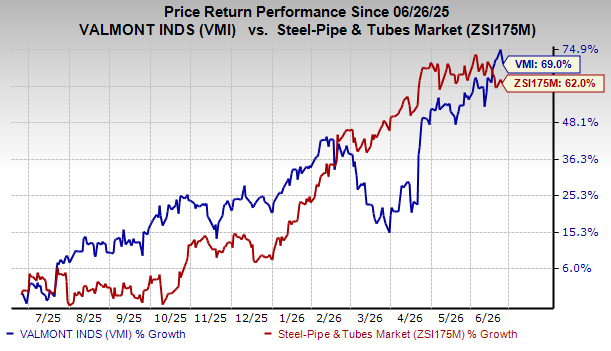

Valmont Industries, Inc. VMI shares have surged 69% over the past year, outperforming the Zacks Steel - Pipe and Tube industry’s rise of 62%. It has been benefiting from demands in utility infrastructure and growth actions led by restructuring and productivity enhancement initiatives toward expanding profitability. Multi-year investment in utility also indicates better growth momentum in the near future.

We are positive about VMI’s prospects and believe that the time is right for you to add the stock to the portfolio, as it looks promising and is poised to carry the momentum ahead.

Image Source: Zacks Investment Research

Let's see what makes VMI stock an attractive investment option at the moment.

Positive Analyst Sentiment for VMI Stock

Earnings estimates for VMI have been going up over the past 30 days. The Zacks Consensus Estimate for 2026 has increased by 5 cents. The consensus estimate for the second quarter of 2026 has also been revised upward by 3 cents over the same time frame. The favorable estimate revisions instill investor confidence in the stock.

VMI’s Strong Growth Prospects

The Zacks Consensus Estimate for VMI’s 2026 earnings is pegged at $22.83, suggesting a 19.59% increase from the previous year’s tally. Earnings are projected to increase by 18.03% in the second quarter of 2026.

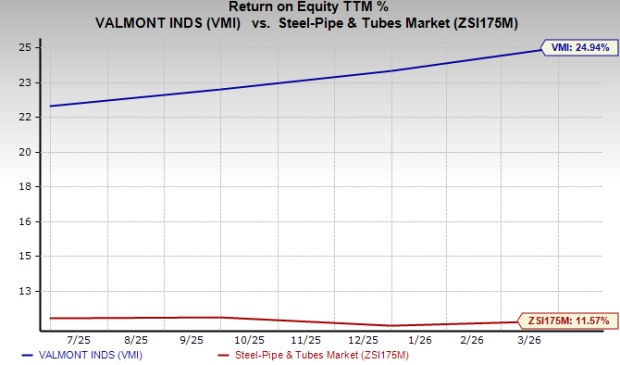

Superior Return on Equity (ROE) for VMI

ROE is a measure of a company’s efficiency in utilizing shareholders’ funds. ROE for the trailing 12 months for VMI is 24.94%, above the industry’s level of 11.57%.

Image Source: Zacks Investment Research

VMI Gains on Strong Utility Demand and Strategic Expansion

Valmont is well-positioned to benefit from multi-year investments in utility infrastructure, supported by electrification, grid modernization and rapidly growing power demand from data centers. The company’s Infrastructure segment continues to emerge as its primary growth engine, with management highlighting that U.S. utilities are expected to invest roughly $1.4 trillion through 2030 to upgrade and expand the electrical grid.

Strong backlog growth has improved revenue visibility and reinstated confidence in sustained demand for VMI’s distribution and substation structures, and continued strategic investments, which position the company to capture increasing utility spending and higher project volumes. In addition to favorable end-market trends, VMI is executing well on operational initiatives aimed at enhancing profitability. The company has implemented restructuring and productivity programs, removed production bottlenecks and upgraded manufacturing capacities, driving some of the strongest Infrastructure segment margins in recent years.

Brownfield expansion projects have added approximately $95 million in annual revenue capacity, while the deployment of AI-enabled scheduling and planning tools is improving efficiency and supporting further margin expansion.

Reflecting these positive fundamentals, management raised its 2026 earnings guidance and increased Infrastructure segment revenue expectations, underscoring confidence in its performance. With strong backlog growth, expanding capacity, improving operational efficiency and exposure to long-term utility investment trends, VMI remains well positioned to deliver sustained revenue growth, margin expansion and earnings growth over the coming years.

VMI’s Zacks Rank & Other Key Picks

VMI currently carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks in the Basic Materials space are Nucor Corporation NUE, Newmont Corporation NEM and Avino Silver & Gold Mines Ltd. ASM.

While NUE and NEM sport a Zacks Rank #1 (Strong Buy) each at present, ASM carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for NUE’s 2026 earnings is pinned at $16.34 per share, indicating a 111.93% year-over-year increase. Its earnings beat the Zacks Consensus Estimate in two of the trailing four quarters and missed the remaining two, with an average surprise of 8.10%. NUE’s shares have jumped 84.2% over the past year.

The Zacks Consensus Estimate for NEM’s 2026 earnings is pegged at $9.91 per share, indicating a rise of 43.83% year over year. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters. NEM’sshares have gained 58.8% over the past year.

The Zacks Consensus Estimate for ASM’s current fiscal-year earnings is pinned at 34 cents per share, indicating a 17.24% year-over-year increase. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with an average surprise of 125%.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Valmont Industries, Inc. (VMI): Free Stock Analysis Report

Nucor Corporation (NUE): Free Stock Analysis Report

Newmont Corporation (NEM): Free Stock Analysis Report

Avino Silver (ASM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).