Tandem Diabetes Care, Inc. TNDM is well-poised to grow in the coming quarters as the rising prevalence of diabetes and increasing adoption of connected care continue to support demand for automated insulin delivery. The company’s pay-as-you-go reimbursement model could lower upfront barriers for pump starts and support higher supply revenue per customer over time. Solid financial health also adds to the stock’s appeal. Yet, macroeconomic pressures and execution risk surrounding the pump platform could weigh on Tandem Diabetes’ growth.

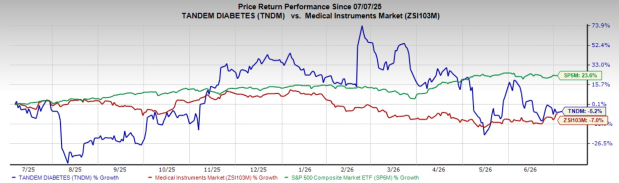

Over the past year, this Zacks Rank #3 (Hold) stock has declined 5.2% compared with the 7% fall of the industry. However, the S&P 500 composite has risen 23.6% during the same time period.

The renowned medical device company has a market capitalization of $1.05 billion. Tandem Diabetes has an estimated long-term earnings growth rate of 33.4%, outpacing the industry’s 12.5% growth. In the trailing four quarters, TNDM surpassed earnings estimates twice, matched in one and missed on one occasion, the average surprise being 23.7%.

Let’s delve deeper.

Tailwinds for TNDM Stock

Diabetes Market Expansion: Management described the insulin-dependent market as large and underpenetrated, and the global diabetes care device market is expected to witness a CAGR of 8.7% during 2025-2032. In the United States, Tandem Diabetes is now commercializing Control-IQ+ for both type 1 and type 2 diabetes, which broadens the eligible patient pool for its t:slim X2 and Mobi platforms. The company is also using its updated business model to target more conversions from multiple daily injections by lowering upfront barriers in the pharmacy channel. This creates a longer runway for new starts if execution is consistent across payer access, education and onboarding.

Image Source: Zacks Investment Research

Business Model Transition Adds Levers: Tandem Diabetes launched a pay-as-you-go reimbursement model in the U.S. pharmacy channel, building on expanded pharmacy benefit coverage and prior progress moving t:slim supplies into pharmacies. In first-quarter 2026, pharmacy sales represented 6% of U.S. sales, showing early traction but still leaving a long runway for mix shift. Management reaffirmed 2026 guidance for revenues of about $1.065 billion to $1.085 billion, gross margin of about 56% to 57% and adjusted EBITDA margin of about 5% to 6%. This framework suggests the near-term transition impact is contained within the plan, while the longer-term upside comes from lower upfront barriers for pump starts and higher supply revenue per customer as utilization builds.

Liquidity Supports Execution: Tandem Diabetes ended first-quarter 2026 with $570.3 million of cash, cash equivalents and short-term investments and closed a 0.00% convertible debt offering due 2032. The company had no short-term debt at the quarter-end. Operating cash flow was $11 million in first-quarter 2026, supported by higher gross profit and lower year-ago comparable that included acquired IPR&D expense. This liquidity can fund inventory, product development and the planned international buildout without forcing near-term equity issuance.

What Ails TNDM Stock?

Macro and Reimbursement Sensitivity: Demand for pumps and supplies depends on payer coverage and patient willingness to start or upgrade therapy, which can soften when broader economic conditions tighten or when healthcare systems push for lower device costs. Tandem Diabetes remains in a net loss position, and management is also implementing a pay-as-you-go model that lowers upfront cost but can shift revenue timing. If inflation, labor costs or logistics costs rise faster than planned, it can offset the company’s targeted gross margin expansion.

Reliance on Pump Platform Execution: Tandem Diabetes remains heavily reliant on pump sales to expand its installed base and recurring supply stream, making it vulnerable to product issues or supply disruptions. The company is still dealing with ongoing infusion set supply shortages. Meanwhile, management expects the rollout of extended-wear infusion sets to support customer experience and gross margin over time. Delays in product filings, integration or recalls could slow starts, raise costs and pressure long-term supplies growth.

TNDM Stock Estimate Trend

The Zacks Consensus Estimate for Tandem Diabetes’ 2026 loss per share currently stands at 72 cents compared with the year-ago quarter’s loss of $2.58.

The Zacks Consensus Estimate for the company’s 2026 revenues is pegged at $1.08 billion. This suggests a 6% increase from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Illumina ILMN, Align Technology ALGN and Integra LifeSciences IART.

Illumina has an earnings yield of 2.8% compared to the industry’s negative 14.6% yield. Its earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 12.2%. ILMN shares have rallied 95.8% compared with the industry’s 25.6% growth over the past year.

ILMN carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Align Technology, carrying a Zacks Rank #2, has an estimated long-term earnings growth rate of 10.3% compared with the industry’s 5.5% growth. Shares of the company have dipped 6.3% against the industry’s 9.6% growth. ALGN’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 7.8%.

Integra LifeSciences, carrying a Zacks Rank #2, has an earnings yield of 13.7% against the industry’s negative 3% yield. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 16.7%. IART shares have rallied 33.8% against the industry’s 10.5% decline over the past year.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tandem Diabetes Care, Inc. (TNDM): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Illumina, Inc. (ILMN): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).