Alphabet’s (GOOG) (GOOGL) Google has spent the past few years establishing itself as one of the biggest forces in artificial intelligence (AI). From expanding Gemini across Search, Workspace, and Android to investing heavily in custom TPUs and next-generation data centers, the tech giant has built a powerful AI ecosystem backed by world-class models, massive computing resources, and billions of users.

But the AI race is only getting more competitive. Meta Platforms (META), the parent company of Facebook, Instagram, WhatsApp, and Threads, has ruled a digital empire. Now, it is betting big on AI with an aggressive push to become one of the industry’s top AI players. Under CEO Mark Zuckerberg, it has committed billions of dollars to AI infrastructure, custom chips, top-tier talent, and a network of gigawatt-scale data centers designed to dramatically increase its computing power. Meta is also accelerating the rollout of new AI models and developer tools as it races to build more capable AI agents.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That strategy is beginning to turn heads on Wall Street. A new report from boutique research firm SemiAnalysis argues that Meta’s aggressive infrastructure buildout and expanding AI compute capacity could allow it to surpass Google’s AI capabilities within the next six months. Further, the report projects that Meta could overtake both OpenAI and Anthropic in total AI compute by year-end, thanks to its massive data center expansion and proprietary AI training ecosystem. The bullish assessment sent META shares higher and has investors asking whether Meta could become the next AI leader.

To that end, let’s see how investors should play META stock here.

About Meta Stock

Meta Platforms hardly needs an introduction. Born as Facebook in 2004, the company has evolved far beyond its dorm-room origins into a global digital ecosystem spanning Instagram, WhatsApp, Messenger, and now Threads. What began as a simple newsfeed has steadily transformed into a platform shaping the ways in which billions communicate, create, and connect. Today, Meta is leaning hard into AI, augmented reality, and its long-term metaverse ambitions, positioning itself as infrastructure for the next wave of digital interaction.

That long-term vision has made Meta one of Wall Street’s biggest success stories. The stock has surged 440% over the past decade, helping the company grow into a tech giant with a market capitalization of $1.7 trillion and cementing its place among the “Magnificent Seven.”

However, the ride has not been entirely smooth. Over the past 52 weeks, META stock has slipped 7.7% and remains 17% below its all-time high of $796.25. Much of that weakness stemmed from familiar investor concerns, including uncertainty around advertising demand, soaring AI-related capital spending, and questions about when those massive investments would begin generating meaningful returns.

However, sentiment has shifted noticeably in recent weeks. Meta stock has recently regained momentum as investors have started viewing its massive AI spending as a long-term growth driver rather than a near-term cost burden. Confidence has been boosted by the rollout of its custom Iris AI chip, expanding gigawatt-scale data center plans, and the launch of the competitively priced Muse Spark 1.1 model. Together, these initiatives could lower computing costs, create new AI revenue opportunities, and strengthen Meta's position in the fast-growing AI market, improving investor sentiment toward the stock. Over the past five days alone, META stock is up 10.35%.

From a technical standpoint, momentum also appears steady. The 14-day RSI sits at 64.36, approaching, but not yet deep into, overbought territory, while the MACD oscillator signals bullishness with positive histogram bars, suggesting buyers continue to hold the upper hand and the recent upward momentum could have further room to run.

www.barchart.com

www.barchart.com Valuation-wise, Meta may appear expensive, trading at 21.44 times forward price-to-earnings and 6.72 times forward sales, both above sector averages. However, the stock remains below its own historical valuation levels for its forward P/E. Given Meta's expanding AI ambitions and strong earnings growth potential, that premium looks increasingly justified and could become more attractive as future growth catches up. Plus, Meta has been rewarding shareholders through dividends.

A Snapshot of Meta’s Q1 Earnings Report

In the first quarter of fiscal 2026, reported on April 29, Meta’s revenue climbed 33.1% year-over-year (YOY) to $56.3 billion, comfortably beating Wall Street’s expectations. Profit growth was even more impressive, with EPS surging 62.4% annually to $10.44, well ahead of analysts’ estimates.

The company’s massive user base continued to grow. Family daily active people – which includes users across Facebook, Instagram, WhatsApp, and Messenger – reached 3.56 billion in March, up 4% YOY. Management noted that a slight sequential decline was largely due to internet disruptions in Iran and restrictions on WhatsApp access in Russia.

Meta’s advertising engine also remained remarkably healthy. Ad impressions across its family of apps increased 19% YOY, while the average price per ad rose 12%, highlighting strong advertiser demand. Meanwhile, headcount, as of March 31, edged up just 1% annually to 77,986, reflecting disciplined hiring despite the company’s aggressive AI expansion.

Still, investors initially focused on spending. Meta lifted its 2026 capital expenditure guidance to $125 billion to $145 billion, largely to fund its AI infrastructure buildout, triggering an 8.55% drop in the stock after earnings despite the strong quarterly results.

Meta is scheduled to report its second-quarter FY2026 results later this month. Management has guided revenue in the range of $58 billion to $61 billion.

Meanwhile, Wall Street expects Q2 EPS to come in at $7.09, reflecting a modest YOY decline. Looking further ahead, analysts project full-year FY2026 EPS of $29.46 before rebounding strongly to $35.18 in FY2027, representing 19.4% annual EPS growth.

Why SemiAnalysis Thinks Meta Could Leapfrog Google in AI

For years, Google has been viewed as having one of the deepest AI moats in the industry. But according to SemiAnalysis, that advantage may not last much longer. In a new report, the firm argues that Meta’s AI strategy is no longer just about building better models but about building a bigger and more efficient AI engine. SemiAnalysis believes Meta Superintelligence (MSL) could surpass Google’s AI capabilities within the next six months, driven by an unprecedented combination of computing power, proprietary data, and elite AI talent.

One of the biggest reasons is infrastructure. The report estimates that Meta will overtake both OpenAI and Anthropic in total AI compute by the end of the year as it simultaneously builds five gigawatt-scale “Titan” data center clusters. These facilities will be connected through Meta’s custom AI-Backbone networking architecture, allowing the company to train massive AI models across data centers located thousands of kilometers apart as if they were operating together.

But hardware is only part of the story. While many AI companies are competing for increasingly limited public training data, Meta is creating its own advantage. According to SemiAnalysis, the company has reassigned roughly 3,000 engineers to build an in-house reinforcement learning environment that generates proprietary training data from real employee workflows. That gives Meta a unique data pipeline that rivals cannot easily replicate.

Also, Meta is investing aggressively in the people needed to turn that infrastructure into better AI. The company has spent billions to recruit top researchers from rivals, including OpenAI, Anthropic, and Scale AI, while continuing to expand its frontier AI team.

SemiAnalysis summed up its view with a message that investors should not focus only on where Meta’s latest AI models rank today. Instead, they should pay attention to the pace of improvement. If Zuckerberg continues investing at the current rate, the firm believes Meta has a realistic chance of leapfrogging Google in frontier AI capabilities within the next couple of months.

What Do Analysts Expect for Meta Stock?

Despite the bullish view from SemiAnalysis, not everyone on Wall Street is becoming more aggressive on Meta. Citizens analyst Andrew Boone maintained a “Buy” rating but trimmed his price target to $800 from $825, not because of weakening confidence, but because of Meta’s soaring AI investment plans.

Boone praised the launch of Muse Spark 1.1, calling it a meaningful step toward competing with frontier AI labs, and believes the Meta Model API could open new revenue streams through model access and advertising. However, with AI compute needs accelerating and capex potentially reaching $200 billion in 2027, he expects near-term profitability to remain under pressure, prompting a lower valuation multiple despite improving long-term growth prospects.

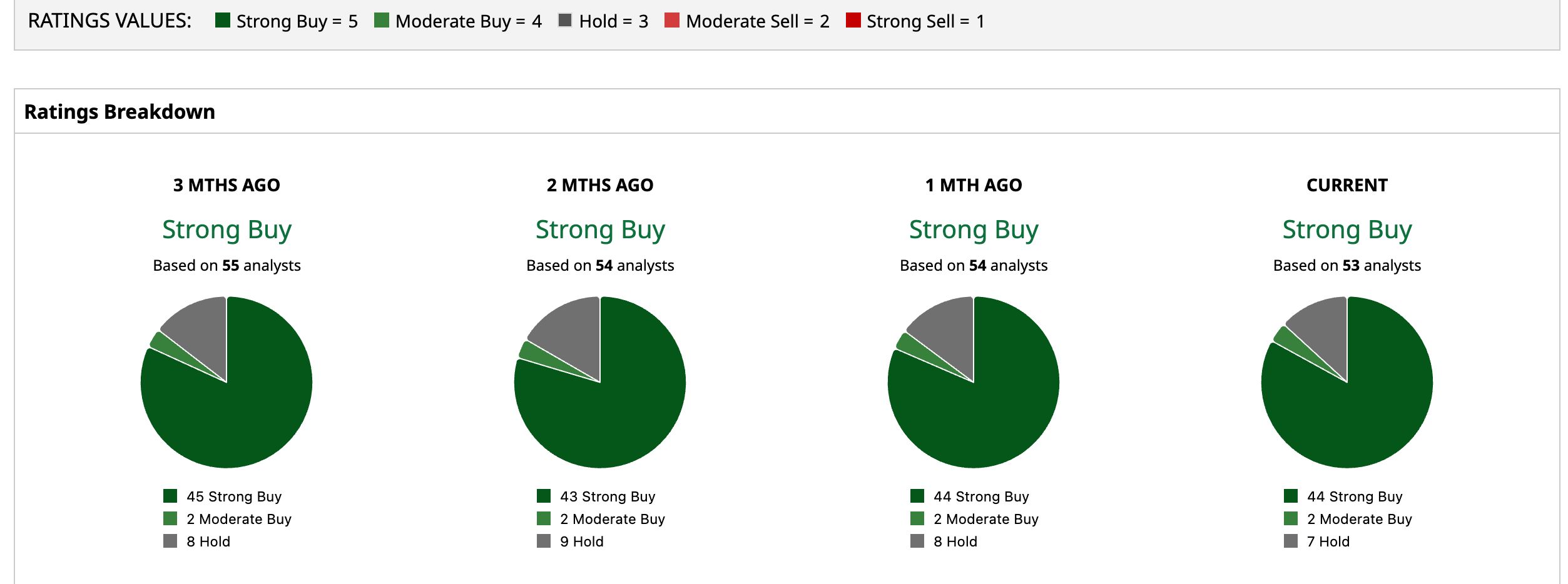

Overall, Wall Street is flashing the green flag for META, with a “Strong Buy” consensus reflecting widespread optimism about the stock’s growth prospects. Of the 53 analysts offering recommendations, 44 are giving it a solid “Strong Buy,” two suggest a “Moderate Buy,” and seven give a “Hold.”

META’s average analyst price target of $823.30 implies a 24.7% upside potential. Meanwhile, the Street-high price target of $1,015 suggests that the stock can still rally as much as 53.8% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Delta Air Lines Could Be a Top Stock to Buy for the Rest of 2026 Why Analysts Are Betting Western Digital Stock Can Gain Another 30% from Here COIN Stock Alert: 3 Reasons Why Coinbase Shares Are In Focus A New Report Says Meta Platforms Could Overtake Google AI. How to Play META Stock Here.