Grok seems to be losing steam at a really sensitive moment, giving up ground to rivals. Just weeks after SpaceX’s (SPCX) landmark IPO pushed the company into public markets at a huge valuation, its flagship chatbot’s MAUs are down 5% quarter-over-quarter (QOQ) so far in Q2. That kind of drop naturally puts a shadow over the big growth story that helped get investors excited.

SpaceX did everything right on day one, jumping onto Nasdaq 100 Index ($NDXT) and quickly landing in major indices like the Russell 1000 Index. The move to fold xAI into the business and lean heavily on Grok as a key pillar now faces tougher questions, especially with clear signs that its momentum is slowing.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

So as Grok’s market share slips and its growth engine stutters, the core issue is hard to ignore. Is Grok just a short‑term drag on an otherwise strong story, or an early warning that SpaceX’s post‑IPO strategy isn’t as solid as it looks?

SpaceX’s Rich Valuation

SpaceX is a U.S. company that designs and launches rockets, runs the global Starlink satellite internet service, and builds advanced tools like Grok and voice agents. All of this sits inside one integrated space and technology business.

SPCX was only listed on June 12, yet the stock already sits at about $1.94 trillion in market value. The stock trades at -2.95% over the past five trading sessions.

www.barchart.com

www.barchart.com That price is backed by a price‑to‑sales multiple of 104.66 times versus a sector median near 1.21 times, which shows investors are paying a huge premium for future growth.

Their latest reported quarter for March 26 shows revenue of roughly $4.694 billion, up 15.42% year-over-year (YOY), so the core business is still growing. This same period delivered net income of about -$4.276 billion, with net income growth at -709.85%, making it clear that profits are under heavy pressure.

The company’s operating cash flow came in near $1.047 billion, but operating cash flow growth dropped -84.57%, pointing to a sharp squeeze on cash generation. That net cash flow figure of roughly -$8.516 billion, with a change in net cash flow of -162.51%, shows SPCX is burning a lot of cash to fund Grok and its wider AI plans.

SpaceX Tries to Build Around Grok

SpaceXAI is starting to show where it expects its next wave of growth to come from, and the moves are pretty clear. The company recently rolled out a no‑code voice agent builder that lets users create ready‑to‑use voice assistants in under two minutes without writing any code.

This tool runs on the Grok Voice model, offers more than 80 different voices, and supports 25 languages. That setup is aimed squarely at call centers, customer support teams, and sales groups that want something they can plug in and use quickly.

SpaceX is also putting the hardware and energy side in place to back this strategy. The company plans to build an eight‑mile natural gas pipeline in Texas, called Starpipe, running from land near the Port of Brownsville to its Starbase launch site. This line is scheduled to start construction next month and is expected to be in service by January 2027, supplying fuel directly for more frequent Starship launches.

Together, these moves make it clear SpaceX is trying to build a full stack around Grok.

Analysts Lean Hard Into SPCX’s Future

Earnings expectations for SpaceX right now tell a simple story. For the current quarter ending June 2026, the average earnings estimate sits at about $-0.23 per share, with an estimated YOY growth rate of -100.02%.

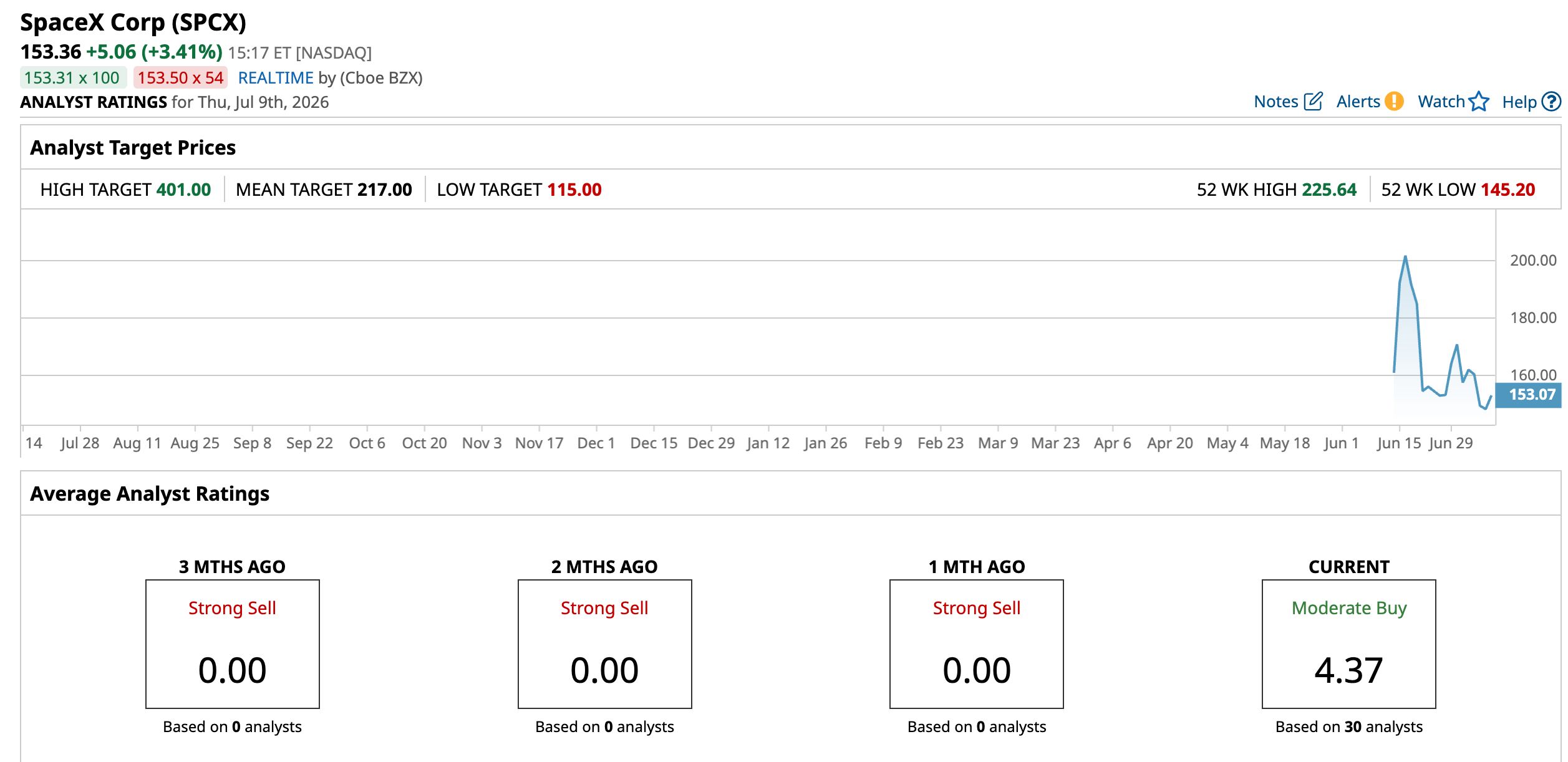

Other analyst price targets follow that idea of heavy spending now and potential rewards later. Morgan Stanley is set to release its full view this week, and analyst Adam Jonas has already floated a $300 target for SPCX, roughly 102% upside.

Raymond James goes even further, putting an extremely aggressive $800 target, around 439% upside, on the stock.

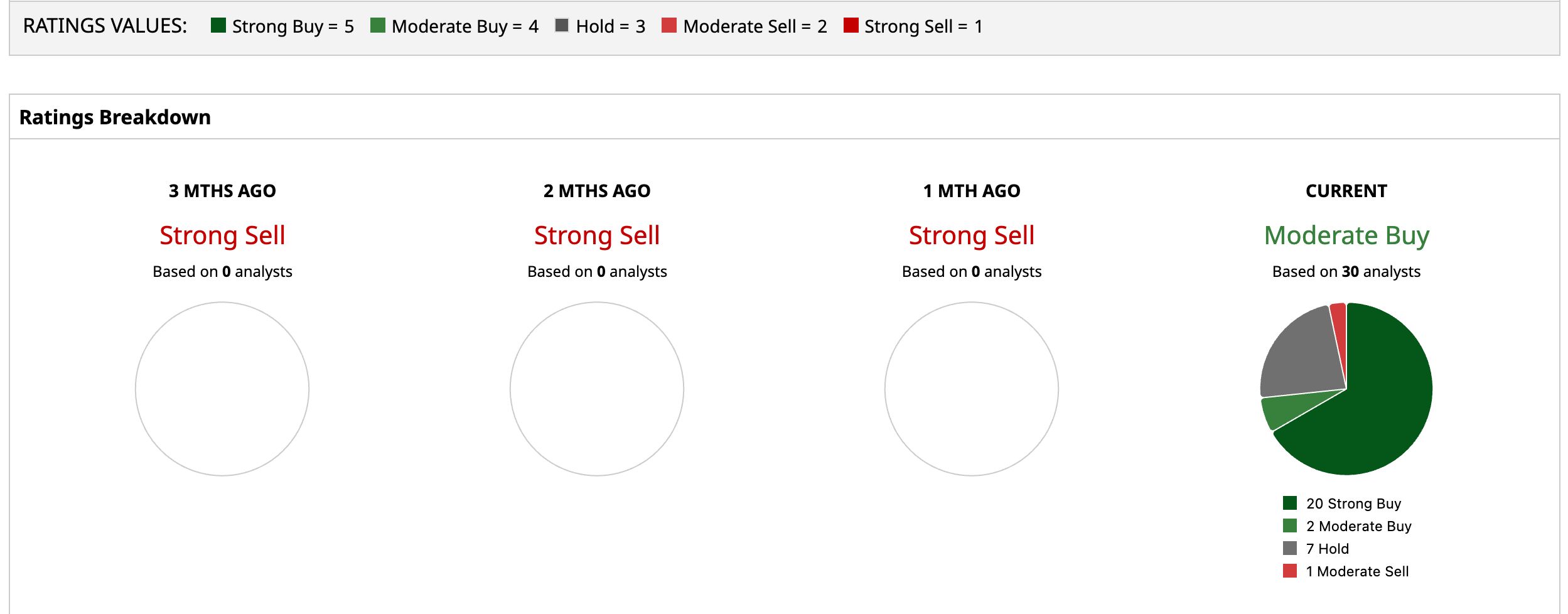

Consensus still leans firmly in the bullish camp. The latest survey of 30 analysts shows a consensus “Moderate Buy” rating. The average price target comes in at $217, which implies roughly 41.5% upside from the stock's current trading price.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Grok’s market share decline clearly dents the tidy AI growth story around SPCX, but it doesn’t kill the “Strong Buy” thesis. SpaceX is stacking new AI products and infrastructure, giving the stock real optionality if execution improves. In the near term, shares look more likely to grind sideways or drift slightly lower as investors test that narrative. Longer-term direction hinges on one thing above all else, whether SpaceX can turn Grok from a lagging chatbot into a meaningful earnings driver.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Navitas Semiconductor Stock Is on the Ropes. It Faces a New Patent Infringement Lawsuit. Grok’s Ongoing Market Share Decline Raises Questions About SpaceX’s AI Strategy Post-IPO Starbucks Is Serving Up Your Coffee with a Side of AI. What That Means for SBUX Stock. Nvidia Stock Has Been Flat, But NVDA Price Targets are Higher - Shorting Puts Works