The semiconductor industry is entering a major investment cycle, fueled by AI, advanced packaging, HBM and next-generation chip manufacturing. Among them, Onto Innovation, Inc. ONTO and KLA Corporation KLAC stand out as leaders in process control, inspection and metrology. KLA is the dominant industry player, while Onto Innovation is a fast-growing specialist focused on advanced packaging and semiconductor inspection technologies, making them a highly relevant comparison for investors.

Per a report from Fortune Business Insights, the global semiconductor metrology and inspection equipment market size is estimated to go from $15.84 billion in 2026 to $27.56 billion by 2034, at a CAGR of 7.2%. The semiconductor equipment market is growing as AI chips require increasingly precise manufacturing. Key demand drivers include advanced packaging, chiplet architectures, HBM, 2.5D/3D integration, automotive semiconductors and AI accelerator production. KLA benefits across leading-edge nodes, while ONTO is leveraged for advanced packaging investments.

Although both companies operate in similar markets, they differ significantly in size, product portfolio, customer exposure and growth prospects. Investors seeking exposure to semiconductor equipment must decide whether they prefer the stability of an established industry giant like KLA or the higher-growth potential offered by Onto Innovation.

The Case for KLAC

KLA is the global leader in semiconductor process control, benefiting from advanced inspection and metrology technologies, strong customer relationships and high switching costs as chip manufacturing becomes increasingly complex. KLA continues to view AI as a major growth driver and a key contributor to its accelerating momentum. The company is experiencing stronger-than-expected traction in advanced packaging, prompting it to raise its outlook for advanced packaging-related semiconductor process control revenue from approximately $635 million in 2025 to around $1 billion in 2026, which is significantly above previous expectations.

Since 2021, KLA has expanded its process control market share by 360 basis points and now holds a position roughly seven times larger than its nearest competitor. It expects accelerating wafer fabrication equipment growth in 2026 and 2027, driven by increasing demand for process control across leading-edge logic, HBM, advanced packaging, faster product cycles and rising semiconductor design complexity. These trends are increasing the need for KLA’s solutions to improve R&D efficiency, support fab ramps and optimize manufacturing yields.

KLA’s increasingly advanced systems and longer tool lifecycles are strengthening its high-margin services business, creating a predictable long-term growth driver as customers demand greater tool performance and uptime. Reflecting this momentum, the company introduced a 2030 financial model targeting 13-17% revenue CAGR, raised its services growth outlook to 13-15%, increased its capital return target to more than 90% of free cash flow and announced its 17th consecutive dividend increase along with a new $7 billion share repurchase authorization. KLA expects to outpace the broader wafer equipment market through 2030, supported by the growing importance of process control across semiconductor manufacturing.

Image Source: Zacks Investment Research

Despite the positive outlook, investors should monitor several risks. Emerging technologies such as electron-beam inspection could alter competitive dynamics in process control, requiring KLA to increase R&D spending if competing solutions offer superior performance or cost efficiency. Additionally, elevated component costs, including DRAM used in system image-processing computers, are expected to pressure gross margins through at least 2026. While supply remains secure, unfavorable product mix shifts or additional tariffs could further weigh on profitability and operating leverage.

The Case for ONTO

Rather than competing directly across KLA's entire product lineup, Onto Innovation focuses on niche markets experiencing rapid growth, especially those benefiting from AI chips and heterogeneous integration. Its smaller size allows it to grow faster when semiconductor capital spending accelerates. It has delivered strong revenue growth, driven by AI-related packaging demand, advanced inspection solutions, rising customer adoption, growing software revenue and expansion into specialty semiconductor markets. Its smaller revenue base also lets new customer wins generate an outsized percentage growth.

ONTO expects momentum to speed up in the second half of the year, supported by customer expansions, increasing adoption of new products and a growing backlog, leading to more than 15% sequential revenue growth and over 30% revenue growth in 2026. Demand is fueled by AI and high-performance computing applications, while the company's integrated optical process control and software solutions, strengthened through its strategic collaboration with Rigaku, enhance its value proposition for semiconductor manufacturers. As semiconductor manufacturers adopt more complex materials and 3D structures, management anticipates rising demand for hybrid metrology solutions that merge optical and X-ray technologies.

Image Source: Zacks Investment Research

Its Ai Diffract software, developed with Rigaku, has already secured two competitive wins and multiple customer evaluations, demonstrating its ability to address advanced process control challenges. The collaboration opens new revenue opportunities via software licensing and integrated metrology solutions, while Onto Innovation's 27% investment in Rigaku reinforces long-term alignment and access to next-generation X-ray technology. Combined, these capabilities position Onto Innovation to leverage growing demand in advanced packaging and cutting-edge semiconductor manufacturing.

Furthermore, ONTO’s Dragonfly platform is becoming a major growth driver, supported by a more than $240 million HBM-related volume purchase agreement through 2027 and expanding adoption across AI-driven advanced packaging applications. Recent customer qualifications, strong order momentum and growing demand for 3D inspection technologies are strengthening its position in high-bandwidth memory and advanced packaging markets, with the company expecting advanced packaging revenue to grow more than 50% in 2026.

Despite strong growth prospects, Onto Innovation faces risks from cyclical semiconductor spending, intense competition, customer concentration and geopolitical uncertainties in Asia. The company must continue innovating to maintain its market position, while ongoing supply chain constraints, particularly in precision optics, could adversely impact revenue growth and profitability.

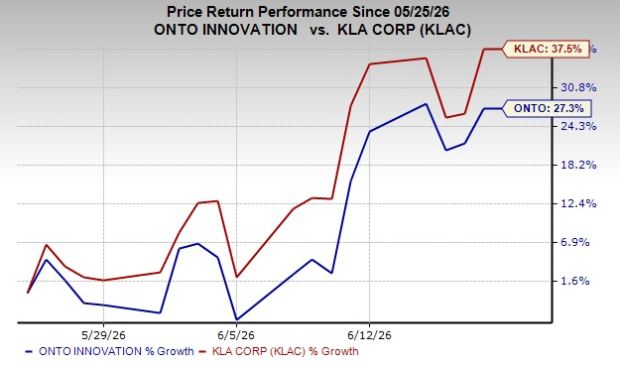

Share Performance Trajectory for ONTO & KLAC

In the past month, ONTO stock has surged 27.3% while KLAC has gained 37.5%.

Image Source: Zacks Investment Research

Valuation: Discount vs. Premium

Valuation often determines future investment returns. In terms of forward price/earnings, ONTO shares are trading at 39.61X, lower than KLAC’s 52.71X.

Image Source: Zacks Investment Research

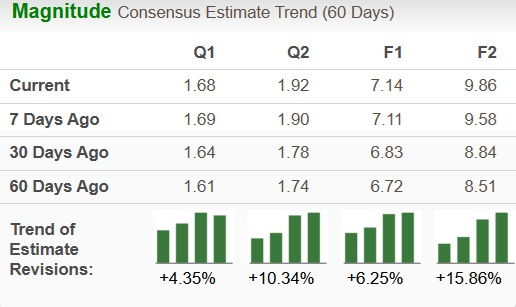

How the Zacks Consensus Estimate Compares for ONTO & KLAC

Earnings estimates for ONTO have moved up for both 2026 and 2027 over the past 60 days.

Image Source: Zacks Investment Research

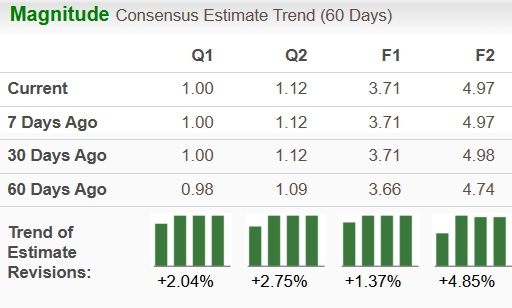

For KLAC estimates have moved up for both 2026 and 2027 over the past 60 days as well.

Image Source: Zacks Investment Research

ONTO vs. KLAC: Which Stock is the Better Pick?

Both ONTO and KLAC currently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies are well-positioned to benefit from the long-term expansion of semiconductor manufacturing, but they appeal to different types of investors. KLA is a strong choice for conservative investors, offering market leadership, solid profitability, recurring revenue and lower risk. Onto Innovation provides higher growth potential through its exposure to advanced packaging and AI semiconductor trends, but with greater volatility. Overall, KLA is better suited for stability and long-term consistency, while Onto Innovation appeals to investors seeking higher-risk, higher-reward opportunities.

Nonetheless, holding both stocks at present could provide balanced exposure to semiconductor industry growth, combining KLA’s stability with Onto Innovation’s higher growth potential.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

KLA Corporation (KLAC): Free Stock Analysis Report

Onto Innovation Inc. (ONTO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).