion, OBDC stock is down 10.54% year-to-date (YTD), although the stock has staged a recovery from its April lows. The stock also offers a dividend yield of 13.43%, which is much higher than the sector median of 1.30%.

www.barchart.com

www.barchart.com So, with the OBDC president doing the needful to convey his own confidence about the company's prospects, will shares of Blue Owl finally see green?

Muted Q1 With A Silver Lining

Before diving into the financials of Blue Owl, it must be established that a company like itself is not measured primarily on traditional metrics such as sales and earnings. The evaluation rests on some other relevant metrics.

Beyond that, Blue Owl had a disappointing Q1. Its net asset value per share dwindled to $14.41 from $15.14. Net asset value is the difference between the fair market value of the assets the company has and its liabilities. In addition, total assets declined to $15.3 billion from $17.7 billion in the year-ago period as investment income dropped to $396.8 million from $464.6 million in the same period.

Notably, the company had a cash balance of $455 million. Overall, Q1 ended with the company invested in 230 companies, spanning 30 industries. The total portfolio size was $15.3 billion, and the average investment size was $66.7 million. This was down on almost all fronts from the previous year's figures of 236 companies, 30 industries, a total portfolio size of $17.7 billion, and an average investment size of $75 million.

However, in Q1 2026, Moody's upgraded Blue Owl's credit rating to Baa2, an investment-grade category. Moreover, the stock is trading at a forward price-to-book value of 0.77 times, which is lower than the sector median of 1.24 times.

Steady & Conservative

Blue Owl's prescience must be appreciated. Loan issuance experienced a slowdown during the first quarter. This development stemmed partly from heightened caution among borrowers and somewhat tighter credit standards adopted in response to ongoing geopolitical uncertainties. Notably, management continues to pursue a measured approach to risk-taking that prioritizes the long term stability and health of the organization. As a result, leverage declined to 1.13 times from 1.19 times in the prior quarter.

Further, the credit quality metrics offer perhaps the most straightforward read on portfolio health. As of March 31, 2026, investments on non-accrual represented 2.0% and 1.0% of the portfolio at cost and fair value, respectively, improving from 2.3% and 1.1% at the end of 2025, with no new non-accruals added in Q1. Since inception, the net loss rate across the broader Blue Owl Credit platform has remained below 10 basis points annually, which is a remarkably clean track record across a full credit cycle.

The specialty finance layer adds another dimension to the quality argument. Seven joint venture and specialty finance partnerships spanning asset-based finance, equipment leasing, life sciences, and life settlements collectively generated ROEs of over 14% in the past year, with exposure to more than 300 underlying loans and approximately 10,000 individual asset line items. Those partnerships generate income that is less correlated with base rates than the core loan book, which provides a meaningful buffer when the Federal Reserve is cutting.

Analyst Opinion

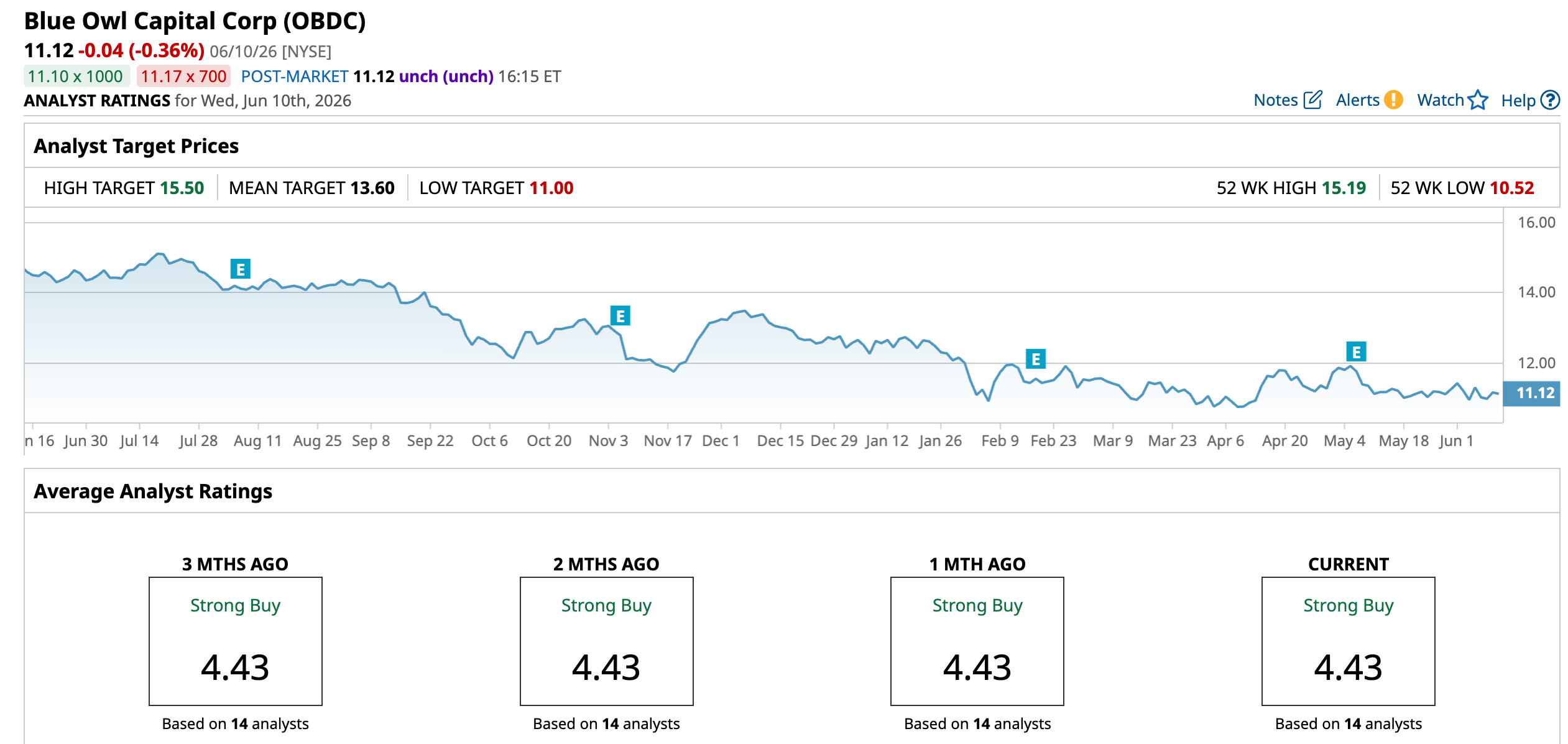

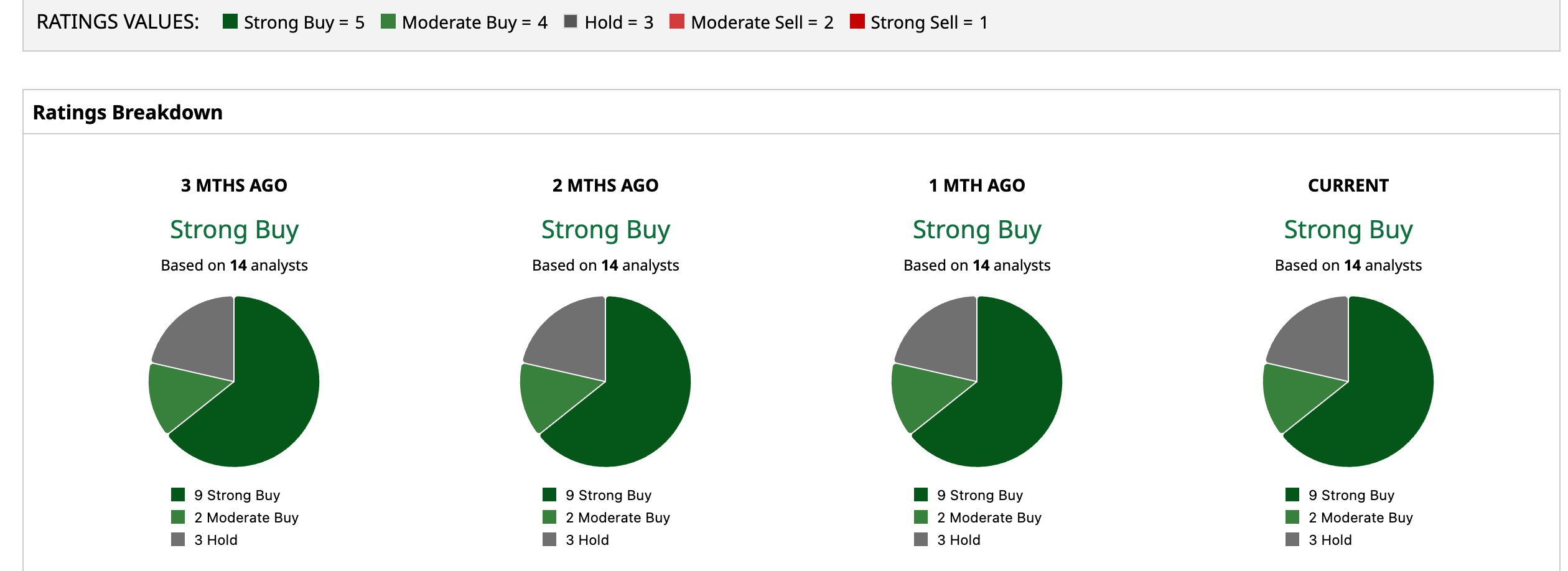

Overall, analysts have deemed OBDC stock to be a “Strong Buy” with a mean target price of $13.60. This indicates an upside potential of 22.3% from current levels. Out of 14 analysts covering the stock, nine have a “Strong Buy” rating, two have a “Moderate Buy” rating, and three have a “Hold” rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Stock Sink After Q2 Earnings Miss. Why 267% Pipeline Growth Wasn’t Enought. Jensen Huang Says AI Is ‘Insanely Profitable.’ That Means It’s Not Too Late to Hop on the Nvidia Bandwagon. Blue Owl Capital President Logan Nicholson Just Bought 3,000 Shares of OBDC Stock Amid Private Credit Scandal Nvidia Chose This AI Cloud Stock Over Everyone Else. Here’s Why.