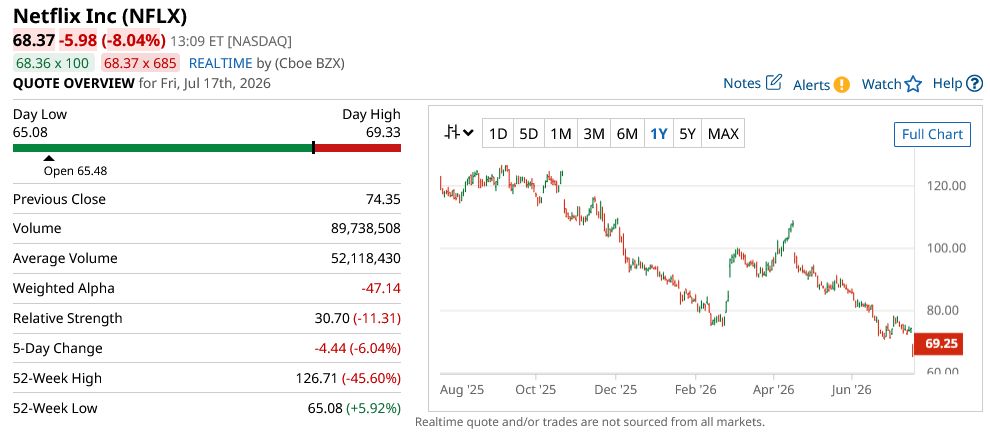

Markets have become increasingly impatient with even the slightest sign of slowing growth. Companies can deliver billions in revenue, rising profits, and healthy cash flow, yet a modest adjustment to guidance can erase tens of billions of dollars in market value overnight. That's undoubtedly what happened with Netflix (NFLX).

While traders focused on its guidance following second-quarter earnings, long-term investors should focus on something far more important: whether the company's competitive position and earnings power remain intact. By that measure, Netflix still looks like one of the strongest media businesses in the market.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comStrong Results Were Overshadowed by Guidance

Second-quarter revenue climbed 13% year-over-year (YoY) to $12.6 billion, while net income increased 9% to $3.4 billion. Those aren't the numbers of a business losing momentum.

Instead, investors zeroed in on management's guidance. Netflix said Q2 revenue would grow about 12% with the full year narrowed to approximately $51.0 billion, while Wall Street had been expecting roughly $51.38 billion. That modest change was enough to push NFLX stock down more than 8% in trading Friday.

Yet management appeared far less concerned than the market. During the earnings call, Chief Financial Officer Spencer Neumann characterized the quarter-to-quarter movement as little more than background noise, pointing investors toward the much larger opportunity ahead.

Netflix estimates there are roughly 800 million addressable households across the markets it serves, representing a $670 billion revenue opportunity. Today, management believes it captures only about 7% of that revenue pool and roughly 5% of global TV viewing share.

Those numbers suggest Netflix's biggest growth opportunities still lie ahead, not behind it.

Wall Street Turns More Cautious

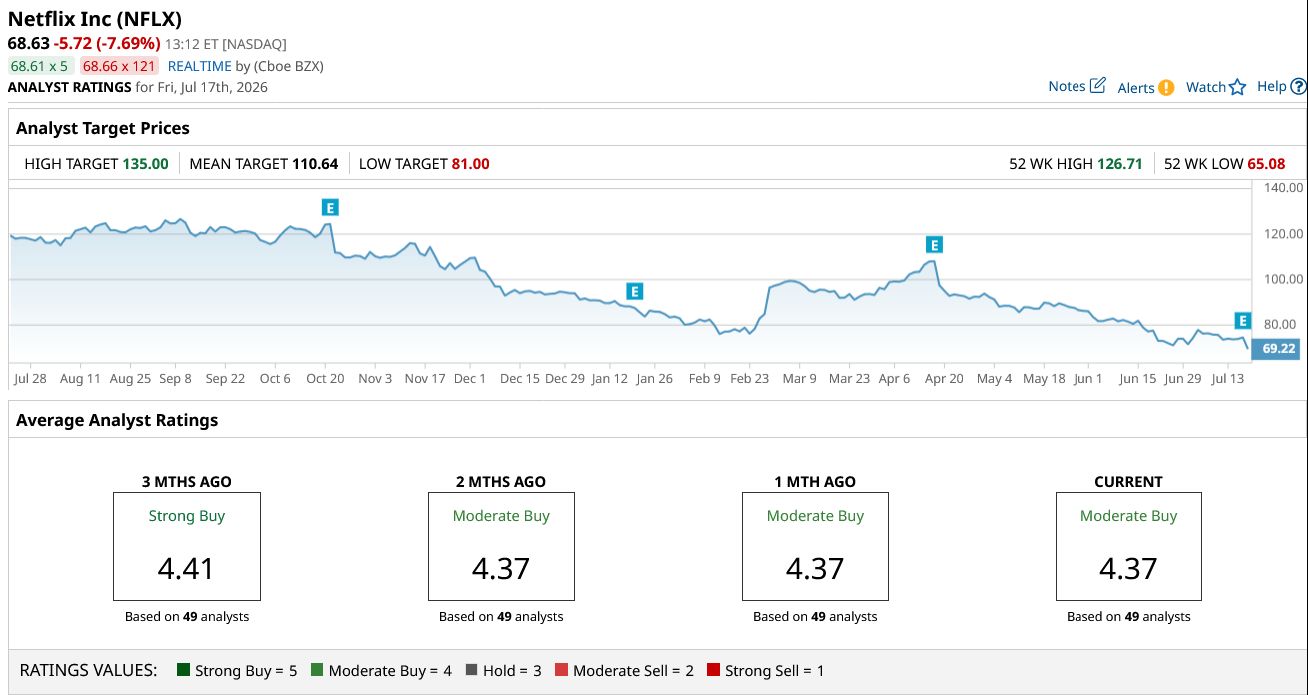

The weaker guidance also prompted a swift response from Wall Street. At least 11 brokerage firms lowered their price targets following the earnings release, reflecting the more conservative near-term revenue outlook rather than any deterioration in Netflix's underlying business.

Most analysts maintained positive ratings on the stock, choosing to trim valuation assumptions instead of changing their long-term investment thesis. In other words, the debate shifted from what Netflix is worth today to can it continue growing tomorrow.

That lines up with management's own message, with Neumann arguing investors should instead focus on Netflix's much larger runway for international expansion and advertising growth.

www.barchart.com

www.barchart.comAdvertising and Buybacks Add Fuel for Future Returns

Advertising continues to evolve into one of Netflix's largest growth drivers. Before this earnings release, the company saw a 60% increase in first-quarter ad-supported plan sign-ups in advertising markets. Its advertiser base also expanded 70% YoY to more than 4,000 clients, while management previously targeted approximately $3 billion in advertising revenue during 2026—double the prior year's level.

Management noted that advertising contributed meaningfully to Q2 revenue growth and expects that trend to continue into the third quarter.

Meanwhile, capital allocation is becoming another tailwind. After missing out on acquiring Warner Bros. Discovery (WBD), Netflix resumed returning cash to shareholders. It bought back $1.3 billion worth of stock in Q1 and has announced an additional $25 billion authorization on top of the $6.8 billion remaining on the prior one.

Valuation Looks Better Than the Reaction Suggests

Before earnings, shares traded at roughly 29 times earnings and about 34 times free cash flow. Those valuations are broadly in line with the S&P 500 ($INX) despite Netflix continuing to grow revenue at a low- to mid-teens pace—faster than many large-cap technology and media peers.

Ironically, the market is pricing Netflix similarly to the broader index while the company still has a long runway through international expansion, advertising, and increasing engagement.

With NFLX stock now down roughly 46% from its 52-week high, investors are being offered a much more attractive entry point than they had just days ago.

Key Takeaway

In short, Wall Street punished Netflix for a guidance adjustment measured in a few hundred million dollars while largely ignoring a business that continues to grow revenue, expand profits, build its advertising platform, and return billions to shareholders through buybacks.

No one can consistently buy at the exact bottom, but as Netflix continues expanding into a $670 billion addressable market while monetizing only a fraction of its global audience today, this roughly 10% earnings-driven decline looks like one of the better buying opportunities the market has offered this year.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Just Punished Netflix’s Guidance, But the Real Story Could Send the Stock Much Higher After This Stock Popped on Earnings, Options Traders Are Betting $6.8 Million on a Short Call Diagonal Spread Why Circle Stock Is the Most Divisive Name in Fintech Right Now Why Piper Sandler Likes AST SpaceMobile (ASTS) Stock Over Other Space Stocks