As investors continue hunting for the next breakout story in artificial intelligence (AI) infrastructure, attention has started converging on a less flashy but increasingly critical segment of the market, data center networking, where Marvell Technology (MRVL) has emerged as a key name in focus.

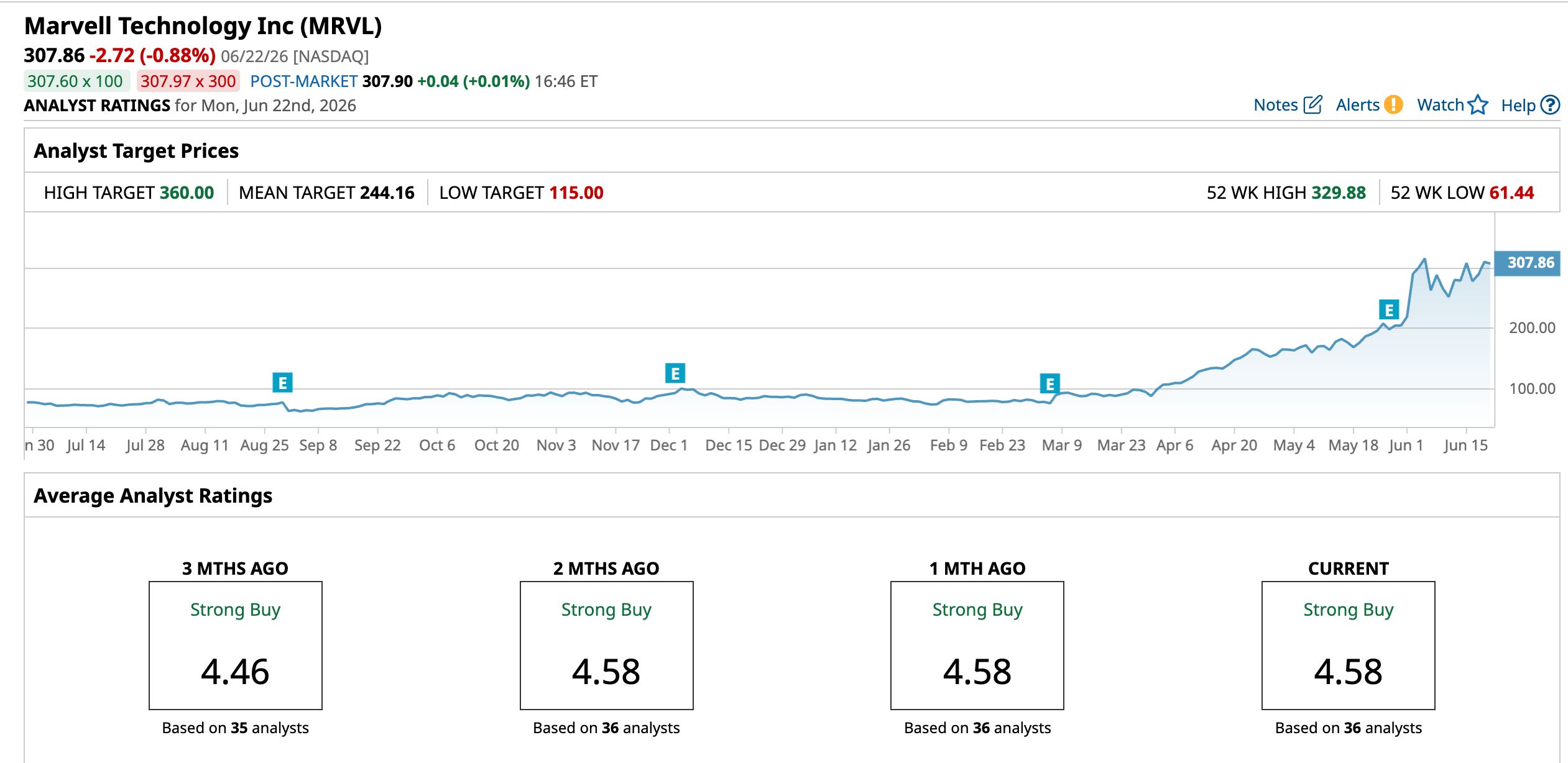

KeyBanc sharpened that narrative by raising its price target on Marvell to $385 from $260 on Thursday, June 18. This helped push the stock up 7.27% in intraday trading as the market priced in the upgraded outlook. In fact, the stock made its new 52-week high of $329.88 that day.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Analyst John Vinh maintained an “Overweight” rating and made a clear distinction between themes inside the AI buildout, arguing that data center networking offers a more durable and visible growth runway compared to custom XPUs even as the company maintains visibility toward $10 billion in revenue by FY2029.

He pointed to structural shifts across global data centers where rising bandwidth demand and AI workloads have steadily elevated networking into a central role rather than a supporting function, positioning it as the strongest growth engine over the coming years.

That conviction underpins KeyBanc’s broader forecast, which projects more than $20 billion in Marvell data center revenue by FY2029. This projection places networking at the center of long-term expectations as investors reassess how much of the AI infrastructure upside the company can realistically capture.

About Marvell Stock

Headquartered in Wilmington, Delaware, Marvell Technology designs semiconductor solutions that power modern data infrastructure. The company develops networking, connectivity, storage, optical, and custom computing chips used across data centers, cloud platforms, telecommunications networks, and enterprise systems.

Commanding a market cap of $271.7 billion, its technologies help move, process, store, and secure data efficiently from centralized servers to the network edge worldwide.

Over the past 52 weeks, the stock has gained 318.8%, extending that momentum into the current year with a 262.3% year-to-date (YTD) increase. The recent trend has remained strong with an 56.8% rise over the past month and an additional 10.1% gain across the last five trading sessions, reflecting sustained investor demand.

www.barchart.com

www.barchart.com On the valuation front, MRVL stock is trading at 76.73 times forward adjusted earnings and 23.58 times sales, positioning it at a premium relative to both industry levels and its five-year historical averages.

The company also returns capital through an annual dividend of $0.24 per share, reflecting a yield of 0.08%. The most recent distribution stood at $0.06 per share on April 30 for shareholders of record as of April 10, providing a modest income component alongside its growth profile.

A Closer Look at Marvell’s Q1 Earnings

On May 27, Marvell reported its Q1 FY2027 earnings results wherein revenue climbed 27.6% year-over-year (YOY) to $2.42 billion, landing in line with analyst estimates of $2.41 billion. Adjusted EPS moved up 29% from the year-ago figure to $0.80 and matched estimates of $0.79.

The real action came from the data center engine. Management leaned on broad multi-product adoption across optical interconnect, custom silicon, and switching, which helped push data center revenue up 27.2% YOY to $1.8 billion and reinforced how deeply AI has embedded itself into the company’s growth story.

Non-GAAP gross profit rose 25.6% from the year-ago period to $1.4 billion while non-GAAP gross margin held firm at 58.9%. Non-GAAP net income also moved higher 33% YOY to $718 million while cash and cash equivalents stood strong at $3.8 billion at quarter-end, giving the balance sheet plenty of breathing room.

Looking ahead, management has signaled a steady climb rather than a one-time spike. They expect sustained double-digit sequential revenue growth supported by accelerating adoption of next-generation interconnect and custom silicon. They have tied the outlook to the strategic partnership with NvidiaCorporation (NVDA) and the ramp of new AI-focused product lines, framing them as key gears in the growth machine.

For Q2 FY2027, management is guiding net revenue to $2.7 billion with a variation of 5% on either side, while non-GAAP diluted net income per share is projected at $0.93 with a possible variation of $0.05.

FY2027 revenue is expected to grow about 40% YOY. The upside rests heavily on the data center segment, now expected to grow about 50% for the year. Looking further out, FY2028 revenue is projected at approximately $16.5 billion, about $1.5 billion higher than the previous forecast, showing that expectations continue to be pulled higher.

On the other hand, analysts are expecting Q2 FY2027 EPS to rise 32% YOY to $0.66. For the full FY2027, they project earnings growth of 42.1% to $3.07, followed by another 66.5% jump to $5.11 in FY2028.

What Do Analysts Expect for Marvell Stock?

Apart from KeyBanc, Marvell picked up another vote of confidence as B. Riley joined the upgrade chorus. Analyst Craig Ellis raised the price target from $240 to $345 while keeping a “Buy” rating intact on the shares.

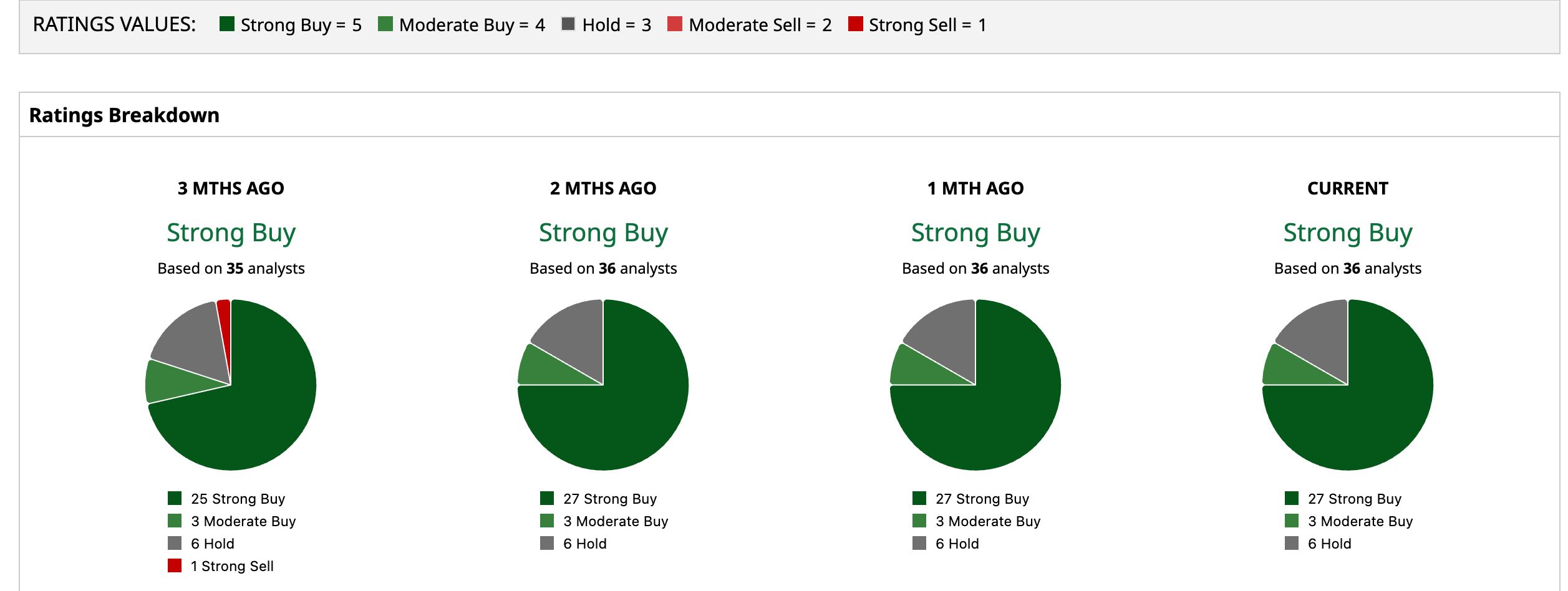

The broader sentiment around Marvell now sits comfortably in “Strong Buy” territory. Out of 36 analysts covering the stock, 27 have stamped it as a “Strong Buy” while three have taken a “Moderate Buy” stance, and six have chosen to sit on “Hold.”

The stock has already sprinted past its average price target of $244.16, and the Street-High target of $360 suggests a gain of 16.9% from current levels. Meanwhile, KeyBanc has pushed the envelope even further with its $385 price target, keeping the spotlight fixed on how far this networking-led rally can stretch.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Mark Cuban Says OpenAI Is ‘Sh*tting Away’ Its Money on AI Infrastructure: Says ‘They’ll Never Get’ a Return on Their Trillion-Dollar Spending Spree Marvell Just Got a New Street-High Price Target. Wall Street Thinks Networking Is a Huge Growth Opportunity. Michael Burry Just Refused to Buy the SpaceX IPO. Here Are 3 Companies He Is Buying Instead. Intel Will Design and Manufacture Chips for Apple. What This Really Means for INTC Stock Investors.