After years of testing investors’ patience, Intel (INTC) is finally showing signs of progress. Under CEO Lip-Bu Tan, the company has achieved a string of earnings beats, strengthened its AI strategy, and restored investors' confidence that its long-awaited recovery may be taking shape. Meanwhile, Advanced Micro Devices (AMD) is expanding its lead in AI infrastructure, gaining server market share, and profiting from surging demand for its data center and AI chips. While both semiconductor companies are compelling choices now, Goldman Sachs analyst James Schneider has a clear choice between Intel and AMD as to which offers a better risk/reward case.

The Case for Intel

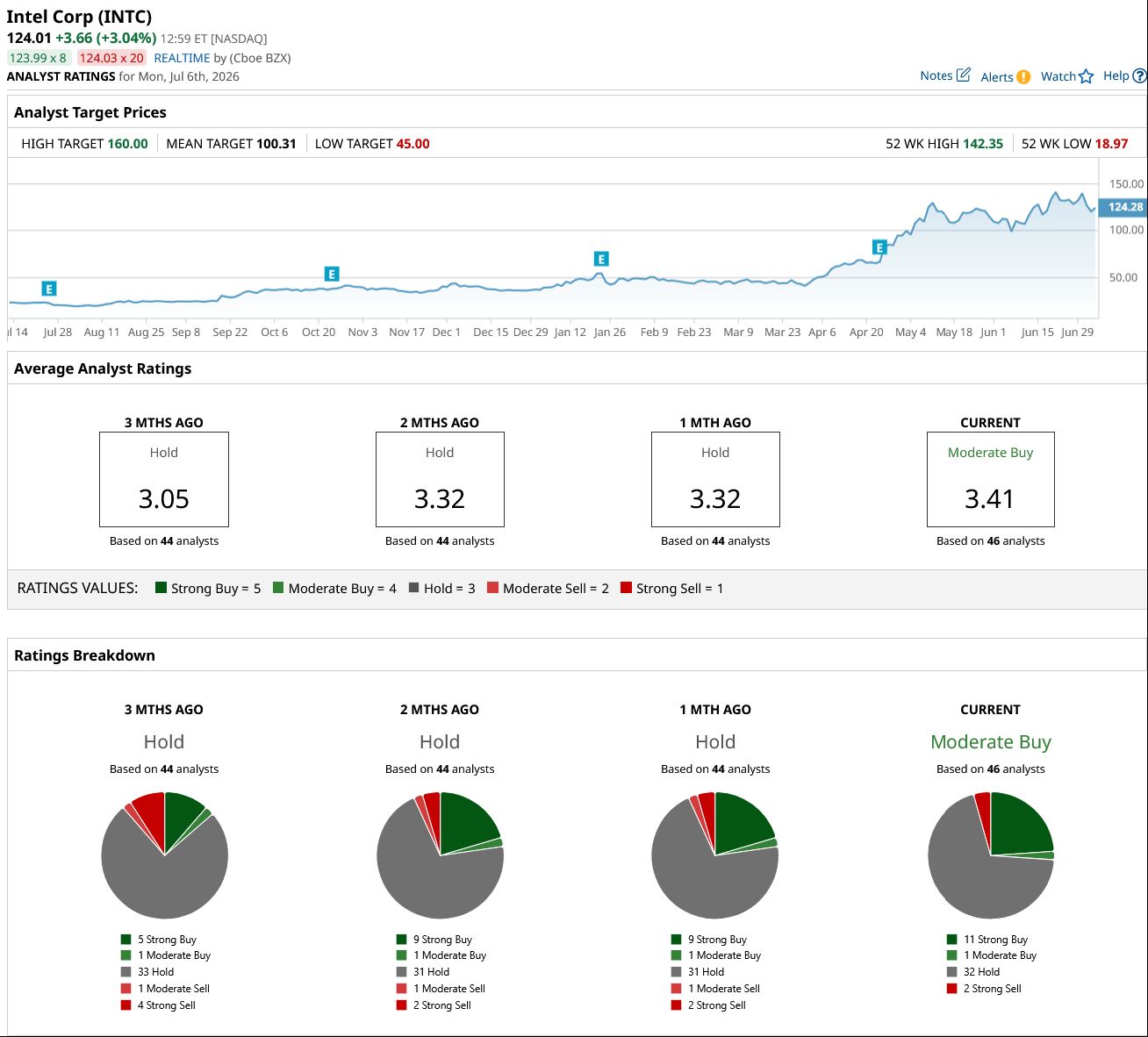

Recently, Goldman Sachs analyst James Schneider rated INTC stock a “Neutral,” with a target price of $150, which implies roughly 25% upside from current levels. While Schneider believes Intel has meaningful long-term catalysts, its closest competitors offer better revenue visibility and appear to be more attractive investment opportunities now.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

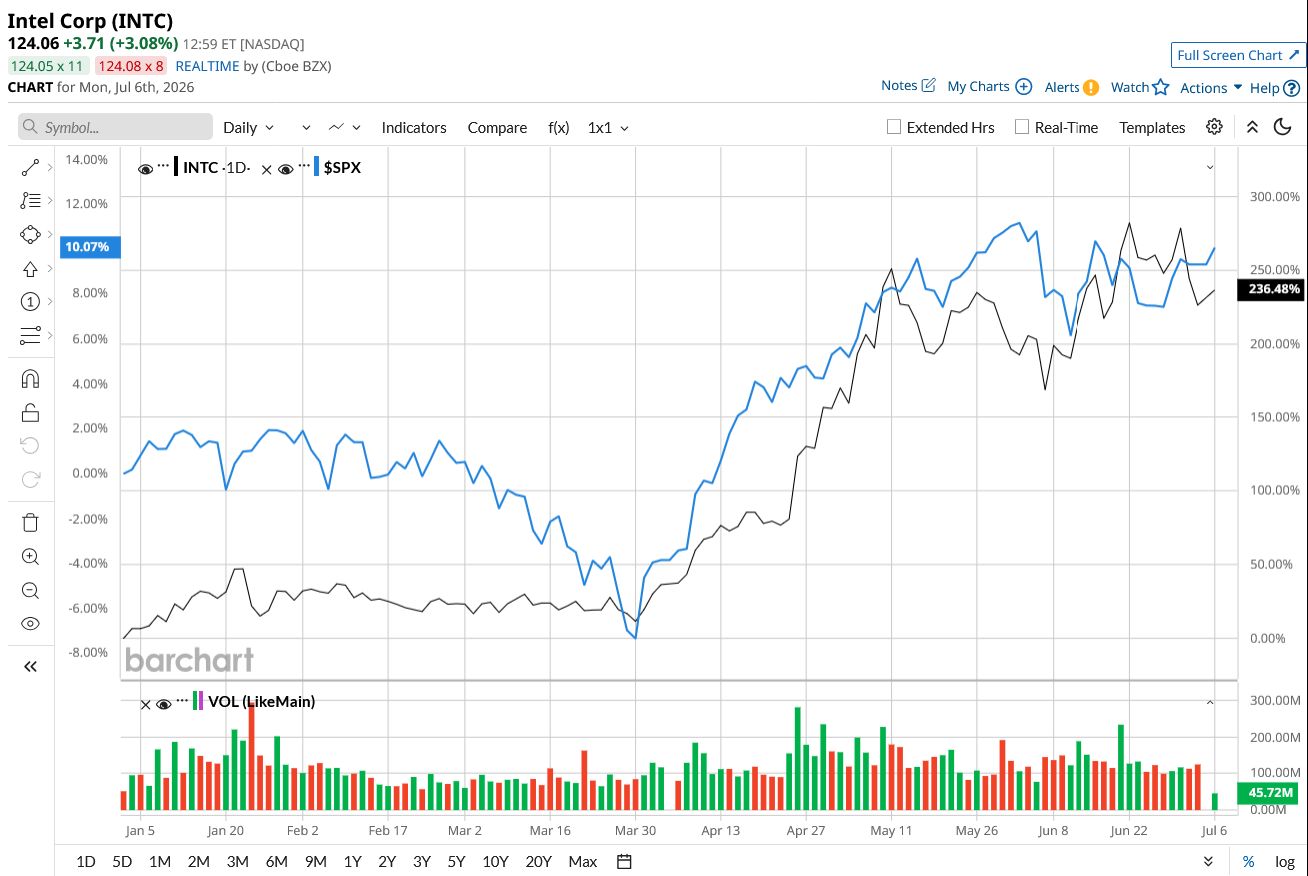

Here’s why I believe the analyst might be right. Intel’s investment case has dramatically changed over the last few years. After sitting out the AI boom, Intel has now attempted the most ambitious transformations in the semiconductor industry. INTC stock has surged 236% year-to-date (YTD), outperforming the S&P 500 Index ($SPX) gain of 10%.

www.barchart.com

www.barchart.com Much of that change has been driven by CEO Lip-Bu Tan, with operational discipline, stronger partnerships, and renewed focus on the company's core strengths. Intel’s first quarter results showed solid signs of progress, with revenue up 7% year-over-year (YoY) to $13.6 billion. Adjusted earnings came in at $0.29 per share, dramatically outperforming Wall Street's expectation of just $0.01 per share. It also marked Intel's sixth consecutive earnings beat.

Management also claimed in the Q1 earnings call that future agentic AI workloads may rely much more heavily on CPUs to coordinate increasingly complex tasks. Given Intel’s long-standing leadership in server processors, this opportunity could become significantly more valuable. The company is already seeing healthy demand for the company's Xeon processors. Hence, it is ramping up production for Intel 3-based Xeon 6 chips and Intel 18A-based Core Series 3 products. The company has also expanded partnerships with Alphabet's (GOOG) (GOOGL) Google and Nvidia (NVDA) to strengthen its AI ecosystem. Plus, collaborations with SpaceX (SPCX) and Tesla (TSLA) into next-generation semiconductor manufacturing technologies could be another long-term opportunity.

Goldman Sachs’ hesitation aligns with many other analysts’ views that Intel’s recent progress is not enough to justify the stock's premium valuation. Its foundry business is still operating at a loss as the company is investing aggressively in advanced manufacturing capacity. Free cash flow also remained negative at $2 billion in the quarter. Currently, Intel is trading at roughly 77 times projected 2027 earnings, with analysts expecting earnings to increase 42.6% from fiscal 2026 levels. This combination of improving execution, growing AI opportunities, and substantial financial risk explains why Goldman Sachs sees meaningful long-term upside for Intel while remaining cautious.

Overall, Wall Street maintains a consensus “Moderate Buy,” rating for INTC stock. Of the 46 analysts covering the stock, 11 rate it a “Strong Buy,” one says it is a “Moderate Buy,” 32 rate it a “Hold,” and two suggest it is a “Strong Sell.” INTC has surpassed its average target price of $100.31. However, its high price estimate of $160 implies an upside potential of 29% from current levels.

www.barchart.com

www.barchart.com The Case for AMD

Although Schneider believes Intel is well-positioned to benefit from the next wave of AI-driven server demand, he ultimately argues that investors have better opportunities elsewhere.

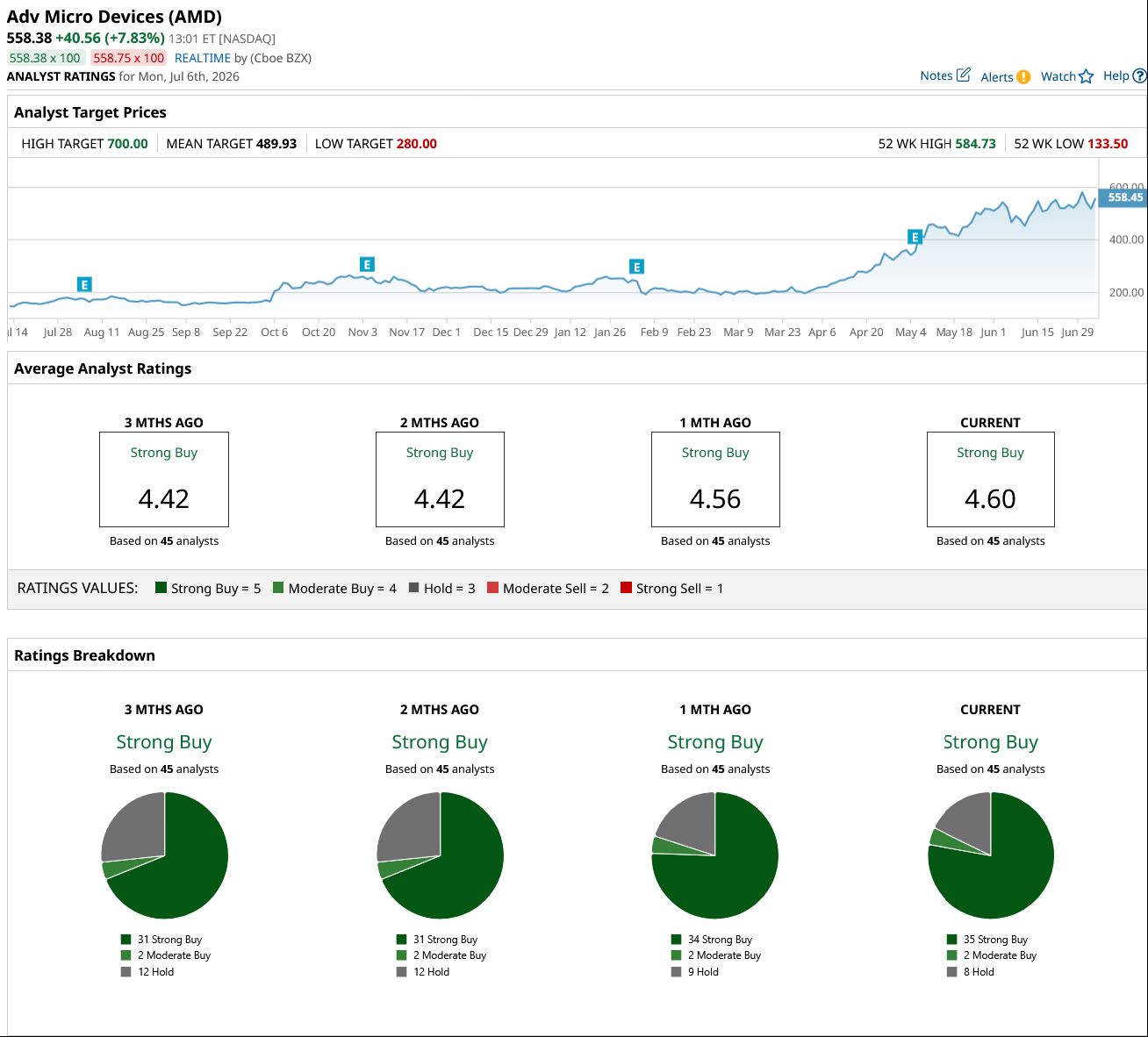

Advanced Micro Devices is one of them, which designs high-performance computer chips used in data centers, AI systems, personal computers, gaming consoles, and embedded systems. Its key products include EPYC server processors, Ryzen PC processors, Instinct AI GPUs, and Radeon graphics cards. AMD stock has skyrocketed 161% YTD, outperforming both the overall market and the tech-heavy Nasdaq Composite ($NASX).

www.barchart.com

www.barchart.com In the first quarter, AMD generated $10.3 billion in revenue, an increase of 38% YoY, while adjusted earnings per share climbed 43% to $1.37 per share. Its data center business generated $5.8 billion in revenue, led by the robust demand for EPYC server processors and Instinct AI accelerators. The company also continues to capture market share in server CPUs. Revenue from cloud and enterprise server CPUs each increased by more than 50% from the prior year. Its next-generation MI450 GPUs and Helios AI platform are gaining tremendous customer support.

For the second quarter, AMD forecasts a 70% YoY increase in server CPU revenue. Longer term, the company even expects the server processor market to grow at a compound annual rate exceeding 35% and expand beyond $120 billion by 2030. Furthermore, management believes its data center AI segment could produce “tens of billions” of dollars in yearly revenue by 2027, with growth expected to outpace its long-term target of over 80%.

Currently, AMD is trading at 39x forward 2027 earnings, with analysts expecting earnings to increase by 78% from fiscal 2026 levels. While AMD is also trading at a premium, it offers much better growth relative to its valuation. Intel commands nearly double AMD's valuation despite offering significantly slower expected earnings growth. This is probably why Goldman favors AMD because its earnings outlook reveals a company already benefiting from accelerating AI adoption and expanding market share.

On Wall Street, AMD stock holds an overall consensus of “Strong Buy.” Of the 45 analysts covering the stock, 35 rate it a “Strong Buy,” two rate it as a “Moderate Buy,” and eight rate it a “Hold.” The stock has surpassed its mean target price. But the high price estimate of $700 suggests it has an upside potential of 25% over the next 12 months. Besides AMD, Schneider also pointed to Nvidia having a “relatively balanced risk/reward at current share levels.”

So, Which Is the Better Buy Now?

For Goldman Sachs, AMD stands out as its growth story appears more solid and long-lasting. And I agree. With stronger revenue visibility, continued market share gains, expanding AI exposure, and fewer turnaround-related uncertainties, AMD remains the AI stock at current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Micron Expands Partnership With General Motors. What That Means for MU Stock. Skyworks Solutions Has Unusual Put Options Volume Today - A Short-Put Play Dear IBM Stock Fans, Mark Your Calendars for July 22 Intel vs. AMD: Goldman Sachs Analyst Thinks the Answer Is Clear