Memory chip and AI-driven data storage stocks are among the market’s hottest areas right now, and Sandisk (SNDK) has been one of the biggest beneficiaries of the trend. Demand continues to rise as AI adoption accelerates and cloud companies invest heavily in expanding storage capacity.

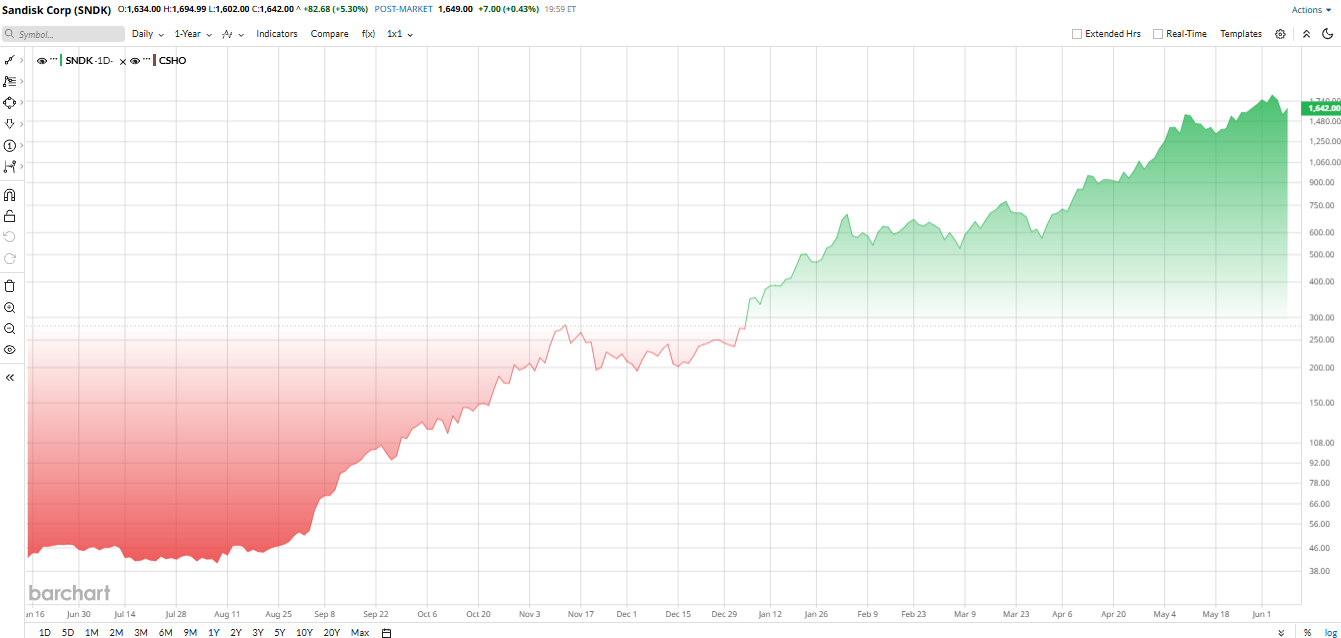

That strong backdrop has helped fuel a massive rally in SNDK stock over the past several months. Shares recently received another boost after Bank of America raised its 12-month price target from $1,550 to $2,100, catching investors' attention. Even after dropping more than 11% on June 5, Sandisk quickly rebounded 5% to $1,642 on June 8 and has continued to climb this week.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The reason is simple. AI keeps pushing memory demand higher, NAND supply remains tight, and investors still see Sandisk as one of the cleanest ways to play the storage shortage.

Sandisk’s New Identity as an AI Storage Play

Sandisk is a pure-play flash memory company now, not just a Western Digital (WDC) unit in disguise. The company sells NAND-based storage for data centers, PCs, edge devices, and consumer electronics. Since the spinoff in 2025, the market has treated Sandisk like a direct bet on AI storage demand and the pricing power that comes with it.

Sandisk has signed multiple multiyear customer agreements and is also preparing high-bandwidth flash products later in 2026. That matters because it gives the company more stability and more leverage if memory prices stay strong. It also shows that Sandisk is trying to turn a hot cycle into a better long-term business model. That is a smart move in a market that can get ugly fast when supply eventually catches up.

The company's stock is also soaring. SDNK stock has surged more than 660% in 2026 and about 4,400% over the past year. That is the sort of move that makes every dip look small — and every upgrade feel important. The latest pop came after Bank of America and Mizuho both turned more bullish, saying the supply-demand backdrop in memory is still working in Sandisk’s favor. Even the recent pullback did not change the bigger trend. AI data centers still need storage, and Sandisk is selling into a market where pricing remains firm.

At first glance, Sandisk looks expensive because the share price is so high. But the earnings multiple tells a different story. SNDK stock trades at 25.7 times forward earnings, while the broader semiconductor sector trades close to 26 times. That is not a bargain-bin valuation, but it is also not crazy for a company growing this fast. The market is basically saying the current cycle is real, but it still wants proof that the earnings power can last.

www.barchart.com

www.barchart.com Sandisk Beats Q3 Earnings Estimates

Sandisk’s latest quarter showed exactly why the bulls are so loud. Revenue hit $5.95 billion in the third quarter, up 251% year-over-year (YOY) and well ahead of estimates. Datacenter revenue came in at $1.47 billion, while Edge came in at $3.66 billion, and Consumer revenue was $820 million.

Net income was $3.62 billion. Adjusted EPS came in at $23.41, a huge sequential jump of 278% from adjusted EPS of $6.20 in Q2 2026. That is not just a beat. That is a full-blown reset in earnings power.

Cash was strong, too. Sandisk generated $2.99 billion in free cash flow and ended the period with more than $3.73 billion in cash and equivalents.

CEO David Goeckeler called the quarter a “fundamental inflection point” and said the company is shifting toward a higher-value data-center business. He also pointed to a “zero-debt balance sheet” and newly authorized buyback program.

For the next quarter, Sandisk guided for revenue of $7.75 billion to $8.25 billion and adjusted EPS of $30 to $33, both ahead of Street expectations. BofA also lifted its fiscal 2027 revenue estimate to $44 billion and EPS estimate to $188.

What Do Analysts Say About SNDK Stock?

Wall Street is becoming increasingly optimistic about Sandisk as demand for AI-related memory products continues to strengthen.

Recently, Bank of America analyst Wamsi Mohan reiterated a “Buy” rating and raised his price target to $2,100, pointing to improving pricing trends and strong demand. Mohan also increased his fiscal 2027 revenue and earnings forecasts, signaling confidence in the company’s growth outlook.

Other analysts have followed suit. Cantor Fitzgerald recently raised its target to $2,900, while Mizuho lifted its target to $2,200. These bullish outlooks reflect expectations that growing AI adoption will continue driving demand for memory products.

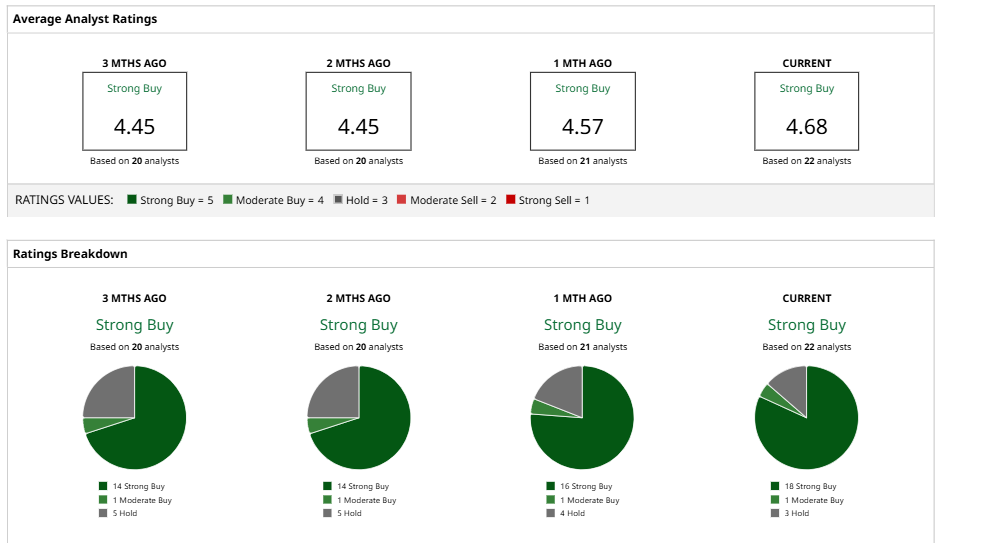

Overall, analysts remain largely positive on Sandisk. Most see the company benefiting from strong demand from AI and data-center customers, as well as a favorable supply-and-demand environment in the memory market.

Based on 22 analysts with coverage, Sandisk has a consensus “Strong Buy” rating. The average price target of $1,863.06 suggests that Wall Street still sees potential upside of 2% from current levels, although expectations have already risen significantly following SNDK stock’s strong rally.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How to Play PBLS Stock After the Parabilis IPO Sandisk Stock Has More Room to Run Even After 660% Rally, According to Bank of America This Analyst Just Upgraded Devon Energy Stock. Here's Why. Why 1 Veteran Analyst Firm Hiked Its Qualcomm Stock Price Target for 2026