Academy Sports and Outdoors, Inc. ASO used its first-quarter fiscal 2026 earnings call to argue that its growth engine is gaining traction again, even as management described a pressured discretionary backdrop. The company returned to positive comparable-sales growth, raised its sales outlook and pointed to momentum in e-commerce, new stores and loyalty.

The more important message from the call was forward-looking. Executives framed the rest of the year around self-help initiatives, offsetting weaker lower-income demand and the drag from elevated gas prices.

ASO Returns to Positive Comps Growth

Chief executive officer Steven Lawrence said that fiscal first-quarter sales of $1.44 billion rose 6.7%, while comparable sales increased 2.9%, with traffic up in the low-single digit and average unit retail up in the high-single digit. Lawrence said that the results marked a return to comps growth and came in at the high end of the range that management had discussed in April.

The quarter also topped the Zacks Consensus Estimate on both key headline metrics. Adjusted earnings were $0.93 per share, beating the Zacks Consensus Estimate of earnings of $0.91. Revenues of $1.442 billion surpassed the consensus estimate of $1.439 billion. That translated to an earnings surprise of 2.20% and a revenue surprise of 0.20%.

Chief financial officer Earl Ford said that e-commerce remained a standout, growing more than 17% and expanding penetration by 100 basis points. Ford added that all four divisions posted gains, with outdoor up 12%, sports and recreation rising 6%, apparel growing 5% and footwear inching up 3%.

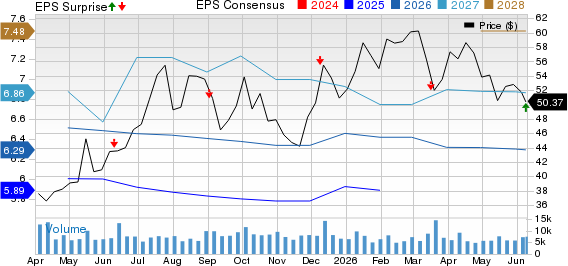

Academy Sports and Outdoors, Inc. Price, Consensus and EPS Surprise

Academy Sports and Outdoors, Inc. price-consensus-eps-surprise-chart | Academy Sports and Outdoors, Inc. Quote

ASO Benefits From Category & Brand Momentum

Lawrence highlighted outdoor as the strongest business, supported by fishing and shooting sports. He said the ammunition business turned positive in February after creating headwinds for much of last year, while firearms continued to gain share based on NICS checks data.

During the earnings call, Academy Sports also highlighted newer merchandise initiatives. Lawrence said that suppressors were launched in a limited number of stores during the quarter and are planned for more than 100 stores by the year-end, positioning the category as an incremental sales driver with a high attachment rate to firearms.

On the branded side, management pointed to continued strength in Nike and Jordan, along with growth in better private brands such as Freely and R.O.W. Lawrence said that the combined Nike and Jordan business rose at a mid-single-digit rate and the trend is expected to continue through the year.

ASO Puts More Weight on Loyalty & Digital

A central theme of the call was the relaunch of My Academy Rewards. Lawrence described a three-tier structure spanning base loyalty, a private-label credit card and a co-branded Mastercard, with the program built to increase engagement and make value more visible at the point of sale.

Management said that enrollment is already running up in the double digits year over year and that the goal is to add 2 million members this year, bringing the total loyalty membership above 15 million. Lawrence framed the offer as especially timely because customers are looking for ways to stretch spending.

The digital agenda also remains active. Lawrence said that Academy Sports is expanding same-day delivery to Uber Eats and Instacart in addition to DoorDash, while also planning to migrate on-site search to Google AI Commerce search and Gemini Enterprise tools ahead of the back-to-school season.

Academy Sports Raises Sales Outlook but Retains Margin View

Ford said that the gross margin fell 71 basis points to 33.2% in the quarter, mainly because of tariffs. He broke down the pressure in Q&A, saying tariffs created a 110-basis-point headwind that was partly offset by improvements in shrink and shipping.

Even with that pressure, ASO raised its full-year sales guidance to $6.23-$6.35 billion from $6.15-$6.35 billion. The comparable-sales guidance moved to flat to up 2% from down 1% to up 2%, while adjusted earnings per share guidance remained at $6.40-$6.80.

Ford said that the company expects first-half gross-margin pressure followed by modest back-half expansion, leaving the full-year gross-margin outlook unchanged at 34.5-35%.

ASO Q&A Centers on Consumer & Tariffs

Analysts pressed management on whether the strong fiscal first quarter could hold as tax-refund benefits fade. Lawrence said that the business is likely to soften in the fiscal second quarter, with total sales through Memorial Day rising in the low-single digit and comps staying roughly flat, which he tied to higher gas prices.

A Goldman Sachs analyst asked about margin pressure and category mix. Ford responded that tariffs were the main culprit, and the lower-margin outdoor mix, including ammo, was a factor but not the primary driver.

A UBS analyst also pushed on what bridges fiscal first-quarter comps strength to the rest of the year. Ford said that management’s initiatives alone get the business to the mid-point of its full-year comps outlook, while the wider range depends on the lower-income consumer and external events, such as the World Cup and America’s 250th anniversary.

Academy Sports Tone Stays Constructive but Cautious

The call left a measured impression. Lawrence repeatedly emphasized that Academy Sports is building momentum through new stores, loyalty, digital capabilities and category expansion, while also acknowledging a cautious consumer who is increasingly shopping around promotions.

Ford reinforced that posture by pointing to a strong balance sheet, a healthy free cash flow and continued capital returns, but he did not downplay the impacts of gas prices, freight and tariffs on the year’s shape.

Zacks Signals Point to Balanced Setup

ASO currently carries a Zacks Rank #4 (Sell), alongside a Value Score A, a Growth Score A, a Momentum Score C and a VGM Score A.

Under the Zacks framework, strong Style Scores are most favorable when paired with a Zacks Rank #1 (Strong Buy) or 2 (Buy), while 4 outweighs attractive style characteristics. The A grades on value, growth and VGM indicate favorable underlying style traits, but the current rank points to weaker near-term estimate revision momentum. You can see the complete list of today’s Zacks #1 Rank stocks here.

The combination leaves a mixed signal after the quarter. The Style Scores suggest that ASO has appealing characteristics on several measures, but the Zacks Rank remains the more important screen and can change as earnings estimates are revised following the latest results.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Academy Sports and Outdoors, Inc. (ASO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).