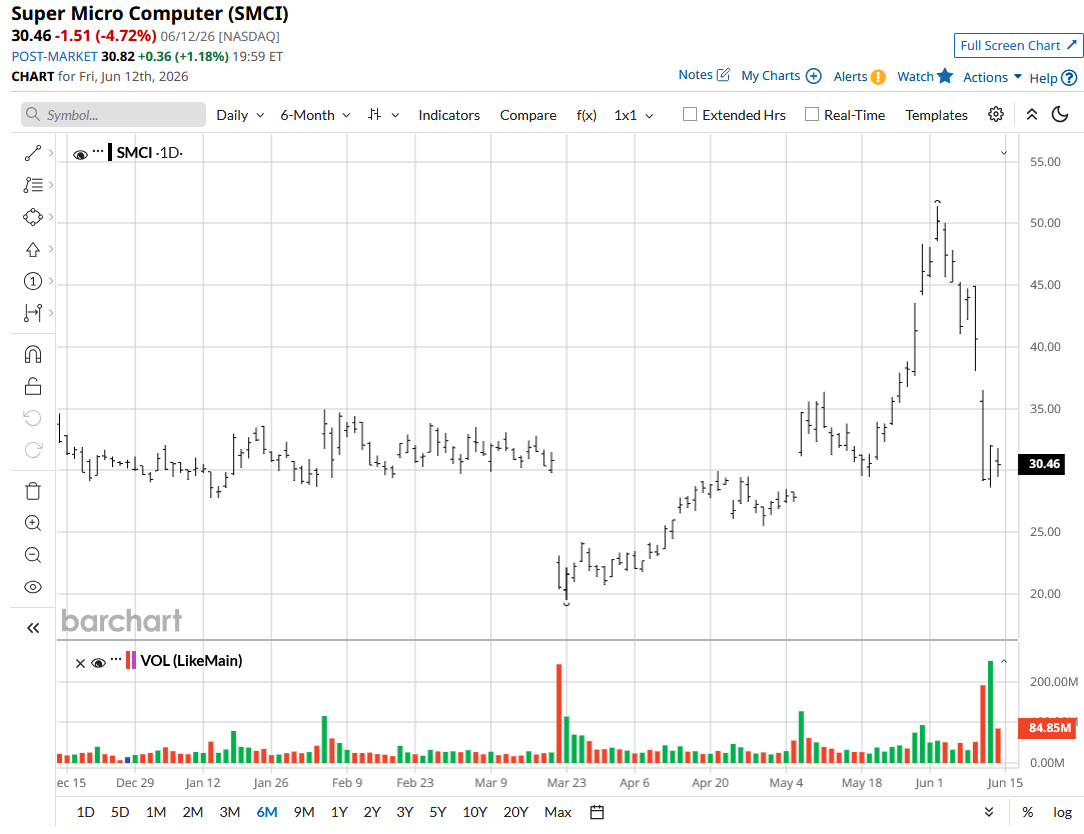

Supermicro (SMCI) recently announced plans to raise $7 billion through an equity offering to purchase components needed to fulfill AI server orders worth $39 billion. Where otherwise a backlog would be considered positive for a company, raising money through equity issuance to fulfill that order has spooked investors. Accordingly, concerns about dilution have caused SMCI stock to fall 28% over the past five days.

This isn’t the company’s first experience with severe volatility. In 2024, after Supermicro was nearly delisted from the Nasdaq Exchange due to its auditor resigning over accounting irregularities, the stock dropped by 70%. Since then, sudden and large moves have become common with SMCI shares.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The $39 billion worth of orders in question is primarily due to rising demand for AI infrastructure. As one of Nvidia’s (NVDA) major server assembly partners, the surge in demand for Nvidia chips has had a direct impact on Supermicro’s growth. To put this backlog into perspective, the company’s revenue for its most recent fiscal year was $22 billion, so the orders will be challenging to fulfill. However, with guided revenue between $38.9 billion and $40.4 billion for fiscal 2026 and Supermicro set to deliver Vera Rubin-powered servers, the firm might not be in as worrisome a position as the recent drop suggests.

About Supermicro Stock

Supermicro is involved in building infrastructure that is crucial for today’s artificial intelligence and high-performance computing workloads. The company designs and manufactures data centers, enterprise IT systems, and edge computing products used in telecom, 5G, and IoT. Supermicro is based in San Jose, California.

A 52-week high of more than $62 and a 52-week low of $19.48 suggest that investors have had a rough ride over the last 12 months. Underperformance at a time when other AI infrastructure stocks are skyrocketing comes as a huge disappointment, as questions about management quality and financial strength continue to bother shareholders.

www.barchart.com

www.barchart.com Valuation isn’t investors’ immediate concern when it comes to SMCI stock. At face, the forward price-to-earnings (P/E) ratio of 14.4 times and price-to-sales (P/S) multiple of 0.8 times offer immense value. However, there’s a good reason for this massive discount — and it has everything to do with the equity offering.

Supermicro already has $9.1 billion in debt against just $1.31 billion in cash. The fact that the firm is raising more money is a serious red flag for investors, especially in the context of its recent corporate governance issues. While management downplayed such issues on the earnings call, these concerns continue to weigh on the stock price.

Supermicro Delivers Better Than Expected Guidance

Supermicro reported third-quarter fiscal 2026 earnings on May 5. Revenue of $10.2 billion marked a significant jump from $4.6 billion in the same quarter last year but still came in 17% below the analyst consensus estimate. Still, the company did beat the EPS estimate of $0.63, reporting $0.84 compared to just $0.31 in Q3 2025. Along with these two metrics, Supermicro also reported year-over-year (YOY) growth in gross margin and operating income. CEO Charles Liang said that revenue missing the estimate wasn’t due to a lack of demand but rather delays in customer sites being able to receive orders. Liang believes this is a short-term issue, with revenue to be recognized in the coming quarters.

For Q4, Supermicro guided revenue between $11 billion and $12.5 billion, along with non-GAAP EPS of $0.65 to $0.79. The analyst consensus estimate for the quarter is $11.07 billion in revenue and EPS of $0.55. Liang expects at least 20% of net income to come from Data Center Building Block Solutions (DCBPS) in two years. When asked whether the ongoing investigation into the company allegedly violating export controls would affect Supermicro's Nvidia supply, Liang said the company's partnerships remain strong. “Our understanding is that there has been no change in allocation,” said CFO David Weigand.

What Do Analysts Say About SMCI Stock?

In May, Goldman Sachs analyst Katherine Murphy maintained a “Sell” rating on SMCI stock with a price target of $30. Murphy believes the company is heavily reliant on a small number of customers, with just one client accounting for 27% of quarterly sales. The analyst also noted that total revenue from higher-margin services and software was just 1%, making Supermicro reliant on hardware sales. Meanwhile, Mizuho analyst Vijay Rakesh recently increased his target from $36 to $44 while keeping a “Neutral” rating.

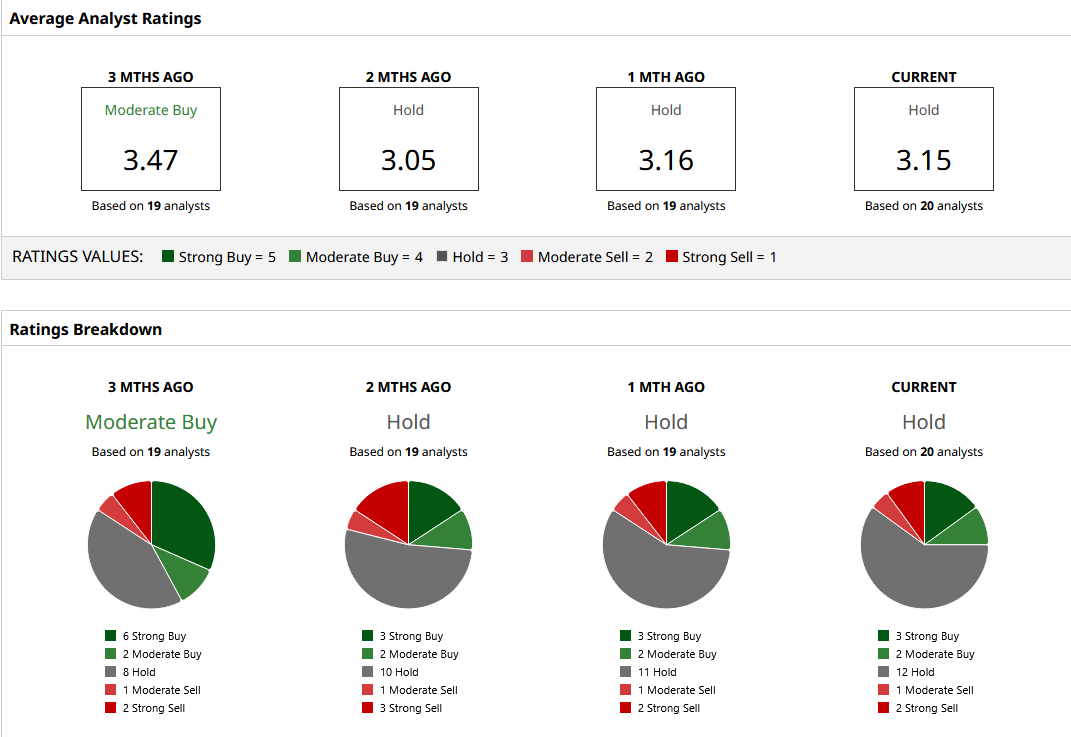

Based on 20 analysts with coverage, SMCI stock has a consensus “Hold” rating. The mean price target of $35.87 indicates potential upside of 23% from current levels. The price targets for SMCI stock range from a high of $50 to a low of $15, reflecting divided Wall Street sentiment.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Salesforce Acquires AI Agent Firm Fin for $3.6 Billion to Expand Agentforce. CRM Stock Could Double Over the Next 4 Years. What to Know as Mobileye Stock Announces Robotaxi Expansion Plans Nvidia Books Massive $85 Billion in Orders for Jumbo Bond Sale. What That Means for NVDA Stock. SpaceX Just Had the Biggest IPO Ever. Here’s How to Get Paid From the Frenzy.