Microsoft (MSFT) has long been viewed as one of the market’s steadier mega-cap growth names, thanks to its reach across software, cloud computing, and enterprise technology. But even a company as dominant as Microsoft is not immune to the pressure of shifting geopolitics, changing regulations, and the need to constantly fine-tune where it deploys capital and people.

That tension is now coming into focus in China, where Microsoft is reportedly cutting hundreds of jobs from its Azure cloud unit. The move comes when data and regulatory issues become more complicated between Washington and Beijing, even as Azure continues to post strong growth and Microsoft keeps expanding its global cloud footprint.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors trying to separate the noise from the real story, here’s what the latest China layoffs may actually say about MSFT's bull case.

www.barchart.com

www.barchart.com Microsoft Has Slumped in 2026. Is the Valuation Finally Attractive?

Over the past year, Microsoft shares fell about 19%, badly lagging the sector’s 19% gain. Year-to-date (YTD) in 2026, the stock is down around 20% as AI spending fears linger. It trades below its 50-day and 200-day moving averages. Capex worries, margin uncertainty, and rotation away from mega-cap tech have kept buyers cautious.

Microsoft trades at a price-to-sales ratio of 10, more than double the sector median of 4. That’s expensive on a sales basis. But its P/E of 25 is slightly below the sector’s 26, hinting at relative earnings value. The valuation picture is mixed, hardly a steal, but not wildly expensive either.

What Layoffs Mean for Investors

So, Microsoft is reportedly laying off hundreds of employees in its China-based Azure unit, according to the South China Morning Post. The move aims to streamline cloud operations and redirect focus to higher-growth AI services outside China. Investors took it in stride; the stock moved little. The cuts highlight a leaner approach amid geopolitical tensions and a maturing China cloud market.

For investors, shedding non-core roles could protect operating margins. Yet it also signals that Azure’s expansion in the region may slow. The long game is about pouring resources where AI demand is hottest.

The AI Growth Engine Keeps Humming

Microsoft’s fiscal third quarter was a reminder that AI tailwinds are real. Revenue climbed 18% to $82.9 billion. Intelligent Cloud, the segment housing Azure, jumped 30% to $34.7 billion, with Azure and other cloud services up 40% on AI workloads. Productivity and Business Processes added $35.0 billion, up 17%, while More Personal Computing delivered $13.2 billion, down 1%.

Net income surged 23% to $31.8 billion, and diluted earnings per share hit $4.27, also up 23%. Microsoft Cloud revenue came in at $54.5 billion, and the company said its AI annual revenue run rate reached $37 billion, up 123% from a year earlier.

Free cash flow came in at about $15.8 billion, based on $46.7 billion in operating cash flow and $30.9 billion in additions to property and equipment, while cash and cash equivalents stood at $32.1 billion.

CEO Satya Nadella said Microsoft’s AI business surpassed a $37 billion annual revenue run rate, up 123% from a year earlier, while margins were pressured by continued investment in AI infrastructure.

Looking ahead, for the current quarter, Microsoft said Azure and other cloud services revenue is expected to grow 39% to 40% in constant currency, while revenue is seen at $86.7 billion to $87.8 billion.

Betting $190 Billion on the Future

Beyond layoffs, Microsoft launched AI-powered Surface PCs with neural engines in spring 2026, expanded its OpenAI enterprise partnership, and released seven custom AI models. Project Solara, a cloud sustainability tool, also debuted. The company’s AI annual recurring revenue hit $37 billion, up 123%. All this is backed by a $190 billion capital expenditure plan for 2026, mostly for data centers and AI infrastructure.

These moves confirm Microsoft’s AI-dominant position, yet the enormous spending keeps investors asking when the payoff will truly arrive.

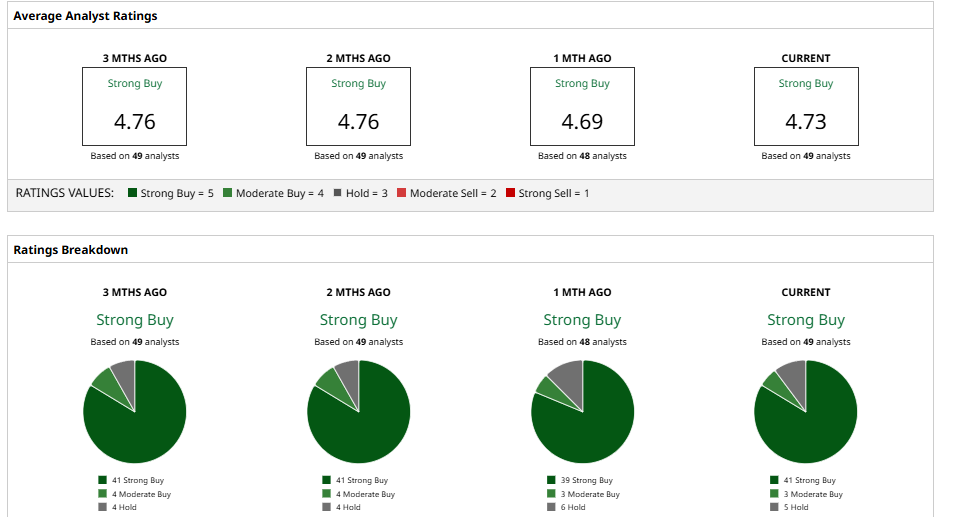

The Street’s Verdict on MSFT Stock

Wall Street is mostly liking the Microsoft growth story. Morgan Stanley reiterated an “Overweight” rating and a $650 price target, saying the software spending backdrop remains supportive and Microsoft stands to benefit from broader Azure adoption and AI demand.

Similarly, Piper Sandler recently kept an “Overweight” call but trimmed its target to $540, while Guggenheim held a “Buy” rating with a $586 target ahead of earnings. Goldman Sachs also has a “Buy” rating and a $655 target.

Bank of America upped its target to $500, citing faster-than-expected AI monetization.

Taken all together, according to Barchart, the consensus rating is “Strong Buy.” The average 12-month price target is $554.28, implying roughly 40% upside from recent levels. Notably, MSFT stock currently has zero sell ratings.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Microsoft Is Cutting Hundreds of Azure Jobs in China. The Hidden Story No One Is Telling. How to Play Einride Stock After the Autonomous Trucking Company’s IPO Unusual Options Activity Points to Bullish Bets on MSFT, CSX, and SCHW GM Stock Alert: What to Know as General Motors Announces Energy Storage Pivot