Honeywell (HON) shares pushed meaningfully higher on June 15 after the company’s board of directors formally approved the spinoff of Honeywell Aerospace.

HON closed at $227.41 on Monday, representing significant positive momentum as investors responded enthusiastically to this final milestone in the firm’s multi-year portfolio transformation. In the following days, HON stock has continued the positive momentum, hitting a session high of $234.70 today.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The approval sets the stage for a distribution date of June 29, when HON will distribute Honeywell Aerospace common stock to shareholders of record on June 15.

Including today’s gains, HON stock is up roughly 20% versus the start of this year.

www.barchart.com

www.barchart.comInvestors Are Bullish on Honeywell’s Spinoff

The mechanics of the separation involve shareholders receiving one share of Honeywell Aerospace for every two shares of HON held.

Honeywell Aerospace will commence trading under the ticker HONA on June 29.

The remaining automation-focused business will operate as Honeywell Technologies and continue trading under the ticker HON, with a 1-for-2 reverse stock split immediately following the separation.

The market’s positive reaction reflects investor belief that the spinoff will unlock value by creating two more transparent, investable entities, each with distinct risk profiles, capital requirements, and industry cycles.

The strategic logic is rather compelling: conglomerate discounts have long weighed on diversified industrials, and pure-play companies typically command higher multiples from investors who can more easily benchmark performance against direct peers.

What Management Expects From Separated Businesses

The spinoff will create two distinct and focused industry leaders.

Honeywell Aerospace will operate as a tier-1 aerospace and defense supplier of mission-critical systems and tech, positioned to benefit from resurgent commercial air travel growth and increasing global defense spending driven by geopolitical tensions.

Management has outlined compound annual sales growth targets of at least 6% through the end of this decade, with earnings growth exceeding sales growth and cash flow exceeding earnings growth.

Honeywell Technologies, the remaining business, will concentrate on leading the industrial world's transition from automation to autonomy, encompassing process automation, building automation, and industrial automation.

HON benefits from tailwinds, including energy security investments, decarbonization requirements, regulatory-driven smart building adoption, and manufacturing reshoring trends.

Management has set three-year targets of at least 4% organic growth, more than 60 basis points of annual margin expansion, and over 10% annual earnings growth, accompanied by greater than 90% free cash flow conversion.

Honeywell Remains on the Lookout for Acquisitions

The spinoff represents the culmination of a significant portfolio transformation executed over the past three years under Chairman and CEO Vimal Kapur.

This included the recent IPO of Honeywell’s quantum computing business — Quantinuum (QNT).

The SEC declared Honeywell Aerospace’s Form 10 registration statement effective on June 11, removing one of the final regulatory hurdles.

The company has also signaled appetite for bolt-on acquisitions in the $2 billion to $4 billion range, particularly targeting its industrial automation division, which operates in an addressable market worth about $35 billion.

How Wall Street Recommends Playing Honeywell

From a valuation perspective, HON’s rally pushed it to a level considered modestly overvalued by some quantitative metrics, with a trailing P/E of 32.2x compared to a five-year median of 23.9x.

However, the forward P/E of 21x suggests that earnings growth expectations embedded in the spin-off thesis are compressing the multiple on a forward basis.

Execution risk remains the key concern, including the possibility of stranded costs and operational disruption during the transition period.

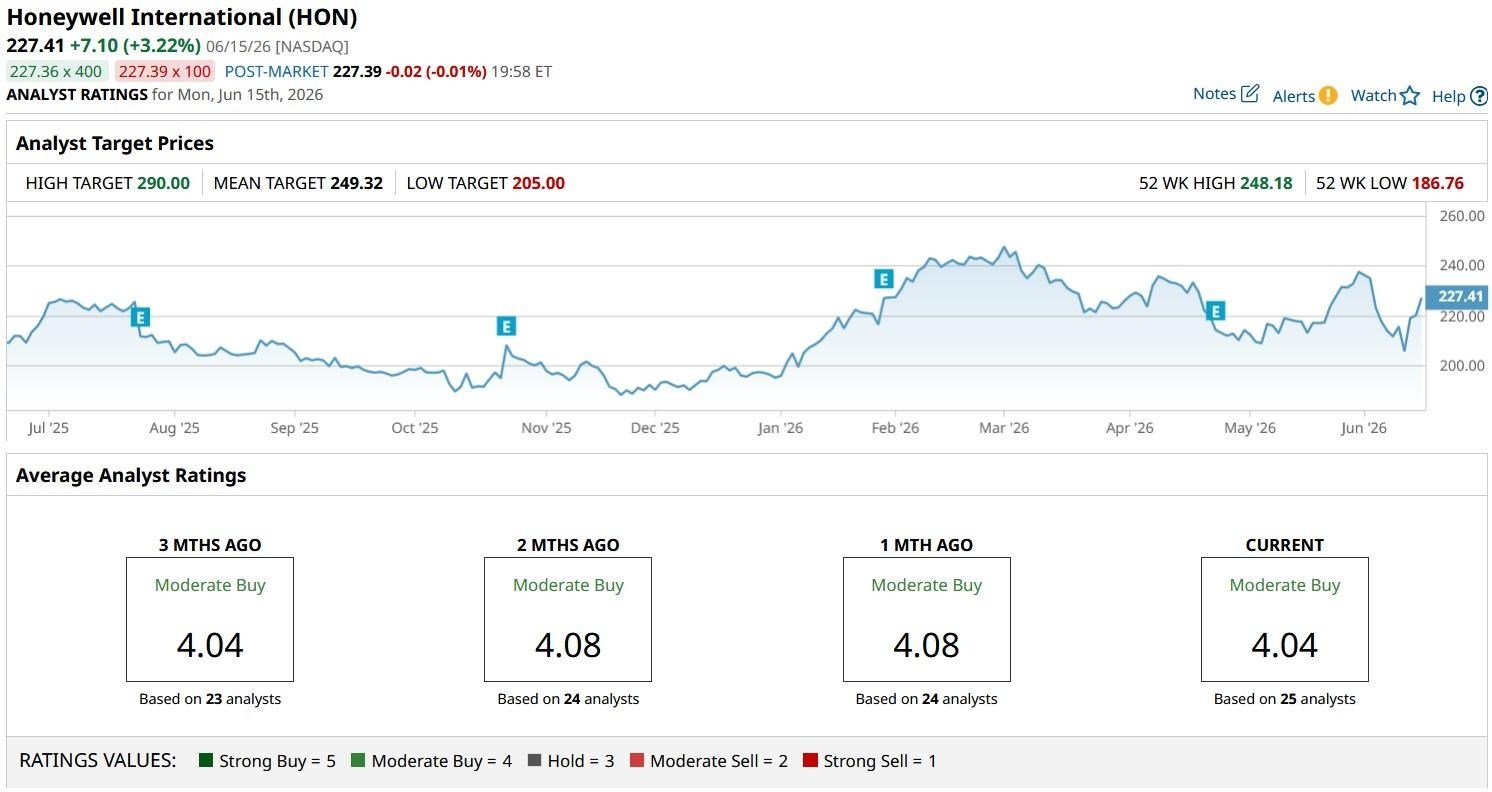

But the Street’s consensus “Moderate Buy” rating on Honeywell suggests analysts view the long-term value creation potential as outweighing near-term separation challenges.

The mean price objective on HON currently sits at about $250, indicating potential for a 10% rally from here.

www.barchart.com

www.barchart.comThis article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

HON Stock In Focus as Honeywell's Aerospace Spinoff Receives Final Approval Citi Upgrades AMD Stock to ‘Buy’ on Massive Meta GPU Sales Potential ‘At Some Point, People Stop Trusting’: Billionaire Mark Cuban Says OpenAI CEO Sam Altman Is ‘All Over The Map’ And Warns ‘That Will Backfire on Him’ Dear Nebius Stock Fans, Mark Your Calendars for June 22