Jabil, Inc. JBL has been one of the standout performers in the electronics manufacturing services industry, with its shares climbing sharply as AI infrastructure spending accelerated. The rally reflects growing investor confidence in the company’s ability to capitalize on AI-driven demand while improving profitability across its diversified business. The key question now is whether Jabil’s earnings growth can continue to justify its higher valuation.

JBL Earnings Continue Building Momentum

Jabil delivered another strong fiscal third quarter, reinforcing confidence in its execution. Revenue increased 11.8% year over year to $8.75 billion, while core diluted earnings per share climbed 23.9% to $3.16, exceeding the Zacks Consensus Estimate. The company also generated core operating income of $504 million, with its core operating margin improving to 5.8%.

Cash generation remained another bright spot. Adjusted free cash flow reached $359 million during the quarter, prompting management to raise its fiscal 2026 adjusted free cash flow outlook to more than $1.4 billion. Broad-based strength across AI infrastructure, capital equipment and warehouse automation, together with improving automotive and connected living demand, supported the stronger-than-expected results.

Image Source: Zacks Investment Research

Why Jabil’s Outlook Remains Constructive

Management continues to expect favorable business conditions through the remainder of fiscal 2026. The company increased its full-year revenue outlook to approximately $35 billion while projecting core diluted earnings per share of about $12.70 and core operating margins of approximately 5.8%.

AI infrastructure remains the primary growth driver. Management now expects approximately $13.6 billion in AI-related revenue during fiscal 2026, supported by expanding hyperscale customer relationships and increasing demand across cloud infrastructure, networking, compute, storage, cooling and rack integration. Automotive demand has also improved from earlier expectations, while healthcare, digital commerce and warehouse automation continue contributing to a more balanced growth profile.

Strong operating leverage, disciplined capital spending and an asset-light manufacturing strategy should continue supporting margin expansion and healthy cash generation as new production capacity comes online.

What Could Limit JBL's Upside?

Although Jabil’s operating momentum remains favorable, several factors warrant caution. Customer concentration continues to expose the company to the risk of reduced orders from major clients. The electronic manufacturing services industry also remains highly competitive, with companies such as Flex, Ltd. FLEX and Sanmina Corporation SANM competing for many of the same outsourcing opportunities.

Macroeconomic uncertainty, geopolitical developments and uneven demand across consumer-oriented markets could also create periodic volatility. While automotive trends have improved recently, management continues to view that end market cautiously because of ongoing demand fluctuations.

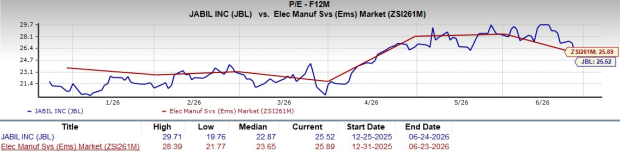

How JBL Valuation Shapes Expectations

Jabil's strong share price performance has lifted its valuation. The stock currently trades at a forward 12-month P/E of 25.52, compared with the sub-industry average of 25.89. While the premium is not significant, the valuation suggests much of the company's improving AI infrastructure outlook and earnings momentum may already be reflected in the share price. As a result, sustained revenue growth, margin expansion and continued execution will likely be important drivers of additional upside.

Image Source: Zacks Investment Research

How JBL Ranking Indicators Support Investors

Jabil currently carries a Zacks Rank #2 (Buy), reflecting favorable near-term earnings momentum. The stock also earns a Momentum Score of A, Growth Score of B and VGM Score of A, indicating attractive momentum and growth characteristics that complement its positive earnings outlook. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

However, the company’s Value Score of C suggests investors should balance those encouraging indicators against valuation considerations. Jabil’s AI-driven growth story remains intact, but after a powerful rally, continued execution will likely play an increasingly important role in determining future shareholder returns.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Jabil, Inc. (JBL): Free Stock Analysis Report

Flex Ltd. (FLEX): Free Stock Analysis Report

Sanmina Corporation (SANM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).