Coursera (COUR) stock was listed in March 2021 and the stock briefly traded at all-times highs above $50. With the Covid-19 pandemic necessitating shift to online classes, Coursera was among the beneficiaries.

However, the positive momentum in the stock was short-lived and the downtrend has sustained. In the last 52-weeks, COUR stock has declined 32.2% with negative sentiments on the back of growth concerns.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Notably, the online educational services industry is in a phase of consolidation. Coursera completed the merger with Udemy in June 2025 in an attempt toward diversification, cost optimization, and potential growth acceleration.

On July 6 in a development post-merger, Coursera announced cutting of jobs for “an unspecified number of employees.” The company expects to incur charges of $8 million to $11 million related to severance and other benefits. The announcement is a clear indication of the focus on optimizing the cost structure and possible margin expansion on merger synergies. While the impact of the merger and cost cutting remains to be seen, COUR stock seems oversold.

About Coursera Stock

Headquartered in Mountain View, Coursera operates an online learning platform. With global presence, Coursera unites educators, learners, and institutions, serving approximately 197 million learners from over 230 countries and territories as of December 2025.

The company has a widely addressable market through Coursera for individuals, enterprises, businesses, campus, and government. Further, Coursera Plus is a subscription offering giving learners access to over 13,500 courses, guided projects, specializations, and professional certificates.

For FY25, Coursera reported revenue of $757 million, which was higher by 9% on a year-over-year (YOY). For the same period, Coursera reported operating and free cash flow of $109 million and $78 million, respectively.

For FY26, Coursera has guided for revenue of $810 million. With relatively muted growth being a concern, COUR stock has declined by 22.3% in the last six months.

www.barchart.com

www.barchart.com Merger Benefits Can Create Value

With the completion of the Udemy merger, the focus is on building a stronger financial profile coupled with a leaner operating model. Coursera is also intent on building a next-generation platform for skills that will be relevant in the coming years.

From the perspective of financial stability, Coursera expects over 80% of Q1 FY26 revenue to be recurring. Growth in subscription in the enterprise and consumer segment is likely to support upside in recurring revenue and EBITDA margin expansion. For FY26, the company expects EBITDA margin of 13%.

Among specific growth triggers, there has been continued demand for AI courses. In Q1 FY26, AI courses witnessed 20 enrollments per minute. With launches from Alphabet (GOOG) (GOOGL) and Microsoft (MSFT) focused on delivering practical, job-ready skills, the AI segment is likely to remain a subscription growth driver.

Besides the course launches from the corporate sector, Coursera has more than 300 universities in its ecosystem. This supports subscription growth as learners get these universities listed on their course certificate, which boosts credibility. So, it's not surprising that registered learners have continued to grow on a steady basis and the addressable market is global.

An important point to note is that with the merger of Udemy, the company is positioned to benefit from the latter’s enterprise asset. For Coursera on a standalone basis, paid enterprise customer growth was relatively muted at 5% for Q1 FY26. With these potential benefits, COUR stock seems attractive.

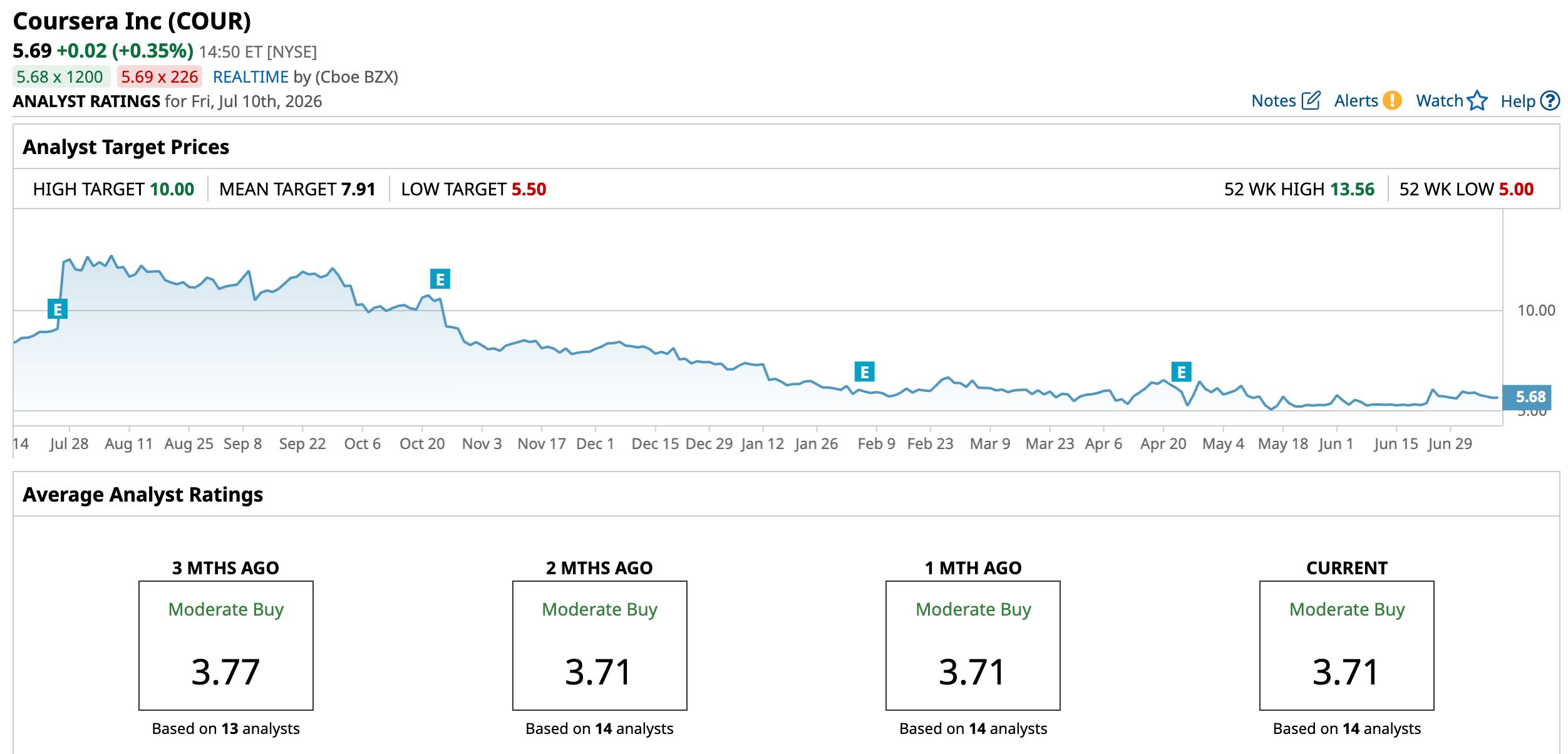

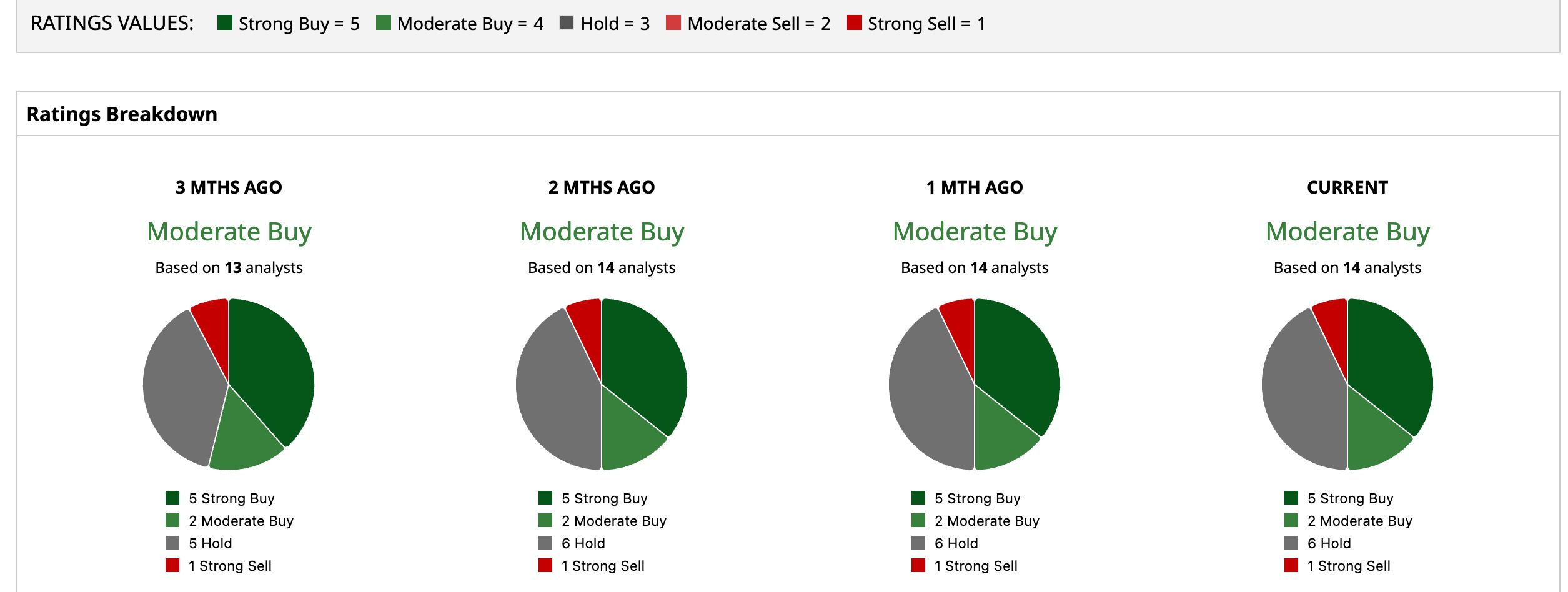

What Do Analysts Say About COUR Stock?

Based on 14 analysts with coverage, COUR stock has a consensus “Moderate Buy” rating. While five analysts have a “Strong Buy” rating for the stock, two have a “Moderate Buy,” six have a “Hold,” and one analyst has a “Strong Sell” rating.

The mean price target of $7.91 represents an upside potential of 39% from current levels. Further, the most bullish price target of $10 suggests that COUR stock could climb as much as 75.8% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Stock Has Been Flat, But NVDA Price Targets are Higher - Shorting Puts Works Why Analysts Still See Big Upside for Micron Stock After Its Massive Rally Coursera Stock Can Rally from Oversold Levels on Merger Synergies IBM Just Unveiled Major Updates to Its Bob AI Platform. How to Play IBM Stock Here.