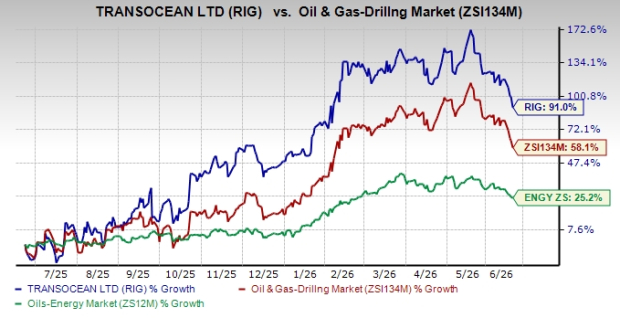

Over the past 12 months, Transocean Ltd. RIG, a Switzerland-based oil and gas drilling company, has significantly outperformed both its industry and the broader energy sector. RIG’s shares have gained 91% during the period, comfortably exceeding the 58.1% return of the Oil & Gas Drilling sub-industry (ZSI134M) and the 25.2% growth recorded by the broader Oil-Energy Sector (ZS12M). The strong relative performance reflects investors' growing confidence in Transocean's premium offshore drilling fleet, improving contract backlog and favorable market conditions supporting offshore exploration activity.

Analysis of 12-Month Share Price Movement

Image Source: Zacks Investment Research

With the offshore drilling market showing signs of recovery, investor attention has increasingly turned to Transocean to assess its long-term investment potential. The company stands to benefit from rising demand for offshore rigs and an expanding contract backlog, although its shares have remained volatile amid broader energy market uncertainties.

Against this backdrop, evaluating the key factors shaping RIG's recent performance is essential to determine whether the stock presents an attractive buying opportunity at current levels or whether investors should adopt a more cautious stance.

Factors Driving RIG's Competitive Strength

Strong Contract Backlog Provides Long-Term Revenue Visibility: RIG significantly strengthened its earnings visibility by adding approximately $1.6 billion of new contracts and extensions during the reporting period, lifting total backlog to more than $7 billion. The high level of contracted work for both 2026 and 2027 reduces earnings uncertainty, supports future cash generation and provides greater confidence that the company can continue deleveraging while benefiting from improving offshore drilling demand.

Exceptional Operational Performance Supports Margin Expansion: RIG delivered outstanding operational execution with approximately 98% uptime and revenue efficiency above 97%, allowing contract drilling revenues to exceed expectations. High fleet utilization combined with disciplined cost management resulted in adjusted EBITDA margin exceeding 40%, demonstrating that the company is efficiently converting stronger market conditions into improved profitability and cash generation.

Multi-Year International Contracts Improve Earnings Stability: Recent contract awards across Norway, Brazil and the Eastern Mediterranean extend the operating lives of several high-specification rigs through the end of the decade. These long-duration agreements reduce idle time, improve fleet utilization and establish predictable cash flows, positioning Transocean to benefit from sustained offshore investment over multiple years.

Energy Security Concerns Reinforce Long-Term Offshore Demand: Management believes recent geopolitical developments have highlighted the importance of reliable offshore oil and gas production. Governments and operators are increasingly prioritizing domestic and diversified energy supplies, which is expected to support continued investment in deepwater exploration and development, creating favorable long-term demand for Transocean's specialized drilling fleet.

Premium Fleet Positioning Supports Pricing Power: Transocean operates one of the industry's highest-specification ultra-deepwater and harsh-environment fleets. Management indicated that customers increasingly require these premium assets for long-duration development programs, allowing the company to pursue higher-value contracts while maintaining strong utilization as offshore activity expands globally.

Why Investors Should Be Cautious About RIG

Offshore Drilling Remains Exposed to Geopolitical and Macroeconomic Risks: While management believes global energy security supports offshore investment, the business remains vulnerable to geopolitical events, changes in commodity prices, regulatory developments and customer capital allocation decisions. These external factors are largely outside Transocean's control and could materially influence contract activity and long-term financial performance.

Near-Term Revenues Remain Concentrated in Existing Contracts: Management indicated that revenue guidance is primarily supported by firm contracts, while upside depends on new awards commencing earlier than expected or existing contracts being extended. If negotiations progress more slowly than anticipated, Transocean may experience weaker revenue growth than investors currently expect.

Earnings Remain Highly Dependent on Offshore Drilling Demand: Transocean's future performance relies heavily on continued customer spending for offshore exploration and development projects. Any decline in oil prices, reductions in capital budgets or postponement of drilling programs could weaken contract awards, increase idle rig time and negatively affect revenue growth despite the company's current backlog.

Rising Operating Costs Could Pressure Future Margins: Management acknowledged early signs of inflation from higher logistics, freight and energy-related costs following geopolitical disruptions. While current financial guidance remains unchanged, persistent inflation across equipment, services and supply chains could gradually increase operating expenses and reduce profitability if cost recovery mechanisms prove insufficient.

Capital Expenditure Requirements Have Increased: Management raised expected capital expenditures because of additional customer-related requirements, including environmental upgrades for a rig operating in Norway. Although part of these costs is expected to be recovered, higher capital spending reduces near-term free cash flow and highlights the ongoing investment needed to maintain a competitive offshore drilling fleet.

Verdict for RIG Stock

Transocean is supported by a strong contract backlog, premium ultra-deepwater fleet, multi-year international contract awards and exceptional operational execution, which provide solid revenue visibility, stable cash flows and healthy margin expansion. The company also stands to benefit from sustained offshore drilling demand driven by energy security concerns and its strong positioning in high-specification drilling markets.

However, its earnings remain highly dependent on offshore drilling activity, customer capital spending and commodity prices, while rising operating costs, higher capital expenditures and potential delays in new contract awards could weigh on near-term financial performance. Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this Zacks Rank #3 (Hold) stock to their portfolios.

Key Pick

Investors interested in the energy sector might look at some better-ranked stocks like Delek US Holdings DK, Phillips 66 PSX and Murphy USA MUSA, sporting a Zacks Rank #1 (Strong Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Delek US is valued at $2.54 billion. It is a U.S.-based downstream energy company that focuses on refining crude oil and distributing petroleum products. Headquartered in Brentwood, TN, Delek US Holdings operates through two main segments: refining and logistics.

Phillips 66 is valued at $66.61 billion. It is a diversified energy company that refines crude oil, markets petroleum products, and operates midstream, chemicals, and renewable fuels businesses. Phillips 66 operates across the United States and internationally.

Murphy USA is valued at $10.18 billion. The company is one of the largest independent gasoline and convenience store retailers in the United States, operating a network of stores primarily located near Walmart locations. Murphy USA focuses on offering low-cost fuel and everyday convenience products, supported by a strong loyalty program and disciplined capital-allocation strategy.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Transocean Ltd. (RIG): Free Stock Analysis Report

Delek US Holdings, Inc. (DK): Free Stock Analysis Report

Murphy USA Inc. (MUSA): Free Stock Analysis Report

Phillips 66 (PSX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).